|

|

|

|

|

|

Vol. 7 - Issue 2

March 7, 2018

|

|

|

|

|

|

|

|

| |

Check out this brief video of Governor Pataki discussing his interview with Randy |

| |

I knew going in that George Pataki was six-six. But that still didn’t keep me from being startled by the former New York governor’s height when I saw him standing outside his office. No wonder Dewey Ballantine won the lawyers’ basketball league championship three out of four years that Pataki was on the team in the early 1970s. The former governor still plays, he told me, even if his step is slower. “My jump shot is now a set shot and I haven’t dunked. If I tried to dunk I would end up in the emergency room.”

George Pataki learned how to play basketball growing up on his grandparents’ twelve-acre farm in Peekskill, New York, 35 miles north of New York City. But throwing a ball through a bent hoop, with no net, and picking corn at age ten, are hardly all that Pataki learned there.

I visited the former three-term Republican governor at his office, at Norton Rose Fulbright, in Midtown Manhattan, to ask him about a quarter century in politics and nearly a half century as a lawyer. An hour later I left sure of one thing. Despite the importance of his two careers, he is defined by neither.

Sitting at a small work table in his corner office, Pataki, 72, has a warm and folksy manner. He’s unscripted. His answers match my questions. Nothing like a politician. Pataki has a great sense of humor. It was on display when I asked him if he knew how to use the office photo copier.

|

| |

|

| |

The Son Of A Bootlegger

The Pataki farm was a family compound. It was purchased by his paternal grandfather after he emigrated from a small town in Hungary. Barely eking out an existence it served as home to Pataki, his brother, parents, both sets of grandparents, nine aunts and uncles and twelve cousins. The twenty-nine family members lived in six houses spread around the farm. It was a unique experience, Pataki told me. “My cousins are still like brothers and sisters.”

From his father’s side Pataki learned the importance of hard work and forward planning, as is the life of a farmer. When it comes to farming, Pataki told me, “there are no short cuts.” It was a whole different ballgame on his mother’s side. His maternal grandfather moved “from one moneymaking scheme to the next – not all of them within the boundaries of the law,” Pataki described him in his self-titled autobiography. This included a distillery that he set up in the tub during Prohibition. Pataki laughed as he told me that at age six his mother was “putting Gordon’s Gin labels on the bottles.”

I asked Pataki about this curious combination that makes up his DNA. But he didn’t see it as so unusual. “In a sense, it is typically American because Americans have that diversity in most of our backgrounds. And hopefully it leads us to have the best of all these different traits come together.”

One of Pataki’s favorite farm stories is his father’s annual effort to corner the local tomato market. Every year he planted tomatoes in early April, six to eight weeks before everyone else, knowing that the plants were likely to succumb to an inevitable frost. However, if they survived, he’d be the only one selling tomatoes for a time. But, despite Pataki and his father covering every plant with plastic and baskets, Lucy always pulled the football away.

Pataki’s father did not become a tomato magnate, but the lesson of planting tomato’s in early April stayed with Pataki. Whether it’s in law or politics, he told me, “you keep trying to do something that others think can’t be done. Often times they are right, but there comes that exceptional time when you do something no one else thought was possible. And when you accomplish that you can change things in a way that, by simply going along with conventional wisdom, you never have the chance to do.” But Pataki hastened to add “so long as you don’t bet the ranch on it.”

From Farmer To Wall Street Lawyer

Pataki made his way to Yale University, where he started out as a science major. But then he “discovered beer and politics,” he told me. And unlike a history or English course, he explained, that he could do in one night, “quantum physics you couldn’t quite do in one night. So I switched my major.”

Yale was followed by law school. Pataki had fallen in love with political debate and political ideas and he explained that “having an understanding of the law really mattered to me as being able to do that better.” But he was also looking to the future: “The thought arose that maybe someday I’ll run for office. And being a New Yorker, going to law school in New York, would be something that probably made a great deal of sense.”

Pataki entered Columbia Law School in 1967. At that time, societal debates and protests, even violent, were the order of the day. Some named the lounge outside the library the Pataki Memorial Lounge, on account of his constant presence there, discussing issues. Pataki called Columbia a “crazy time,” describing it as “having the most radical campus in the country.” “Everything you believed in,” he told me, “every fundamental view that you thought everybody else accepted, often times nobody else did. It made you rethink and it challenged you and that’s always a good thing.”

Following graduation Pataki landed at Dewey Ballantine in New York City. His annual salary, $15,000, was three times that of his mailman father. But Pataki quickly realized that being a Wall Street lawyer wasn’t in his makeup. He had come from a place where a handshake was as good as a contract. He wasn’t good at thinking in terms of how the other side can take advantage of you. “I loved Dewey,” he told me, but it wasn’t the right fit: “I like to trust people. I don’t like to be cynical. A lawyer always has to consider the possibility of someone not acting in good faith. Growing up on that farm that wasn’t the way it was.”

Ironically, Pataki would return to Dewey’s office. The firm was named for Thomas Dewey, New York’s Governor from 1943 to 1954.

The Transition To Politics

Pataki, now with his wife, returned to the family farm – to a house with no heat or toilet – and the life of a small-town lawyer. He also began to think about the possibilities of state government. His first foray was as a member of a joint legislative task force on court reorganization. It was instrumental in the passage of a constitutional amendment providing for the New York Court of Appeals, the state’s highest court, to be comprised of appointed, and not elected, members. Ironically, Pataki was, unknowingly, creating a future responsibility for himself. As Governor, he would appoint six judges to the court.

