|

|

|

|

|

Vol. 4, Iss.5

May 20, 2015

|

|

|

|

| |

|

| |

General Liability Insurance Coverage – Key Issues in Every State

Key Issues’s Link To The New York Times Best Seller List

Special Discounted Price

Unfortunately, there is a glitch on Amazon.com concerning the purchase of the 3rd Edition of Key Issues. I am trying to get it fixed. In the meantime, the book can be purchased at “Create Space” (which is an “Amazon company” anyway). I have arranged for a 30% off Discount Code so that the book can be purchased at the lowest price yet.

Use Discount Code 2WY94T8V at the following Create Space site to get this reduced price: http://www.createspace.com/5242805

More information about the 3rd Edition of General Liability Insurance Coverage – Key Issues in Every State here: http://www.InsuranceKeyIssues.com

***

Jeff and I are truly humbled by the number of people purchasing the 3rd Edition of General Liability Insurance Coverage – Key Issues in Every State, the kind comments people have sent and really positive reviews that the book has received. We also sincerely appreciate all the insurers who are buying the book in bulk for their claims staff. As the old adage goes, you can never be too rich or too thin or own too many copies of Key Issues.

On the subject of reviews, Nelson DeMille, multiple New York Times best seller, including three times at the #1 spot, put his claims adjuster hat back on and reviewed Key Issues. I interviewed DeMille in the last issue of CO and he was kind enough to say yes to my request to take a look at Key Issues and write a blurb about it.

|

|

As a former claims adjuster, I found General Liability Insurance Coverage: Key Issues in Every State informative and interesting. Randy Maniloff and Jeffrey Stempel are accomplished writers, and this is a great reference book and resource for anyone who wants to understand or write about these important issues.

Nelson DeMille

New York Times #1 Bestselling Novelist

Author of 19 Books

Over 50 Million Copies Sold |

|

| |

OK, so Key Issues having a link to The New York Times Best Seller list is tenuous. Like, really tenuous. Like, me saying that because I ripped tickets at a movie theater I worked in the motion picture industry. But hyperbole and headlines have long had a peas and carrots relationship.

See for yourself why so many find it useful to have, at their fingertips, a nearly 800-page book with just one single objective -- Proving the rule of law, clearly and in detail, in every state (and D.C.), on the liability coverage issues that matter most. |

| |

|

| |

|

|

|

| |

|

|

|

|

Vol. 4, Iss. 5

May 20, 2015

My Wall Street Journal Op-Ed On Pacquiao—Mayweather Post-Fight Lawsuits

|

|

|

Regular readers of Coverage Opinions know that a favorite topic of mine is lawsuits that involve professional sports that contain a fan component. Lawsuits surrounding numerous aspects of professional sports are abundant. They often involve business issues. But every once in a while a suit comes along that involves the fans in some way, such as fan being hit by a foul ball or injured by a furry mascot. These are great cases because, as fans, we have a first-hand appreciation for what one of the parties is thinking and feeling.

It took many years for the Manny Pacquiao—Floyd Mayweather so-called “Fight of the Century” to come together. But it took just three days for the first (of many) lawsuits to be filed by disgruntled fans on account of the impact of Pacquiao’s alleged late-disclosed shoulder injury. Below is a link to an Op-Ed that I published on the Editorial Page of the May 8th Wall Street Journal that looks at lawsuits brought by sports fans, whose expectations were not met, and how I believe that courts should handle them.

http://www.coverageopinions.info/wallStreetJournalMay82015.pdf

I hope you’ll check it out.

|

|

| |

|

|

|

|

|

|

For the past two weeks or so talk in the sports world has been dominated by one story – Deflate-gate. For the six people in America who do not know what this is, the New England Patriots were accused of using footballs, during the 2015 AFC Championship Game, that contained less air pressure than mandated by the National Football League rules. A softer football may be easier to grip and throw. The Patriots and its quarterback, Tom Brady, denied any wrongdoing.

Deflate-gate dialogue began on May 6th following the release of the “Investigative Report Concerning Footballs Used During The AFC Championship Game On January 18, 2015.” That’s the 243 page report, prepared by the NFL’s lawyer, Ted Wells, of his investigation to get to the bottom on the Deflate-gate story.

This report, now referred to as the Wells Report, reached, among others, the following conclusions: (1) It is more probable than not that Patriots locker room personnel – Jim McNally and John Jastremski -- participated in a deliberate effort to release air from Patriots game balls after the balls were tested by game officials; and (2) It is more probable than not that Tom Brady was at least generally aware of the inappropriate activities of the locker room personnel involving the release of air from Patriots game balls.

Then, just when the Wells Report was retreating from the front page, on May 11th the NFL announced the imposition of harsh penalties on the Patriots and Brady for their conduct. Brady was suspended for the first four games of next season without pay. The Patriots must forfeit their first round draft pick next year and a fourth round pick in 2017. The Pats were also fined $1 million. Of course, they’ll save a couple of million on Brady’s salary, so the team actually comes out ahead on the deal. How did the NFL not see that? In any event, with all this, Deflate-gate was back on the front page.

But despite the incredible noise that Deflate-gate has generated, Tom Brady has been virtually mum on the conclusions of the Wells Report and the sanctions imposed by the NFL. Until now. Brady has chosen to break his silence -- with an exclusive sit down interview with Randy Spencer.

Brady and I are seated at a back table in a small French bistro in Boston’s Beacon Hill neighborhood. It’s too late for lunch and too early for dinner so the place is empty. A young woman approaches – probably a college student. She shows no sign of recognizing the city’s most famous resident. Brady asks her what brands of water she has. She rattles off a few names. Unsatisfied with his choices Brady settles on an iced coffee. I was planning on ordering a Diet Coke. But that now seems out of the question so I also order an iced coffee – even though I really dislike it.

Randy Spencer: Tom, thank you for choosing Coverage Opinions and the Randy Spencer’s Open Mic column to discuss the Deflate-gate situation. I’m sure that media outlets have been relentless in pursuing you for an interview.

Tom Brady: No problem Andy.

RS: That’s Randy.

TB: Right. Yeah, you can’t imagine. ESPN’s drool could end the California drought. And that Matt Louder guy hasn’t stopped calling.

RS: That’s Lauer.

TB: Whatever. I’ve never heard of him. They tell me his show starts at 7 in the morning. Is anyone up that early? [It is clear from Brady’s tone that his question is a serious one.]

RS: Tom, let’s get right to it. You’ve been criticized for not turning over your cell phone to the NFL’s investigators. And the NFL stated that that played a part in its decision to impose a four game suspension. If you had nothing to do with the deflation of footballs, why didn’t you just turn over your phone?

TB: Look man, I’m Tom Brady. One of the greatest QBs ever to lace ‘em up. I’m cooler than the Fonz on his best day. I’m cooler than that Dos Equis guy. I’m so cool I can get away with endorsing Uggs. Plus I got movie star good looks. I’m the Super Bowl MVP. And I’m married to Gisele Bündchen, a super model. And not just any super model – a Brazilian one. She’s even got two dots over one of the letters in her name.

RS: You’re all those things Tom.

TB: Yeah, well, that’s exactly why I couldn’t turn over my cell phone. I couldn’t let people see how many emojis I use when sending text messages. [Brady holds out his phone to show it to me.] You see those two little sunny side up eggs in frying pans? I sent Gisele a text this morning with those pictures, and just from that, she knew that I wanted two eggs for breakfast. And if I’d wanted three eggs I would have just sent her three of those little frying pans. Man, it’s amazing. And if I wanted toast and coffee....

RS: Wow! I never figured Tom Brady as an emoji guy.

TB: I know. Nobody would. You hear emojis and you think Tim Tebow. Not Tom Brady. That’s why I needed to keep my cell out of Wells’s hands.

RS: But that decision cost you four games without pay.

TB: Totally worth it.

RS: Yeah, I can see that. Speaking of the four game suspension, what do you plan on doing to keep busy during those weeks?

TB: [Brady lets out a sigh of exasperation] Don’t ask. Gisele’s got me painting the powder room and cleaning out the garage. She says it’s time for me to throw out my Tom Brady poster collection. If I’m lucky I’ll pull a hammie the first week and get Gisele off my back.

RS: Let’s talk about the Wells Report. It’s the size of a book. Did you read all 243 pages?

TB: I didn’t know they made 243 page books.

RS: The Wells Report concluded that it is more probable than not that you were at least generally aware of the inappropriate activities of McNally and Jastremski involving the release of air from Patriots game balls. Is that true?

TB: Yeah, that’s what the report says.

RS: No, I mean, is it true that you were generally aware of what McNally and Jastremski were doing?

TB: No way. “Generally aware.” “More probable than not.” Who talks like that? Not normal people. If they had the goods on me they’d say so in English. We’re talking about deflating footballs with tons of people around. How hard can that be to prove? This isn’t exactly who killed JFK?

RS: But what do you say about the scientific experiments that concluded that the psi measurements of the Patriots game balls at halftime cannot be entirely explained by the Ideal Gas Law?

TB: Go ask Marvin Greenbaum.

RS: Who’s Marvin Greenbaum?

TB: He’s the guy whose paper I copied off of in high school chemistry.

[The waitress approaches with the drinks. Someone has now tipped her off to who’s sitting at the table. Aren’t you Randy Spencer?, she asks. I acknowledge that I am. She’s asks if we can take a selfie. Of course I oblige.]

RS: Tom, how do you explain the mountain of circumstantial evidence laid out in the Wells Report that McNally and Jastremski were involved in deflating game balls and you were generally aware of it.

TB: Look, the Patriots put together a website that responds to all the conclusions in the Wells Report. Check it out. It’s all in there. It says [Brady makes double quotation mark symbols with his fingers]: “There is no evidence that Tom Brady preferred footballs that were lower than 12.5 psi and no evidence anyone even thought that he did.” I knew nothing. That’s how normal people speak. That’s not weasel lawyer language.

RS: But some of the stuff on that Patriots website is hard to believe. It says that the term “deflator” used between McNally and Jastremski was a reference to McNally wanting to lose weight. Do you really believe that?

TB: If that’s what the Pats’s lawyers say then I believe it. If Bob [Kraft – Patriots owner] tells the lawyers to write a report saying that the earth is flat, then the earth is flat. We have really good lawyers.

RS: The Wells Report says that McNally took the game balls into the bathroom for a minute and forty seconds and that’s when he supposedly deflated them. The said it can be done in that amount of time.

TB: I know. But McNally says he was in there peeing. And that can be done in a minute forty. And if that’s what he says I believe him. Jimmy’s just not gettin’ a fair shake.

RS: You’ve appealed your suspension and it will be heard by Commissioner Roger Goodell. Are you OK with that?

TB: Yeah, that’s cool. Rog and I get along fine and I think he’ll be fair. Besides, I was his wingman one night when we went out during Super Bowl week. Trust me. He owes me.

[Brady’s cell phone rings. He answers it. “Right.” “Ok.” “Yes.” “I’ll get them.” He hangs up and looks at me. “Gisele. She wants me to bring home a quart of milk and a Mercedes.”]

RS: Why do you think that the public is so fascinated by Deflate-gate?

TB: Because it’s about Tom Brady, man. Tony Romo could throw footballs as flat as Frisbees and it would get less coverage on the sports page than a cricket match.

RS: You must know that people are less likely to believe the Patriots’s story because of Spygate.

TB: Look, that was all Belichick’s thing. I have no idea what he was doing. What a dumb idea. I didn’t need to be Dick Tracy to beat the Jets.

RS: What’s it like being coached by Bill Belichick?

TB: Don’t get me started. The NFL is crawling all over me about some slightly deflated footballs and Belichick is the one they should be investigating and writing reports about. Do you know why he cuts the sleeves off his hoodies? To sell them on Ebay. Hey Rog, you think that’s in the best interest of the game?

RS: It was reported that you went to the Kentucky Derby a few weeks back and then jetted to Vegas for the Pacquiao—Mayweather fight later that night. How was the fight?

TB: What a bust! You wanna talk about real deflation?

RS: Tom, do you think that Deflate-gate will hurt your legacy?

TB: The only thing about Deflate-gate that might hurt my legacy is that I did an interview about it with a stand-up comic who writes a column for an insurance law newsletter. [Brady smiles to let me know he’s kidding. At least I think he’s kidding.]

RS: Tom, thanks for speaking with me. I appreciate it.

TB: No problem, Andy.

[Brady pulls out his cell phone and sends a quick text. He holds it out for me to see. It’s a picture of two hour glasses.]

I just asked Gisele to make me two soft boiled eggs.

That’s my time. I’m Randy Spencer. Contact Randy Spencer at

Randy.Spencer@coverageopinions.info

|

|

| |

|

|

|

|

Vol. 4, Iss. 5

May 20, 2015

“Coverage For Dummies” Comes Early

Whoa! You Gotta See This. Perhaps The Greatest “Dummies” Case Ever

|

|

|

I have been writing “Coverage for Dummies” for the past six years. It is published at the beginning of the year and looks back at the best examples, from the year just completed, of people who did really dumb stuff and then attempted to secure insurance coverage for the harm caused.

I am a long ways away from publishing this year’s installment of Dummies. However, a recent case is just too good to wait eight months to share. An astute Coverage Opinions reader and Dummies fan alerted me to the recent decision in Blank-Greer v. Tannerite Sports, LLC, No. 13-1266 (N.D. Ohio Apr. 21, 2015) .