I kidded Pataki that his task force should have also taken the opportunity to correct New York’s goofy and confusing court names – where the Supreme Court is the trial court and has justices, while the highest court is the Court of Appeals, served by judges. “It’s so backwards,” he agreed. We joked about the waste of words it creates -- every time a news story writes New York Court of Appeals, it has to add “the highest court.” But “I think it’s here to stay,” he concluded.

Despite once having felt an excitement for the public service possibilities offered in Washington, Pataki turned his attention locally, where “decisions made at the state level had a direct impact on people’s lives.” He served as Mayor of Peekskill from 1981 to 1984, and then eight years in the New York State Assembly followed by two in the New York Senate.

I told Pataki that I figured out the real reason why he decided to turn away from the law in favor of politics. He gave me a look that said -- bring it on. It can all be found, I explained, in a 1978 decision from the Eastern District of New York called Bohack Corp. v. Borden, Inc. Pataki represented a creditor who lost in Bankruptcy Court and appealed to the District Court. The decision is eye-glazing. It had something to do with the doctrine of set-offs under Chapter 11 of the Bankruptcy Code. I can barely figure out who won. [Pataki didn’t. He was now 0-2 in the case; but prevailed before the Second Circuit.].

I pointed out to Pataki that the decision, which discussed an English statute dating back to 1645, as well as tracing the history of a U.S. statute starting from 1800, is so deadly dull that it would make anyone switch to inactive status.

Pataki remembered the case like it was yesterday. “I won that case and I changed the law!” he declared, adding that the decision went on to be an important precedent. “I was sure that the court was wrong.” He saw my point about the decision being dry, but I have it all wrong. “I loved that case. One of the reasons was I wasn’t with a big firm. There were only four or five of us so I had to do the whole thing. And history and intellectual development has always been fascinating to me. So the idea of going through that. I loved the Bohack case.”

Ironically, the District Court decision includes a passage from Justice Benjamin Cardozo in a U.S. Supreme Court opinion. Cardozo sat on the New York Court of Appeals, New York’s highest court, before heading to Washington. Once again, there’s a foreshadowing of Pataki’s future involvement with the Court of Appeals.

The Governor’s Office

In 1994 Pataki entered the race for New York Governor. It was a task as tall as a corn stalk. He was, as The New York Times called him then [on page B.4], “a little-known Republican lawmaker from Putnam County.” His opponent was the state’s political Goliath -- three-term Democratic Governor Mario Cuomo. Not to mention that New York had two million more registered Democrats than Republicans. Pataki’s platform was tough on crime (bring back the death penalty) and tough on spending. He defeated Cuomo by two percentage points. Pataki went on to serve two more terms as the state’s chief executive. He was at the helm in the State’s response to the September 11, 2001 terrorist attacks (Rudy Giuliani called him a “total partner”) and played an important role in the redevelopment of the World Trade Center site and building of the 9/11 memorial.

But something doesn’t make sense. Pataki made the decision to leave Dewey Ballantine when he realized that corporate law wasn’t suited to someone who liked to trust people and didn’t grow up considering the possibility of someone not acting in good faith. But if such idealism wasn’t right for Dewey, how did he handle New York politics all those years? After all, New York’s capital is well-known for being pretty rough and tumble. Nobody is going to confuse Albany for Mother Teresa’s place in Calcutta.

I asked Pataki about this seeming inconsistency. But he didn’t see it the way I did. “It wasn’t that hard,” he told me, “because you know principles you believe in and other people don’t agree with those principles or agree with the principles but for whatever political reason won’t support those principles and you just try to figure out the motivation of people. When you believe in something it is pretty easy to do your best to try to advance that belief.”

From Howard Stern To Oprah

Let me ask you about Howard Stern. “My opponent,” Pataki replies.

Pataki’s first run for Governor could have easily been derailed by the brash radio show host. In 1994 Stern entered the Governor’s race as the Libertarian Party’s nominee. His campaign platform was simple – he favored the death penalty and wanted road construction to be performed at night. Stern’s plan was to accomplish these things and then resign, turning the state over to his lieutenant governor. The radio host gave speeches, raised money and got tremendous press coverage. But, most concerning for Pataki, he was polling at ten to twelve percent. Pataki’s contest with Cuomo was surely going to be very close. It is likely that Stern would have siphoned off enough Pataki votes to hand the race to Cuomo.

Thankfully for Pataki, Stern dropped out -- to avoid having to comply with the state’s financial disclosure laws -- and endorsed Pataki. While on the campaign trail the would-be Governor constantly heard from people that Stern’s support was the reason they would be pulling the lever for him. With Pataki’s thin margin of victory over Cuomo, what Howard Stern could have taketh from Pataki he probably ended up handing him.

Twenty-plus years later Pataki would run for President and come-face-to face with another candidate who, like Stern, was a brash celebrity, enjoyed tremendous media coverage and owed his success to connecting with disaffected voters. Now there’s talk, at least by some, of Oprah Winfrey throwing her hat into the 2020 Presidential ring. I asked Pataki if the “celebrity candidate,” who can monopolize the media airways, is the “new normal” for politics? “I certainly hope not,” he said. “While political experience can be a negative in the public’s eyes, Pataki acknowledged, “I hope that people now don’t disqualify someone because of that and look for the celebrity candidates, but [instead] look at the person’s philosophies and principles.”