First, let me mention that, in Dummies 2014 (CO, January 14, 2015), I wrote about Davler v. Arch Ins. Co. (Cal. Ct. App. Aug. 25, 2014). In Davler, the court held that no coverage was owed to a cosmetics manufacturer when a (female) manager, determined to figure out who left a sanitary napkin in the bathroom and blood around the toilet seat, forced female employees to pull down their underwear so that another (female) employee could inspect whether they were wearing a sanitary napkin. The employment related practices exclusion precluded coverage.

I concluded that 2014 may be the last year for “Coverage For Dummies” because I figured that there would never be another case as good as Davler. Period.

Well, I may have to stand corrected. Tannerite Sports may top Davler as the all-time greatest Dummies case. I’ll quote liberally from the court’s opinion to demonstrate some folks’ ability to take stupidity to unimaginable heights.

“In May 2012, [James] Yaney’s friend, Jason Vantilburg, in anticipation of the birth of his first child, asked Yaney to host a party to celebrate. Yaney and Vantilburg fashioned the party into a ‘diaper shootout,’ where guests could bring diapers for the new baby and enjoy an afternoon shooting guns in Yaney’s backyard. As a ‘grand finale’ to the party, they also decided to blow up an old refrigerator.

In preparation, Yaney used his [Yaney] Motorsports truck to haul the refrigerator from Vantilburg’s home to his property. He then used his trailer to tow a box van to his backyard so that guests had a target to shoot. On the day of the event, Yaney set up the Motorsports truck and trailer as a staging area for guns and ammunition. ***

Towards the end of the event, Yaney and Vantilburg decided it was time to blow up the refrigerator. They hauled the refrigerator from Yaney’s pole barn into the backyard. Guests stood behind tables fifty meters away from where the refrigerator was located. Vantilburg moved into position behind his rifle, fired at the explosives [H2] inside the refrigerator, and detonated them. The refrigerator immediately blew apart and sent shrapnel flying across the yard. A piece of shrapnel hit (guest) Plank–Greer’s hand, nearly severing it.”

I know. It takes your breath away.

If I knew how to do it, this would have been a great opportunity to use one of those internet survey tools to allow readers to vote for which case -- Davler or Tannerite Spots -- is most worthy of claiming the mantle (for now at least) of all-time greatest “Coverage for Dummies” case.

***

Incidentally, if you are interested, the actual coverage issue involved whether Yaney’s policy with Auto-Owners, for his Auto Repair Shop, provided coverage. More specifically, did the incident arise with respect to the conduct of Yaney’s business. Yaney had invited customers to the party and Yaney discussed his business with Plank-Greet, offering to weld or manufacture a hitch for her car and a bike rack, and he gave her a price for new brake pads.

The court held that: “Here, at most, Yaney’s party mixed personal activities and business, with business being incidental (and, it would appear, coincidental). Yaney used the Motosports truck and trailer to haul items to his property for the party, and spoke with guests, including plaintiff, about his business. Yaney, however, did not co-host the party to promote his business: he held the party to help his friend, Jason Vantilburg, celebrate the impending arrival of his baby. Moreover, focusing solely on the event that gave rise to plaintiff’s injury—blowing up the refrigerator—there is no question that it was done for the guests’ entertainment and bore no relationship to Yaney’s business. Because Yaney was not acting solely with respect to his business, his activities that day were outside the scope of his insurance contract with Auto–Owners. Accordingly, Auto–Owners is not obligated to provide coverage to Yaney for any of Plank–Greer's allegations.”

|

|

| |

|

|

|

|

Vol. 4, Iss. 5

May 20, 2015

The Greatest Coverage Mysteries

|

|

|

For whatever reason, there have long been issues that cause confusion or are mysterious among those involved with coverage. To be clear, I’m not talking about the debate whether faulty workmanship is an “occurrence” or the pollution exclusion should apply narrowly or broadly. Those are disagreements over policy interpretation. Everyone gets it – they just don’t agree. I’m talking about something simpler -- where there is sometimes a misunderstanding of an issue at its core or just lack of knowledge. These are the issues where, if you ask five coverage professionals what something means, you’ll get more than one answer, perhaps some wrong answers and perhaps some I don’t knows.

What follows is a list of some of the Greatest Coverage Mysteries that I have seen over the years.

Just What Is A “Sidetrack Agreement”?

We’ve all seen the term in a commercial general liability policy – sidetrack agreement. It is one of the six enumerated things that quality as an “insured contract,” which is itself an exception to the Contractual Liability exclusion. But we virtually always brush over the “sidetrack agreement” on our way to the only part of the definition of “insured contract” that ever really comes into play: that part of a contract involving the assumption of another’s tort liability.

But just what is a “sidetrack agreement”? And does it ever come up in a case?

Not surprisingly, there is certainly not an abundance of case law addressing sidetrack agreements in the context of coverage disputes. Like, very few. One court that addressed it was United Fire & Cas. Co. v. Gravette, 182 F.3d 649 (8th Cir. 1999).

The Gravette court observed that the term sidetrack agreement was not defined in the policy so it turned to the dictionary for guidance, noting that “sidetrack” means “to shunt, to shift, as a train, from the main line to a siding.” Thus, the court concluded that “the common understanding of ‘sidetrack agreement’ would be an agreement regarding a railroad track or siding.” Based on that super helpful definition, the court held that “the trash hauling contract had nothing to do with railroads. It was not a ‘sidetrack agreement’ and therefore was not an ‘insured contract’ under the policy.”

You get a sense that the Gravette court was relieved that it could resolve the issue as simply as that and hightail it out of there.

The greater mystery than what’s a sidetrack agreement may be what’s it even doing in the policy – along with some of the other definitions of “insured contract” that are also pretty obscure, with likely almost no applicability.

Why Is The “Nuclear Exclusion” An Endorsement In Every CGL Policy?

Everyone likes the “Nuclear Exclusion”. That’s because, when you are reviewing a commercial general liability policy, it is two pages that you can safely skip over as inapplicable.

The Nuclear Exclusion is ubiquitous. It is an endorsement that appears in every CGL policy. But why? I know. Nuclear is associated with catastrophe. And insurers would not, could not, take on such monumental risk. But if you look at the language of the Nuclear Exclusion this makes absolutely no sense. In general, the Nuclear Exclusion applies to insureds that are in the business of owning or operating nuclear facilities or providing services or equipment to them. Needless to say, the number of entities specifically in nuclear-related businesses is infinitesimal. Nonetheless, show me a policy issued to a candy store, plumber or nail salon and I’ll show you the Nuclear Exclusion.

The Curious Definition of “Bodily Injury”

I always thought it was a cardinal rule of document drafting that you do not use the term being defined as part of the definition. That certainly makes sense. Then how come ISO’s standard-bearer commercial general liability policy has, curiously, long-defined the critical term “bodily injury” as “bodily injury, sickness or disease sustained by a person, including death resulting from any of these at any time?”