Criticizing And Shaping The New York Court Of Appeals

Shortly after taking office as Governor, Pataki took aim at the New York Court of Appeals. In particular, he criticized the court’s decisions in criminal cases that he thought overturned convictions based on the defendant’s denial of rights that he considered technicalities. He called some decisions “irrational, mindless, procedural safeguards – not for those who are wrongly charged but for criminals who can get off.”

Pataki told me that he was “critical of junk justice because the most important thing the government does is provide for the safety of its people. And New York State was failing at that. And it was failing for a lot of reasons. One of which was the abandonment of common sense in the application of the law by courts from the trial courts to the Court of Appeals and that had to change.”

Pataki’s criticism of the Court of Appeals made the well-publicized 2010 State of the Union incident, between President Obama and Supreme Court Justice Samuel Alito, over the Citizens United decision, look like a Tupperware party.

Given how harsh his attack, was Pataki worried that it could backfire? Judges are still human. Might they retaliate and double down? No, Pataki told me, he did not have this concern: “I have great faith in people and I wasn’t calling them out personally. I was criticizing the logic behind their decisions and their, in my view, abandonment of the appropriate interpretation of law. So I thought that to criticize people, based on an intellectual analysis, as opposed to, ‘you’re a jerk,’ is something I thought, if you are a judge of that caliber and that stature, you should be able to listen to that.”

On the subject of Pataki’s Court of Appeals appointments, I shared with him a 2014 law review article, from Albany Law Review, where New York lawyer Benjamin Pomerance devoted a staggering 36,000+ words to analyzing Pataki’s high court selection criteria. Given Pataki’s harsh criticism of the Court, Pomerance’s focus was on the role that a candidate’s likelihood to be pro-prosecution played in his or her selection. Pataki was unfamiliar with the article and seemed dubious that someone could figure out what was in his mind. I read the article’s conclusion to him: “A tendency towards supporting the prosecution in criminal cases and a firm stance in favor of the death penalty certainly augmented the likelihood of receiving Pataki’s favor. However, a lack of information in either of these categories certainly was not fatal to the individual’s chances of appointment either.” “I’m impressed,” Pataki said of Pomerance’s work. “That’s pretty accurate.”

Pataki’s Current Practice

Pataki’s current practice at Norton Rose has an energy and environmental focus. He described his firm as having “the best green energy practice in the country by far.” Environmental issues are nothing new to Pataki. As Governor, he championed numerous environmental initiatives, including many associated with cleaning up the Hudson River.

Environmental causes are not usually associated with Republicans. But, for Pataki, it was personal. As a kid, living near the Hudson River, he saw first-hand its polluted condition. “It would be summer in the Hudson Valley, 95 degrees, 95 percent humidity,” he told me. “And there would be all this water and you couldn’t go in. It was just something you wondered how this happened and fortunately I had the chance to try and do something about that and we did.”

The Office Copier

Between growing up on a farm, and spending twelve years in the Governor’s office, where I’m sure Pataki had a few assistants around, I’m curious if he can handle one of the most important tasks required of a lawyer – the office photo copier. It should be on the bar exam.

Pataki paused for a few seconds - I could see him thinking -- and finally said “no.” But, he was quick to add, “I can probably figure it out.” I told Pataki that I wouldn’t ask my follow-up question – can he fix a paper jam? He shouted through his closed door: “Amy, can I fix a paper jam in the copier?” A voice from the other side came back: “no.”

As Pataki was showing me out he walked around to his assistant’s area and pointed to a large button on a machine on her desk. “I just push this button here,” he declared. “Actually, Governor, that’s the printer,” I informed him. “Ah.”

Once A Farmer…

Pataki’s office is most notable for what it’s lacking – photos of himself with Presidents, world leader and A-list celebrities. Surely Pataki’s walls could resemble the old Carnegie Deli. But he’s just not interested in that he told me. Instead the photos in his office are devoted to his family. And, of course, he showed me one of the farm in Peekskill.

Sadly, Pataki told me, the farm had to be sold to assist with the education of his four children on a government salary. But he has since purchased a farm on Lake Champlain. “I try to get up there as much as possible and get out there and work and do stuff.”

Despite going on to practice law in the big city nearby, and spend twelve years running one of the most important states in America, George Pataki never stopped being a farmer from Peekskill. “That’s who I am.”

As New York’s Governor, George Pataki held a job with no term limits. The same can be said of his life as a farmer.

|

|

| |

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Vol. 7, Iss. 2

March 7, 2018

Insurance Company Spokespeople That Actually Make Sense

|

|

|

|

|

| |

Next week the NCAA Men’s Basketball Tournament will be in full swing. Besides the players on the court and fans in the stands, your television will also show lots of team mascots and their shenanigans. There will be giant heads of every size, shape and stripe. You’ll see Clemson’s adorable tiger, who looks like Tony the Tiger’s brother. The Michigan State Spartan will be there, as long as he’s not in court fighting a copyright suit by USC’s Trojan. Duke’s masked Blue Devil, who is disliked as much as Duke, will also be in attendance.

While mascots are usually associated with sports, there are plenty in the insurance world too. They are probably better called spokespeople, but their purpose is similar. You know who there are. Their companies have spent billions of dollars over the years to make sure of it. I enjoy the characters that some insurance companies have developed over the past few years to promote their brands. I love the Gecko -- and follow him on Twitter. Allstate’s Mayhem Man keeps my interest. I’m a big fan of the Farmer’s Guy and have thought about getting that tweed jacket and vest combination. And as long as we’re on the subject…. Progressive’s Flo is getting a little long in the tooth. It’s time for her pension to vest.

But what I find curious about these insurance spokespeople is that they have no connection to insurance. What does a talking lizard have to do with auto insurance? Snoopy is the Fonz of dogs, but I don’t think about life insurance when I see him on the Met Life blimp.

Wouldn’t it make more sense for insurers to use characters whose appearance actually have a connection to the insurance policy that they are trying to sell. Consider these insurance spokespeople that insurers should be using:

Take an insurer trying to sell high level excess policies. If I saw the Jolly Green Giant I would definitely think to myself – You know, maybe I should buy coverage excess of $50 million.

And who better to sell the $1 million primary policy in that new $100 million tower? The Oomph Loompahs of course.

And what about a spokesperson for car insurance that actually has something to do with cars? Kitt from Knight Rider can talk and he probably isn’t too busy these days. Give him something more to do than just sitting around Hoff’s driveway.

Fire insurance policies? “Hi there, this is Smokey the Bear for Fire Mutual. You shouldn’t play with matches, but, if you do…."

If McGruff the Crime Dog told me to buy a fidelity policy I couldn’t sign up fast enough.

Bob the Builder was born to hawk builder’s risk policies.

If a company can’t sell life insurance with the grim reaper as its spokesperson then it should get out of the business.

Travel Insurance – Waldo (of Where’s Waldo fame) should be all over that!

Flood Insurance – So easy. Noah

Pet insurance? Scooby Doo is perfect with all that hijinks he and Shaggy get into. And you could get him for practically nothing. He would take payment in Scooby Snacks.

If Goofy can’t sell professional liability policies, who can?

If you are trying to sell pollution liability policies there could be no better spokesperson than a guy who has spent his entire life in a trash can. Get me Oscar the Grouch on the line |

| |

That’s my time. I’m Randy Spencer. Contact Randy Spencer at

Randy.Spencer@coverageopinions.info |

|

|

| |

|

|

|

|

Vol. 7, Iss. 2

March 7, 2018

The King Reads Coverage Opinions

|

|

|

|

I have always said that Coverage Opinions has a diverse readership. Meet GCH CH Maplewood’s Blue Suede Shoes At Piccino. Or, as he’s known to his close friends, Elvis.

Elvis was the “Best of Breed” winner for Italian Greyhounds at the venerable Westminster Kennel Club Dog Show held last month in New York City. As “Best of Breed,” Elvis appeared on the show’s prime-time broadcast, vying to win the Toy group category. Here is the king of Italian Greyhounds – with breeder--handler Marcy Caton, of Maplewood Italian Greyhounds in Phillips, Maine -- strutting his stuff on the floor of Madison Square Garden |

| |

|

| |

When Elvis isn’t sniffing the spot where Ali-Frazier’s Fight of the Century took place, he likes to sit back, chew on a bone and catch up on the latest in insurance news from Coverage Opinions. Elvis is a long-time CO reader. His favorite cases are about notice. After all, Elvis loves to tender!

Congratulations Elvis! |

| |

|

| |

| |

|

|

|

| |

|

Vol. 7 - Issue 2

March 7, 2018

Thisclose: The 4th Edition Of “Insurance Key Issues”

New Edition To Be Released Any Day Now

|

|

|

|

| |

|

I had been hoping for an end-of-February release of the 4th edition of General Liability Insurance Coverage – Key Issues In Every State. But, alas, as sometimes happens in the book publishing world, there was a delay – but ever so slight. I am confident that the 4th edition of Key Issues will be available for sale on Amazon any day now. The proof copies are on my desk.

Look for an email announcement very soon. Thanks for your patience.

|

| |

|

|

| |

|

|

|

|

Vol. 7, Iss. 2

March 7, 2018

Making Easy The Coverage Issue That “Would Tax Socrates”

|

|

|

|

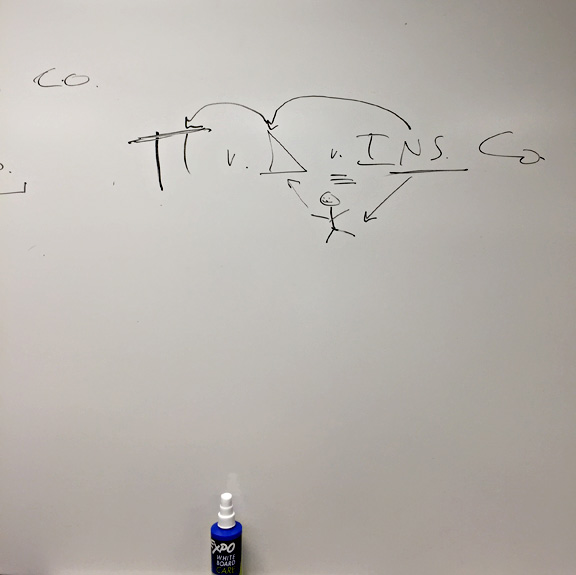

I recently took up the issue of the tri-partite relationship with the students in my insurance coverage class at Temple Law School. This semester has been my first foray into teaching insurance to law students. It’s been a neat experience. My objective has been simple – OK, you guys had Torts. You learned about finding someone liable. Now, let’s talk about the real issue – where’s the money going to come from to satisfy that judgment?