Why Doesn’t Coverage Part B (“Personal and Advertising Injury”) Contain An Employee Exclusion?

There can be no doubt that Coverage Part A (“Bodily Injury” and “Property Damage”) of a commercial general liability policy has no interest whatsoever in providing coverage for injuries sustained by an insured’s employee. The policy’s “Employer’s Liability Exclusion” makes that crystal clear.

But Coverage Part B (“Personal and Advertising Injury”) does not include an “Employer’s Liability Exclusion.” And the definition of “Personal and Advertising Injury” includes slander and libel of a person. It is not at all uncommon for an employee, bringing a claim against an employer for wrongful termination, to allege that they were defamed in the course of their termination. Barring any other issues, such a claim should trigger a defense under a CGL policy.

However, most insurers have no interest in providing coverage, under a CGL policy, for wrongful termination or any other employment practices. After all, they are busy selling stand-alone Employment Practices Policies. So that’s why most CGL policies are endorsed with a specific exclusion for various types of employment practices. So if insurers have no appetite for providing CGL coverage for employment practices, as evidenced by the wide-spread adoption of an employment practices exclusion endorsement, then why not simply include such an exclusion in the body of the policy?

When Is A Claim Made Under A “Claims Made” Policy

An important aspect of a “claims made” policy is when a claim is “made.” ISO’s “claims made” CGL policy, and others, states: “c. A claim by a person or organization seeking damages will be deemed to have been made at the earlier of the following times: (1) When notice of such claim is received and recorded by any insured or by us, whichever comes first; or (2) When we make settlement in accordance with Paragraph 1.a. above.”

I’ve always found this a curious provision. Is it possible for an insurer to settle a claim before notice of such claim is received by the insured or insurer?

What Is a “Hostile Fire”?

Just like a “sidetrack agreement,” “hostile fire” are two other words contained in a commercial general liability policy that we all see but never stop at to say howdy. The term “hostile fire” appears in the CGL policy’s absolute pollution exclusion. The exclusion generally precludes coverage for pollutants at certain premises, but contains exceptions, including one for bodily injury or property damage arising out of heat, smoke or fumes from a “hostile fire.” “Hostile fire” is defined as “one which becomes uncontrollable or breaks out from where it was intended to be.”

But what does that mean – a fire which becomes uncontrollable or breaks out from where it was intended to be. It can’t just mean any old fire – or the exception to the pollution exclusion would be for bodily injury or property damage arising out of heat, smoke or fumes from a “fire.”

It works like this (and, believe me, I had to look this up). Courts historically interpreted fire insurance policies to exclude damages from “friendly fires.” The rationale for this being that the insurer should not assume the risk for a fire that was intentionally ignited and remained confined where intended. Thus, the term “hostile fire” came to be the judicially created term for a fire outside the exclusion for “friendly fires.” Now I get it.

How Does An “Extended Reporting Period” Work

An “Extended Reporting Period” is an important component in a “claims made” professional liability policy. Yet I am often amazed when I hear variations in explanations of it and actually see substantive differences in how it is expressed in policy language. Despite all this, an “Extended Reporting Period” has just one meaning. It provides coverage for claims that are first made against the insured during the Extended Reporting Period – provided that the act, error or omission (i.e., wrongful act) took place after the retroactive date and before the expiration of the policy, i.e., before the commencement of the Extended Reporting Period. An ERP does not provide coverage for wrongful acts that take place during the “Extended Reporting Period.”

It is remarkable how often I hear an “Extended Reporting Period” being explained as a policy provision that extends the period of time for which a claim, made against the insured prior to the end of the policy period, can be reported. While the name “Extended Reporting Period” may suggest this meaning, it is neither accurate or logical. If a claim is made prior to the end of the policy period, wouldn’t it be easier, and cheaper, for the insured to simply report it to the insurer before the end of the policy period, instead of purchasing an extension so that such claim can be reported later? Clearly the name “Extended Reporting Period” – which has little to do with reporting -- is causing some confusion over what it means.

Why Is Contractual Liability Coverage Provided In The Manner It is?

An important aspect of coverage, under a commercial general liability policy, is for an insured’s obligation, to contractually indemnify another, for its tort liability for bodily injury or property damage to a third person or organization. This isn’t some once in a lifetime claims situation, like the $250 provided for bail bonds following a traffic accident. To the contrary, the providing of coverage, for an insured’s contractual indemnity obligation, for another’s tort liability, is a critical component of the CGL policy. It seems curious that such an important coverage grant is provided in such an obscure manner -- by way of an exception, to the otherwise exclusion, for contractually assumed liability.

|

|

| |

|

|

|

|

|

|

Vol. 4, Iss. 5

May 20, 2015

I’m Not Lion:

Court Holds That Cat Urine Not Precluded By Pollution Exclusion

Case More Enjoyable Than Cats

|

|

|

|

| |

Pollution Exclusion cases have become so abundant, and similar, that I’ve taken to limiting my discussion of them in Coverage Opinions to the ones that are truly unique. (See CO, __ (trust me)). Mellin v. Northern Security Insurance Co., No 2014-020 (N.H. Apr. 24, 2015) is in the unique category. The New Hampshire court addressed whether cat urine is a pollutant. This was a national case of first impression. That explains why I had no Meeeemory of ever seeing it.

The issue in Mellin arises under the property section of a homeowner’s policy. But the case and analysis is just as applicable to a dispute under a liability policy. [Not that that matters since this is the first, and probably last, time that the issue will arise.]

At issue was coverage for homeowners who sustained damage to their condominium on account of the smell of cat urine emanating from a downstairs neighbor’s condo. The affected homeowners claimed that they could not rent the condo (a tenant had in fact moved out) and they ultimately sold it for significantly less than it was worth (presumably to cat owners or someone with a habitually stuffed nose).

The homeowners sought coverage for their damages and the case made its way to the New Hampshire Supreme Court. There were three principal issues before the court. Did the claim satisfy the policy’s requirement that the unit “experienced a direct physical loss” as a result of the cat urine odor? Did the pollution exclusion bar recovery? Was the cat urine odor caused by any of the enumerated perils against which the policy insured? I’ll skip this last issue.

The court held that “physical loss may include not only tangible changes to the insured property, but also changes that are perceived by the sense of smell and that exist in the absence of structural damage. These changes, however, must be distinct and demonstrable. Evidence that a change rendered the insured property temporarily or permanently unusable or uninhabitable may support a finding that the loss was a physical loss to the insured property.” [This general issue, whether odor can qualify as physical loss, arises with some regularity.]

Turning to the pollution exclusion, following a lengthy analysis, the court held that it did not apply. In general, the court interpreted the pollution exclusion narrowly, despite how broadly it may read on its face.