I was concerned about tackling the tri-partite relationship with the students. After all, it has a reputation for being pretty complex. The Mississippi Supreme Court put fear in me with Hartford v. Foster (1988), saying this about the tri-partite relationship: “The ethical dilemma thus imposed upon the carrier-employed defense attorney would tax Socrates, and no decision or authority we have studied furnishes a completely satisfactory answer.” And then there’s Finley v. The Home Ins. Co. (Haw. 1998) which had this to say about the tri-partite relationship: “The magnitude of the difficulty in resolving the issue is reflected in the volume of litigation nationwide, and, in the instant case, the number of amicus curiae briefs representing divergent views.”

So it was with trepidation I entered classroom 7B at 10 A.M. on a recent Monday and took a deep breath. But, to be honest, it wasn’t so tough. I don’t see what all the fuss is about. I drew a simple picture on the board and, viola, this supposedly super-duper complex concept was as easy to explain as a hot knife through butter. If Socrates owned a magic marker he would have been fine. |

| |

|

| |

|

|

|

|

Vol. 7, Iss. 2

March 7, 2018

Oh, Canada! Toronto Court’s Unique Foul Ball Injury Case

|

|

|

|

Regular readers of this publication (and I thank you for that) know that I have a soft spot for cases involving fans seeking recovery for injury sustained by being hit by a foul ball (or a tossed-into-the-stands hot dog) at a baseball game. The fans virtually always lose on account of the so-called court-created “baseball rule.” The baseball rule generally provides that a baseball stadium operator is not liable for a foul ball injury as long as it screens the most dangerous part of the stadium and provides screened seats to as many spectators as may reasonably be expected to request them.

But despite the challenge of overcoming the baseball rule, many injured fans still try. The cases generally involve an effort to find an exception, of some sort, to the rule.

My thanks to CO reader, and Toronto coverage lawyer Michael Teitelbaum, of Hughes Amys, LLP (author of “Ontario Insurance Law & Commentary” (2018)) for sending me a copy of the Ontario Superior Court of Justice’s late January decision in Legacy v. The Corporation of the City of Thunder Bay. It is a baseball injury case, but unlike any I’ve ever seen.

Lorrinda Maureena Anne Legacy was driving past Port Arthur Stadium, in Thunder Bay, Ontario, when her driver’s side window shattered. An object hit her head. She pulled over and discovered a baseball on the floor of her car. The baseball had been hit from inside the stadium during batting practice. [I have dreamed of catching a foul ball at a baseball game. I’d even take it this way.]

Ms. Legacy filed suit. But here’s the rub. The stadium was the home ballpark for the Thunder Bay Border Cats. However, the ball had been hit by a player on the visiting team – the Deluth Huskies. The Huskies argument was that a visiting baseball team cannot be liable for injury caused by a baseball being hit out of the home team’s stadium. The opinion does not say this specifically, but, surely, the argument is that a visiting team has no duty to maintain or operate the stadium to keep fans or someone like Ms. Legacy safe. The Huskies cited a House of Lords decision stating that “playing baseball is not a tort.”

I’ve never seen this “visiting team” issue raised in a foul ball injury case. Maybe because it’s so obvious that the visitors are not liable, even if a visiting player hits the foul ball that causes injury. And maybe that will be the outcome here. But the court concluded that it was premature to make that decision. The City (the owner of the stadium) and the Huskies had not yet delivered statements of defence (Canadian spelling – and my spell check gives me the squiggly red line to tell me I’m an idiot).

The court noted a couple of peculiarities about the case that could serve as basis to find liability on the visiting Huskies. First, the protecting netting had large gaps or holes in it. Second, the visiting Huskies players were allegedly hitting balls from third base and not home plate. Based on these circumstances, the court concluded as follows:

“If the Duluth Huskies players knew that they were hitting baseballs out of the stadium onto a busy city street because, for example, the protective netting which was obviously there to prevent such a mishap, was, to their knowledge, rendered ineffective because of gaps or holes, could they be liable?

If the Duluth Huskies were hitting balls out of the park from the vicinity of third-base, rather than home plate, rendering the stadium safety design features ineffective because of their choice of batting position, could they be liable?

These scenarios are within the allegations of negligence pleaded by the plaintiff and may be sufficient to trigger a duty of care.”

The court did not discuss the baseball rule or something similar. I do not know if it’s as difficult for a plaintiff to prevail in a foul ball injury case in Canada as it is in the U.S.

Legacy is an usual case because it involves a claim against a visiting team. And even if that should be an easy no-liability situation, it may be that, with facts like these, liability can be found on the visitors. |

| |

| |

| |

|

|

|

|

Vol. 7, Iss. 2

March 7, 2018

Postscript: Domino’s Pizza Carryout Insurance

|

|

|

|

In the last issue of Coverage Opinions I poked fun at Domino’s Pizza’s “Carryout Insurance Program.” As the pizza chain has been touting in television ads of late, it will replace a carryout customer’s pizza that is somehow damaged on the way home.

It’s a silly idea, of course. But that’s the point. It’s a fun gimmick. But, apparently, not everyone got that. Cathy O’Neill, founder of an algorithmic auditing company (whatever that means) had this to say about the Domino’s offer in a Bloomberg “Viewpoint” piece titled “No, Thank You, I Don’t Want to Insure My Pizza”: “The winner of my personal stupid prize [for recent television commercials that she has seen]: Domino’s ‘pizza carryout insurance,’ which offers a free replacement if you somehow manage to destroy your pizza on the way home. This is just the latest in a long line of products that distort people’s understanding of what insurance should be. Somebody has to put their foot down, and that somebody is me. Let’s remind ourselves what insurance actually is. It’s protection against calamity. It’s something that pays out only in unusual circumstances — and sometimes never — but definitely only when you would not be able to afford the loss.”

Jeez Louise, take it easy Cath. [Can I call you Cath?] It’s a joke. A PR stunt. And it worked. Domino’s got me to talk about their pizza. And you. And now me again.

Ms. O’Neill goes on to rail against what she calls “so called insurance” -- products where the premium is too high relative to the risk transferred, such as for an iPhone. Maybe she’s right about some of that. But she lost me at “[i]f you can buy a pizza, pretty much by definition you can afford the loss of a pizza. You don’t need insurance.”

Get a slice, Cath.

|

| |

| |

| |

|

|

|

|

Vol. 7, Iss. 2

March 7, 2018

It’s Still Going: That Crazy Cosgrove Case

|

|

|

|

Last summer an Arizona federal district court issued Cosgrove v. National Fire & Marine Insurance Company. The court held that insurer-appointed defense counsel, in a reservation of rights-defended case, used the attorney-client relationship to learn that his client did not use subcontractors on a project. When defense counsel did so, he knew, or had reason to know, that his client’s policy contained a Subcontractor Exclusion and that the insurer may attempt to deny coverage based on the exclusion. Thus, the court held that the insurer was estopped from asserting the Subcontractor Exclusion as a coverage defense. The court reached this decision despite the existence, or not, of subcontractors being a pretty routine, and obvious, and not secret, fact in a construction dispute.

Needless to say, this was a very troubling decision for insurers (and appointed defense counsel). Very shortly after the court’s decision the parties settled. As part of the settlement, the court agreed that it would vacate and seal the summary judgment decision. Sure enough, you can’t get the decision on Pacer and the insurer arranged for it to be removed from Lexis and Westlaw. I have a copy of the decision. I’m happy to send it to you. Just promise to bake me a cake with a file in it.

As I reported in the December issue of Coverage Opinions, on November 3rd, the policyholder advocacy group United Policyholders filed a Motion to Intervene to unseal and reinstate the decision. UP said in its brief that what the insurer did was an “impermissible tactic” – one “commonly employed by insurers in an attempt to reshape case law in their favor after an adverse ruling.” UP says that the insurer, faced with an adverse decision, is “seek[ing] to hide the court’s opinion.” The insurer filed a response, providing many reasons for denial of intervention – UP has no standing; the case is over; the judge agreed to vacate and seal the decision as a condition of settlement; the various requirements of the Intervention rule have not been satisfied….

Update: On January 18th the court, in a five and a bit page opinion, denied UP’s motion to intervene, citing such reasons as lack of jurisdiction, it is not a party to litigation that shares questions of law or fact to the case, untimeliness and prejudice to the parties.

Update 2: On February 8th UP filed a notice of appeal to the Ninth Circuit. Maybe the known-for-being-liberal Ninth Circuit will be sympathetic to UP’s objective here. But it seems UP chose a difficult test case given the delay in intervention. |

| |

| |

| |

|

|

|

|

Vol. 7, Iss. 2

March 7, 2018

Encore: NCAA Tournament And Courts (Of Law)

|

|

|

|

[This article appeared in the March 22, 2017 issue of Coverage Opinions. It is republished here, with minor changes to account for its timing now versus then.]

If you are reading this, then, at this moment, you have temporarily stopped working on your algorithm to fill out your NCAA Tournament bracket next week. And once the Tournament starts you’ll be ruminating over the fact that Gladys from H.R. is in first place in the office pool – despite that she spelled Xavier with a Z and has never heard of Gonzaga.

It is not surprising that, given the money involved, the NCAA Men’s Basketball Tournament has been the subject of some legal disputes, especially involving intellectual property rights.

Jason Gay, sports columnist for The Wall Street Journal, recently reported that the NCAA is not happy with USA Gymnastics for wanting to use “The Final Five” for its gold medal winning team from the Rio Olympics. As Gay put it: “You know, because Final Five sounds like Final Four.” The NC2A is also less than pleased with the Big 10 Conference wanting to trademark the phrase “March is On!”

Gay himself came up against the NCAA’s don’t-mess-with-us attitude in 2014 when, while covering the East regional final at Madison Square Garden, between Connecticut and Michigan State, he violated the NCAA’s “cup policy.” As he recounted in a wonderfully entertaining column, the NCAA forbids outside cups at tournament games and requires that beverages be consumed in official NCAA cups. Gay, aware of this policy and looking to wage a small protest – and, no doubt, have some fun with it -- drank a beverage from a coffee mug he brought along featuring eleven illustrations of cats. He was approached by a tournament staffer who made a subtle threat that, on account of Gay’s cat mug, the Journal could be denied credentials to cover the Final Four the following weekend. Gay was forced to turn over the mug. It was returned to him after the game.

The NCAA Men’s Basketball Tournament in fact shows up in cases that have nothing to do with the Tournament. This too is not surprising, given the hold that the tournament has on the public consciousness. Consider these judicial opinions where the NCAA Tournament made an appearance on a different kind of court than basketball.