The court stated: “Applying these definitions in a ‘purely literal interpretation ... surely stretch[es] the intended meaning of the policy exclusion,’ ‘contrary to any reasonable policyholder’s expectations.’ For example, ‘[t]aken at face value, the policy’s definition of a pollutant is broad enough that it could be read to include items such as soap, shampoo, rubbing alcohol, and bleach insofar as these items are capable of reasonably being classified as contaminants or irritants.’” (citations omitted).

In general, the New Hampshire Supreme Court limited the pollution exclusion’s applicability to traditional environmental pollution: “Although an insured may have reasonably understood that the pollution exclusion clause precluded coverage for damages resulting from odors emanating from large-scale farms, waste-processing facilities, or other industrial settings, these circumstances are distinguishable from those before us, which involve an odor created in a private residence by common domestic animals. See Western Alliance Ins. Co., 686 N.E.2d at 999 (recognizing that ‘an insured could reasonably have understood the provision at issue to exclude coverage for injury caused by certain forms of industrial pollution, but not coverage for injury allegedly caused by the presence of leaded materials in a private residence’ (quotation omitted)).”

But, like Morris the Cat, the court was finicky and the decision was not unanimous. The opinion includes a lengthy dissent: “Because the term ‘pollutant” is unambiguously defined within the policy in clear language, I would not look beyond the policy language in determining that the plaintiffs’ claims are precluded by the pollution exclusion clause. This approach is in keeping with the rulings of many courts, which likewise interpret pollution exclusion clauses by looking to the plain meaning of the terms as defined in the text of such clauses.” The dissenting Justice also had this to say on the way out: “I share the view of the Supreme Court of Minnesota that if the pollution exclusion clause is regarded as overly broad, the remedy must be found in the market place or through legislative action rather than through creative judicial construction of clear policy language.” |

|

|

|

|

|

Vol. 4, Iss. 5

May 20, 2015

Lawyer Thinking About Work, On the Way To The Office, Is Not Working

Coverage Opinions Gets A Mention In The Wall Street Journal Law Blog

|

|

|

Cases involving coverage under automobile policies do not usually get a lot of play in Coverage Opinions (what is “use of an auto” cases are sometimes an exception; see infra). But the Supreme Court of Virginia’s decision in Bartolomucci v. Federal Insurance Co., Nos. 140275, 140297 (Va. April 16, 2016) not only finds a home here, but it also made the mainstream media. Sadly, unfairly and cruelly, that just doesn’t happen too often.

Bartolomucci involved a lawyer who was in a car accident on his way to the office. He didn’t have enough insurance so he sought to be covered under his law firm’s auto policy. His argument, based on policy language, was that, while his personal vehicle was not owned by his law firm, it was being used in the firm’s business or personal affairs. Thus, the lawyer argued that his vehicle was covered under the firm’s policy.

In general, the lawyer’s arguments were as follows:

• Since he also works from a home office, he was traveling between work locations and not commuting.

• He habitually thought about work related issues on his commute to work.

• He had a Blackberry, issued and paid for by his law firm, turned on and within his physical reach.

The Virginia Supreme Court rejected the lawyer’s arguments:

“Contrary to these arguments, the facts of this case do not amount to anything more than a typical commute from home to work, which was not covered under the terms of the Federal Policy. The only work related activity that Bartolomucci accomplished before leaving home was to check his work email and call his office voicemail. But the record does not indicate that Bartolomucci read or responded to any work related emails, that the voicemail itself was work related, or that Bartolomucci billed his time for these activities. In addition, beyond the fact that Bartolomucci occasionally worked at home, the record fails to show any relationship between Hogan Lovells and Bartolomucci’s home to establish that place as a Hogan Lovells work location. Moreover, Bartolomucci’s use of his vehicle to commute from home to work was not a ‘use[ ] in’ Hogan Lovells’s business or personal affairs. Bartolomucci did not use his Blackberry during the commute. Merely having access to modern technology such as a Blackberry, which would allow Bartolomucci to conduct work activity if that device was used, ‘does not transform’ an employee’s ‘private activity into company business.’ And merely thinking about work does not make a commute ‘in’ the business, as contemplated by the policy language. The record does not indicate that Bartolomucci billed for any activity or otherwise performed any work during his commute. Also, Bartolomucci was not reimbursed by Hogan Lovells for his commute.”

This decision is hardly surprising. If thinking about work and having a smart phone provided by your employer nearby, even when not in the office, qualified as acting within your employer’s business, there would almost be no end to an employee’s status as an insured under a liability policy.

As for the mainstream media, The Wall Street Journal Law Blog did a post on the Bartolomucci case. On a personal note, it was exciting that your friendly neighborhood insurance coverage newsletter was called upon by The Journal for comment on the case. Here is The Wall Street Journal post:

http://www.coverageopinions.info/WallStreetJournalAPRIL2015.html

|

|

| |

|

|

|

|

|

|

Vol. 4, Iss. 5

May 20, 2015

Emily Post Would Not Approve

He Really Said That? And Then That?

|

|

|

There is no other way to put it. Amica Mutual Ins. Co. v. Vernon, 14-235 (D. Idaho Apr. 17 2015) is a coverage case that grows out of a sad situation. The unfortunate story is told by the court right from the get go. I’ll just set it out here:

“Defendant Russell Vernon and now deceased Roberta McIntire worked at Century Link in Boise, Idaho. The two employees rarely interacted with each other. Several months before Vernon retired in May 2011, and while at work in the break room, Vernon asked Roberta how she made her coffee. She responded, ‘What f*cking business is that of yours?’ The two co-workers had little further interaction until December 2011, when Vernon mailed an anonymous card with an enclosed letter to Roberta. The front of the card read, ‘F* * * You, You F* * *ing F* * *.’ The letter inside the card contained four paragraphs of insults, some of which read: ‘It goes without saying that you undoubtedly must know by now how much you are disliked by the techs here ...;’ ‘Hopefully someday R(redacted) will wise up and dump you for something worth having. It’s funny how many of us like R(redacted) yet would laugh ourselves silly if you were to get run over by a train; and ‘Every year we hope that this will be your last one here but every year you stay.’”

Roberta committed suicide five days after receiving the card and enclosed letter.

Roberta’s Estate and her mother sued Vernon for negligence, wrongful death, intentional infliction of emotional distress, and negligent infliction of emotional distress. Vernon sought coverage under his homeowner’s policy with Amica Mutual Insurance Company. Amica filed an action seeking a declaration that it had no duty to defend or indemnify Vernon. The Idaho federal court held that Amica had no such duties.

At the outset, the court observed: “Much can be said about Vernon’s conduct. However, one thing that cannot be said is that his conduct was accidental.” The court did not provide any analysis as to how it reached this conclusion -- presumably because it was not the basis for its decision. And I didn’t look at Idaho law on the “what’s an ‘accident’ issue.” But, on its face, I’m not convinced that this wasn’t an accident. While Vernon’s conduct was intentional (very intentional), it seems unlikely that he intended to cause Roberta to commit suicide or that it was substantially certain that, by sending the card and letter that he did, she would commit suicide.

In any event, the court concluded, and without breaking a sweat, that coverage for Vernon was precluded by the policy’s exclusion for “[b]odily injury ... arising out of ... mental abuse.” The court held: “It is unimaginable that sending a card to someone which begins, ‘F* * * You, You F* * *king F* * *,’ and then continues on with an additional four paragraphs of vicious and personal insults, could be regarded as anything but ‘mental maltreatment.’ The card falls within any reasonable definition of mental abuse. If sending a card and [the] enclosed letter . . . does not constitute mental abuse, then nothing does.”

The Court was not persuaded by Vernon’s argument in support of coverage: that “the card and letter constitute a ‘social interaction.’” Yes, you read that right, social interaction. That’s really how Vernon characterized the card and letter in support of a duty to defend.

Now, I don’t usually dig into the briefs when writing about a decision. I just don’t have time. I take the opinion for what it says. But this was an exception. I just had to know more about this “social interaction” argument. So I spent a couple of bucks and went onto Pacer (no expense spared for you dear CO readers). Here’s how it was described in Vernon’s Cross-Motion for Summary Judgment: “We maintain that the interaction that occurred between the decedent and the Defendant was nothing more than a ‘social interaction’ to which the decedent was ‘required to be hardened to a certain amount of rough language and to occasional acts that are definitely inconsiderate and unkind.’ (citation omitted). And, the card sent to the decedent did not rise to a level of mental abuse but rather was part of social interaction. The decedent said a profane comment to the Defendant and the Defendant reacted with the card.”

|

|

| |

|

|

|

|

|

|

Vol. 4, Iss. 5

May 20, 2015

Insurance Drones: The Headline That Should Have Many Of Us Up In Arms

|

|

|

| |

Everywhere you turn these days the talk is drones, drones, drones. They supposedly have a million and one uses, including, we’re told, by Amazon for the delivery of packages. I’m dubious that Amazon will ever be dropping books from the sky onto my front porch. The awesome guy who delivers my newspaper every morning virtually always misses the driveway. And he’s throwing the paper from ten feet away -- and while on Earth.

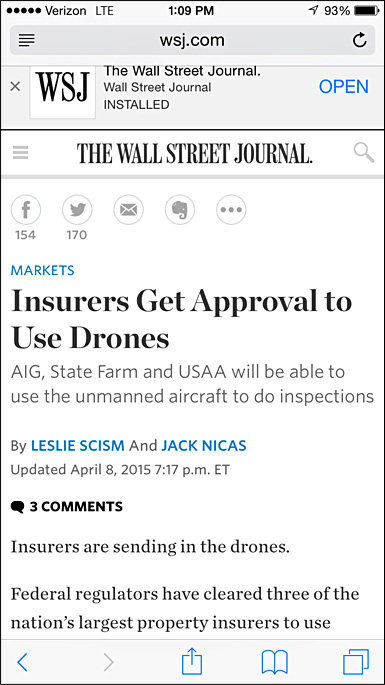

In any event, while Amazon’s use of drones may be a ways away, the insurance industry’s is not. In fact, the day has come. There have been lots of headlines lately about various insurers being granted permission by the FAA to use drones in the claims and underwriting processes. Of course, for those of us who do work for insurers -- as employees or outside providers; which is practically everyone reading this – these stories have generated some unfortunate headlines, such as this one:

Such headlines aside, drones seem to have some legitimate uses for insurers. Consider this lede paragraph from an April 9th story posted on engadget.com under the headline “FAA Allows AIG To Use Drones For Insurance Inspections:” “The Federal Aviation Administration has been rather stingy when it comes to giving companies the OK to test, let alone employ, drones. After getting permission this week, AIG joins State Farm and USAA as insurance providers with exemptions that allow them to use the UAVs [unmanned aerial vehicles, i.e., technical term for drones] to perform tasks that are risky to regular folks -- things like roof inspections after a major storm. In addition to keeping its inspectors safe, the company says drones will speed up the claims process, which means its customers will, in theory, get paid faster. ‘UAVs can help accelerate surveys of disaster areas with high resolution images for faster claims handling, risk assessment, and payments,’the news release explains. They can also quickly and safely reach areas that could be dangerous or inaccessible for manual inspection, and they provide richer information about properties, structures and claim events.” |

|

|

|

In an April 15th story on Insurance Journal’s website, about Erie Insurance’s receipt of FAA approval to use drones, a company executive had this to say: “‘Drones will help our claims adjusters get an early look at potential damage without putting themselves in harm’s way due to unsafe conditions, such as on a steep roof or at the site of a fire or natural disaster,’ [Gary] Sullivan [Vice-president of Property and Subrogation] said. Sullivan added, ‘The sooner we can get in and assess damage, the sooner we can settle claims and help make our customers whole again so they can move on with their lives. We’re proud to be one of the first insurance companies at the forefront of this next chapter in claims innovation.’”

There is another part of the story when it comes to insurance and drones – insurers providing coverage for individuals and entities whose drones cause damage to people or property. It is hard to imagine that the widespread use of drones won’t lead to such claims. And I’m sure we can all image some invasion of privacy claims being brought against drone users. The insurance industry has a long history of quickly responding to emerging risks with risk transfer products. The availability of drone insurance is no exception. Check out drone-insurance.com and riskoverwatch.com for just two sources of coverage.

This is just the beginning of the story when it comes to insurance and drones. Some supposed use of drones seem unlikely to come to pass – or at least not for a long time. But for the insurance industry, drones – both for their own use and as a business opportunity – are here and to stay.

|

|

| |

|

|

|

|

|

|

Vol. 4, Iss. 5

May 20, 2015

To Whom To Send Your Reservation Of Rights Letter

|

|

|

Sometimes the question is asked whether a reservation of rights letter should be sent to defense counsel. That’s one about which there are differences of opinion. That’s not what this article is about. It is about a more fundamental question – to which insureds should a reservation of rights letter be sent? This is the important lesson to come out of Erie Insurance Exchange v. Lobenthal, No. 1971 WDA 2013 (Pa. Super. Ct. Apr. 15, 2015).

Lobenthal involved coverage for a motor vehicle accident. I’m going to skip some of the details and focus on the overarching lesson from the case.

Kory Boyd suffered injuries in a motor vehicle accident while a passenger in a car driven by Devin Miller. An underlying complaint alleged, among other things, that Michaela Lobenthal engaged in “negligent, careless, reckless, outrageous, willful and wanton conduct” and concerted tortuous conduct in that she permitted the possession and consumption of controlled substances by Defendant Miller at a property owned by Defendant Lobenthal’s parents which was covered by [the Erie] insurance policy.”