In People v. Evans, 2011 Cal. App. Unpub. LEXIS 2648 (Cal. Ct. App. Apr. 12, 2011), the California Court of Appeal held that the trial court did not commit error when explaining to a jury how it may use its common sense – despite there being no evidence of a fact presented. The trial court gave as an example someone accused of theft of jewelry in April whose defense was, at the time of the theft, he was home watching the NCAA basketball tournament -- March Madness. The court explained that the jury could use its common sense in assessing the testimony, even though nobody introduced evidence of the dates of the tournament.

In Urofsky v. Gilmore, 216 F.3d 401 (4th Cir. 2000), the Fourth Circuit Court of Appeals upheld the constitutionality of a Virginia statute to the extent that it precluded professors of public colleges and universities from accessing sexually explicit materials, on state-owned or leased computers, for work-related purposes. The dissent saw it differently, noting that “[t]he Commonwealth has not explained, and cannot possibly explain, why employees who access sexually explicit material are any less ‘efficient’ at their work than employees who check espn.com every twenty minutes during the NCAA tournament.”

In Pirschel v. Sorrell, 2 F. Supp. 2d 930 (E.D. Ky. 1998), the court upheld the suspension of a student found in possession of beer while attending a basketball tournament at another school. The court looked at the impact that a school’s players can have on its team’s reputation and applied that conclusion to the team’s fans: “While a school may reap the benefits of a successful team and well-behaved fans, it may also be strapped with a negative label in the event its teams display poor sportsmanship. For example, most, if not all, University of Kentucky basketball fans recall Duke University star Christian Laettner stepping on a Kentucky player’s chest during a NCAA tournament game. Although that incident took place several years ago, many still consider Duke a dirty team.” Likewise, the court observed, “[j]ust as a school may be labeled as having excellent students based on others’ perception of their conduct, a negative reputation will result if students’ behavior is unbecoming.”

In Stainbrook v. Kent, 771 F. Supp. 988 (D. Minn. 1991), the parties agreed that serving a summons and complaint upon LSU, by delivering the documents to its assistant to the athletic director, while the LSU men’s basketball team was competing in the regional final of the NCAA tournament, did not constitute proper service.

Meinke v. VHK Genesis Labs, 2006 U.S. Dist. LEXIS 85664 (N.D. Ill. Nov. 21, 2006) involved employment-related claims brought by a sales employee who worked in the field and from home. He was directed to report to the company’s offices on March 18, 2004. When the employee did not show up, his boss called and told him to turn off the NCAA basketball tournament. He denied that he was watching the tournament at the time.

Denial – That’s my advice to you. |

| |

| |

| |

|

|

|

|

Vol. 7 - Issue 2

March 7, 2018

|

|

|

|

|

|

|

There is a lot to a commercial general liability policy. But its most fundamental aspect, hands down, no argument to the contrary, is that it provides coverage for “accidents.”

Yet, despite this, there is no general liability coverage issue that is litigated more frequently than “what is an accident?” The reason – nobody can agree on what’s an accident. But how is that possible? How can the very essence of a liability insurance policy not be understood by all concerned? Admittedly, I’m not saying anything novel here. Fifty-plus years ago the Pennsylvania Supreme Court made this same observation in Brenneman v. St. Paul F. & M. Ins. Co. (Pa. 1963):

“Everyone knows what an accident is until the word comes up in court. Then it becomes a mysterious phenomenon, and, in order to resolve the enigma, witnesses are summoned, experts testify, lawyers argue, treatises are consulted and even when a conclave of twelve world-knowledgeable individuals agree as to whether a certain set of facts made out an accident, the question may not yet be settled and it must be reheard in an appellate court.”

The question whether something was caused by an “accident” gets the nod as the longest running insurance coverage issue (in conjunction with more recent “expected or intended” exclusion cases, which can overlap liability policy “accident” cases).

The earliest American insurance case that I could find, addressing whether an “accident” took place, is Howell v. Cincinnati Ins. Co., from the Ohio Supreme Court in 1835. At issue was coverage for a boat that sank. [The “accident” issue arose in coverage disputes before the advent of liability insurance.]

And some ancient “accident” cases seek guidance from even more ancient cases, often times English ones with strange citations that very few lawyers practicing in this country understand. The question whether something was caused by an “accident” has been keeping judges, including ones in wigs, busy for a very long time.

But it’s not just that there are a lot of really old cases addressing the “accident” question. The other very interesting fact is that some of these cases look remarkably similar to ones that were decided yesterday. In other words, not only have American courts been grappling, for 180 years, with the coverage question whether injury or damage was caused by an “accident,” but some of the arguments haven’t changed much.

This brings me to a February 27th article in Law360 that addressed “what’s an accident” under California law. In “California High Court Has A Chance To Define Accident,’” Covington & Burling’s Gretchen Hoff Varner and Broer Oatis discuss Liberty Surplus Insurance Co. v. Ledesma and Meyer Construction Co. Inc., a case then to be argued before the California Supreme Court on March 6.

Ledesma involves potential coverage for claims arising out of a construction company employee’s sexual assault of a student, at a middle school, where the company had been working. In the subsequent suit by the student it was alleged that the construction company was liable for negligent hiring and supervision of the employee. At issue – whether coverage for a defense and indemnity was owed to the school district and construction company, under the construction company’s general liability policy. The insurer argued “no accident” as the employee had committed an intentional tort. However, the issue at hand wasn’t coverage for the employee’s intentional tort, but, rather, the construction company’s negligent hiring and supervision of the employee. The federal district court found for the insurer. The case went to the Ninth Circuit, which certified the issue to the California high court.