Putting aside some details, Erie defended Michaela Lobenthal -- being an insured as a resident of her parents’ household. But there was a coverage issue – the potential applicability of a “controlled substances” exclusion. Despite Erie sending two reservation of rights letters, the issue before the Pennsylvania appeals court was whether Michaela Lobenthal was being defended under a reservation of rights.

Here is how that issue could be: “In the instant case, Erie sent two reservation of rights letters, one on April 28, 2011, prior to the underlying complaint being filed, and another on February 7, 2012. Both letters were addressed only to the named insureds, Michaela’s parents, Adam and Jacqueline Lobenthal; neither letter mentioned the defendant in the underlying tort action, Michaela Lobenthal, who had attained majority status as of November 20, 2010. These letters reserved Erie’s right to disclaim coverage and liability for any judgment ‘that may be rendered against yourself,’ i.e., against Adam and Jacqueline Lobenthal. Furthermore, only the second reservation of rights letter, sent approximately three and one-half months after the preliminary objections were decided, referenced the controlled substances exclusion in the policy.” [Preliminary objections resulted in the covered claims, providing alcohol, being dismissed.]

The opinion notes that Michaela’s parents were voluntarily dismissed from the underlying action in June 2011, i.e., they were not defendants when the second reservation of rights letter – at the time that the case was in suit -- was sent.

The court had little trouble concluding that, despite the February 7, 2012 reservation of rights letter being addressed to the named insureds, Michaela’s parents, as well as being sent to her defense counsel, Michaela was not being defended under a reservation of rights.

The court’s decision was as follows: “Erie’s reservation of rights letter was addressed solely to the named insureds, Adam and Jacqueline Lobenthal, not to Michaela. The letter made no mention of Michaela. As in [citation omitted], we will not impute notice to Michaela based on the fact the letter was sent to counsel where the letter was addressed to her parents and made no reference whatsoever to Michaela. By the same token, we refuse to attribute notice to Michaela based on the fact that she was living with her parents at the time. Michaela was an adult at the time the lawsuit was filed, and there is no evidence that she actually read the letter. Michaela was the defendant in the underlying tort action, and the letter should have been addressed in her name.”

Thus, despite that Erie should have owed no coverage to Michaela, on account of the controlled substances exclusion – the court made that point clear – such was not to be the case, as no reservation of rights letter was ever sent to her.

There is much that can be said about this opinion.

Since Michaela’s parents were not defendants when the second reservation of rights letter was sent, a letter addressed to them, stating that Erie was reserving its right to disclaim coverage and liability for any judgment “that may be rendered against yourself,” i.e., against Adam and Jacqueline Lobenthal, certainly lacked precision.

But the overarching take-away from Lobenthal is that, when an insurer sends a reservation of rights letter, no matter how well-drafted it is, it must address coverage for all insureds and be sent to or on behalf of them. There are opportunities for this to be missed. For example, consider a complaint that names several insureds as defendants, such as a named insured company and several of its employees. Here an insurer could overlook the employee-insureds, and send a reservation of rights letter to only the named insured company, and limit the discussion of coverage to the named insured. There are ways in which this problem can be avoided -- while still sending a single reservation of rights letter. This is usually the preferred way to go since sending numerous reservation of rights letters, even if they are very similar, can be an administrative challenge. But sometimes it is necessary to send separate reservation of rights letters to each insured or groups of insureds. This can be the case when the various insureds’ interests in the underlying litigation are not aligned and, therefore, they are being represented by different counsel. Policy language may also spell out to whom notice of certain things should be addressed. Whatever the case may be, a lot of effort that is put into a reservation of rights letter may be for naught if some insureds are overlooked.

|

|

| |

|

|

|

|

Vol. 4, Iss. 5

May 20, 2015

Federal Appeals Court Provides Detailed Discussion Of “Reverse Bad Faith”

|

|

|

So-called “reverse bad faith” is a double-edged sword for Coverage Opinions. On one hand, it is an issue that does not arise too often. And CO seeks to focus on cases that could have wide impact. On the other hand, because reverse bad faith does not come about every day, its uniqueness makes it an attractive case for CO. Uniqueness wins out.

In State Auto Property and Casualty Ins. Co. v. Hargis, No. 13-5020 (6th Cir. May 6, 2015), the Sixth Circuit Court of Appeals provided a detailed discussion of “reverse bad faith.” Bottom line -- the court held that a common law tort claim by an insurer, against an insured, for reverse bad faith, is not recognized under Kentucky law. In fact, the Hargis court also observed that it is “not aware of any jurisdiction that has recognized a cause of action for reverse bad faith.”

Hargis arose out of a fire claim under a homeowner’s policy. Lori Hargis’s home, located in Henderson, Kentucky, was insured by State Auto under a homeowner’s policy. The home burned to the ground. Hargis filed an insurance claim for approximately $866,000. State Auto paid the claim and subsequently commenced an action to declare the policy void, alleging that Hargis caused or conspired to cause the fire and falsely inflated the property loss resulting from the fire.

Hargis asserted counterclaims against State Auto for breach of contract and bad faith under Kentucky common law, the Kentucky Consumer Protection Act and the Kentucky Unfair Claims Settlement Practices Act. State Auto’s investigation eventually led to Hargis’s admission that she had solicited a friend to burn down her house to collect the insurance proceeds. Hargis pleaded guilty and was sentenced to 60 months in prison and ordered to pay restitution to State Auto.

After the indictment was returned against Hargis, State Auto moved for partial summary judgment and Hargis’s bad faith claims were dismissed. State Auto also filed an amended complaint that added a statutory claim for damages for insurance fraud and a common law tort claim, under Kentucky law, for reverse bad faith. State Auto’s argument, in support of reverse bad faith, was that “there is a strong public policy against allowing insureds to profit from their own wrongdoing while simultaneously subjecting insurers to inordinate increased costs for investigation, defense, and litigation.”

The District Court rejected the insurer’s claim for reverse bad faith. The Sixth Circuit agreed. At the outset, the court noted that State Auto cited no Kentucky case that has adopted a claim, by an insurer, for reverse bad faith against an insured. Further, the court stated that it was “not aware of any jurisdiction that has recognized a cause of action for reverse bad faith.”

Despite State Auto’s inability to point to any decisions in Kentucky (or elsewhere) that have recognized a common law claim for reverse bad faith, “State Auto argue[d] that there was no reason to conclude the Kentucky Supreme Court would not decide to allow tort recovery ( i.e., compensatory and punitive damages) for an insured’s bad faith since the implied covenant of good faith and fair dealing imposes contractual obligations on both parties. That is, State Auto contends, it is ‘unjust’ for Kentucky law to allow Hargis to assert a common law tort claim for bad faith without having to face the threat of a reciprocal tort claim for reverse bad faith.”

Nonetheless, for a host of reasons, the Sixth Circuit predicted that the Kentucky Supreme Court would reject State Auto’s invitation to adopt a common law tort claim for reverse bad faith by an insured. These were as follows:

• The reasons articulated by the Kentucky Supreme Court in recognizing first-party common law bad faith. Namely, that a fiduciary relationship existed between the insurer and its insured.

• A prior rejection, by the Kentucky Supreme Court, of an insurance company’s challenge to the fact that the Kentucky Unfair Claims Settlement Practices Act affords rights and remedies to an insured but provides no reciprocal rights or remedies to insurers.

• The standards for proving a claim of bad faith.

• The availability of other remedies for the damages incurred as a result of an insured’s fraud under Kentucky law. More specifically, the court explained: “State Auto repeatedly returns to the theme that it is ‘unjust’ for Kentucky law to allow Hargis to escape the consequences of her intentionally fraudulent conduct. But, she plainly did not. Her fraudulent conduct resulted in a civil judgment against her for all of the damages incurred by State Auto and subjected her to incarceration and an order of restitution to State Auto. The criminal conviction simplified State Auto’s proofs by establishing both breach of contract and the statutory claim for insurance fraud. . . . Further, even if the prosecution had not gone forward, there is no suggestion that State Auto could not have brought a common law claim for fraud. Finally, to the extent that State Auto claims that the threat of punitive damages is necessary to deter such fraudulent conduct, it is hard to imagine that a possible claim for reverse bad faith would be a deterrent if the threat of criminal prosecution was not.”

• The absence of support in other jurisdictions for reverse bad faith.

What I found most interesting was the court’s observation that it was “not aware of any jurisdiction that has recognized a cause of action for reverse bad faith.” Is that really the case?

|

|

| |

|

|

|

|

Vol. 4, Iss. 5

May 20, 2015

Come On. Who Doesn’t Love A Good “Use Of An Auto” Case

|

|

|

Cases involving whether injury arises out of the “use of an auto” – for purposes of triggering an Auto or UM/UIM policy or the applicability of a CGL or homeowner’s policy’s auto exclusion -- have a way of involving strange facts. See Roque v. Allstate Ins. Co., Colorado Court of Appeals, Jan. 19, 2012 (exiting your car and hitting another motorist with a golf club did not qualify as use of an auto for purposes of a UM policy).

And this is not surprising. After all, since automobiles are designed with a clear purpose in mind, what’s “use of an auto” shouldn’t be all that hard to figure out. So, if “use of an auto” is being litigated, then it’s probably because the claim involves something more than a person simply sitting behind the wheel, motoring down the road, minding their own business, en route to Point B. These “use of an auto” cases are also legion. Again, not surprising, since automobiles are so prevalent, on a daily basis, in so many people’s lives.

Here are some cases, indeed from just the past few years, where the facts caused wonderment whether they involved “use of an auto.” The last one is the most recent – from just over a month ago.

Colon v. Liberty Mutual Ins. Co., New Jersey Superior Court, App. Div., Jan. 20, 2012 (automobile driver that bit police officer on the arm during a traffic stop did not qualify as use of an auto for purposes of a homeowners policy) (extra tidbit -- upon being stopped driver gave her name to the officer as Beyonce Knowles).

Sunshine State Ins. Co. v. Jones, Florida Court of Appeal, Jan. 18, 2012 (grabbing the steering wheel to annoy your girlfriend, while she is driving, did not qualify as use of an auto for purposes of a homeowners policy).

Hays v. Georgia Farm Bureau Mut. Ins. Co., Georgia Court of Appeals, Feb. 14, 2012 (using a pick-up truck and a pulley system, in attempting to lift a portable toilet onto the top of a deer stand, qualified as use of an auto for purposes of a homeowners policy).

National Casualty Co. v. Western World Ins. Co., 5th Circuit Court of Appeals, Feb. 3, 2012 (injury to an individual, while being placed into an ambulance, qualified as use of an auto for purposes of an automobile policy).

Colony Ins. Co. v. Comprehensive Rehabilitation Centers, Eastern District of Michigan, December 21, 2011 (automobile passenger that opened the rear door of a van and jumped out, while it was travelling greater than 50 mph, qualified as use of an auto for purposes of a CGL policy).

New London County Mutual Ins. Co. v. Nantes, Supreme Court of Connecticut, Feb. 21, 2012 (individuals that suffered neurological injuries, on account of exposure to carbon monoxide from a car that was left running overnight in a garage, qualified as use of an auto for purposes of a homeowners policy).

Lancer Ins. Co. v. Garcia Holiday Tours, Supreme Court of Texas, July 1, 2011 (exposure of bus passengers to bus driver’s tuberculosis did not constitute use of an auto under bus company’s automobile policy).

Allstate Ins. Co. v. Reyes, New York App. Div., Aug. 7, 2013 (injuries sustained by a woman who walked in front of a parked vehicle, and was bitten on the breast by a rottweiler that extended its head from inside the vehicle, did not arise out of the ownership, maintenance, or use of an underinsured vehicle).

And now the latest entrant into the family of unusual “use of an auto” cases:

In State Farm v. Beauchane, Minn. Ct. App., Apr. 6, 2014, the court addressed coverage for Justin Beauchane, who left his pickup truck (insured) in the middle of the street tied to a tree that he wanted to pull down. A motorcyclist swerved to miss the rope and struck Beauchane’s Chevy Blazer (uninsured), which Beauchane had just moved out of the tree’s path. The court held that coverage was owed under Beauchane’s policy on the pick-up truck because the injury arose from the use of the pick-up.

|

|

| |

|

|

|

|

| |

|

|

Bar’s Policy That Excludes Assault & Battery Is Not Illusory

It is not surprising that a bar owner, who did not pay a lot of attention to the ins and outs of his insurance, would be surprised to learn that his commercial general liability policy contained an Assault & Battery exclusion, as many do. That’s what happened to a tavern owner in Tennessee, who was sued for wrongful death, when a patron was beaten to death in the parking lot of his establishment. The tavern owner argued that, between the Liquor Liability exclusion [version in a standard CGL policy] and A&B exclusion, the coverage was illusory because it would not pay benefits under any reasonably expected set of circumstances. As he saw it, “common sense dictates that customers visit a tavern to drink alcohol and it is reasonably foreseeable, and expected, that intended injuries arising out of a fight on the premises would take place.” The court disagreed. Atlantic Casualty Inc. Co. v. Norton, No. 12-650 (E.D. Tenn. Mar. 23, 2015).

|

|

| |

|

|

|

|

|

|

|

|

|

|

|