Covington’s Varner and Oatis note that California law lacks clarity on the question of what is an accident. They point to cases stating that an accident takes place “if an act or the consequences of an act are unexpected, unforeseen or undesigned.” However, the San Francisco lawyers also note that, in other California appellate court decisions, the “unexpected consequences” prong of the definition of “accident” is disregarded and the courts looks “only at the specific act that caused the injury when determining whether an accident took place.”

Noting this disparity, the authors state that Ledesma provides the California Supreme Court with “the opportunity to answer, once and for all, the following question: When insurance policies refer to an ‘accident,’ what does that mean?”

The Covington duo does a very nice job of discussing what they see as a lack of clarity, under California law, on the “accident” issue. And I agree with them that Ledesma provides the opportunity for a definitive definition of “accident” under California law. When it comes to defining things, supreme courts -- with three-part tests, balancing tests, totality of the circumstances -- are at their best.

However, even if a definitive definition of “accident” comes out of Ledesma, it will not necessarily decrease the amount of litigation over whether a certain injury or damage was caused by an accident. Accident cases flourish nationally not because the term “accident” wants for definitions. It is the application of the facts to the definition that cause the disputes. Determining whether the consequences of an act are unexpected, unforeseen or undesigned is an open invitation for disagreement.

As Justice Musmanno stated in Brenneman: “Everyone knows what an accident is…” And therein lies the problem. Whatever the legal definition of “accident” may be, its application contains an element of “I know it when I see it.”

|

| |

|

|

| |

|

|

|

|

Vol. 7, Iss. 2

March 7, 2018

Pennsylvania Policyholder Finally Cracks The Kvaerner/Gambone Nut

|

|

|

|

For the past ten-plus years the insurers’ record in Pennsylvania faulty workmanship coverage cases has resembled that of the Harlem Globetrotters. The Pennsylvania Supreme Court’s 2006 decision in Kvaerner Metals v. Commercial Union Ins. Co. and the Superior Court’s 2007 decision in Millers Capital Ins. Co. v. Gambone Bros. Dev. Co. have been a one-two punch denying coverage to policyholders for construction defects. Kvaerner held that faulty workmanship does not constitute an “occurrence” under a commercial general liability policy. Gambone subsequently held that even consequential damages of faulty workmanship does not constitute an “occurrence.”

Well, the Washington Generals finally won. The Pennsylvania Superior Court recently decided J.J.D. Urethane Co. v. Westfield Ins. Co., No. 1440 EDA 2017 (Pa. Super. Ct. Feb. 9, 2018) (unpublished). It reads like most Pennsylvania faulty workmanship coverage cases -- until you get to the end.

The Borough of Bedford hired Howard Robson, Inc., a construction company, to upgrade the Borough’s wastewater facility. Robson hired J.J.D. Urethane, as a subcontractor, to supply and install urethane foam insulation, to the annular space on digester tanks, to create a seal against the tank walls. A few years later the Borough discovered that one of the digester tanks had been damaged. Robson had failed to correct it. The Borough sued Robson, who, in turn, filed a joinder complaint against J.J.D., claiming that “J.J.D. had improperly handled expanding foam insulation which was the ultimate cause of the damage to the digester tank.”

J.J.D. sought coverage from Westfield under a commercial general liability policy. Westfield disclaimed coverage and J.J.D. filed a declaratory judgment action. The trial court held that Westfield “did not have a duty to defend either the breach of contract or the breach of warranty claims in the joinder complaint since the claims were premised upon faulty workmanship, which does not constitute an ‘occurrence’ under the parties’ policy. [citing Kvaerner] However, the court found that the language in the Authority’s complaint and the joinder complaint regarding property damage that ‘occurred as a result of conduct outside of the scope of the [Authority’s contract with Robson] and J.J.D.’s Subcontract[,]’ could be considered an ‘occurrence’ under the policy, which could potentially fall within the policy’s coverage. Simply put, the trial court found that Westfield has a duty to defend, and potentially indemnify, Robson where it ‘carelessly allowed foam insulation to enter the digester [t]ank.’”

Westfield appealed to the Superior Court. The appeals court was not at all unmindful of the limitations placed on coverage for faulty workmanship by Kvaerner and Gambone. However, like the trial court, the appeals court also identified negligence outside the plans and specifications of the project; a possible scenario that the court noted was identified in Gambone.

The court held that “the complaint against the insured, J.J.D. (or, the joinder complaint), alleges negligent handling of the foam insulation and careless/negligent installation of the foam not in accordance with the plans and specifications of the project. Therefore, while the [Borough’s] complaint [against Robson] was grounded in allegations of defective workmanship, Robson’s joinder complaint does allege claims of negligent and careless work and work outside of the scope of the parties’ contract. Under such circumstances where the complaint ‘might or might not’ fall within the policy’s coverage as an ‘occurrence’, the insured is obligated to defend.” (emphasis added).

For sure the J.J.D. court could have done a better job of explaining this distinction, between work performed within the contract and outside of it. The court could have been more specific in this regard. Nonetheless, has the Superior Court – with its “work outside of the scope of the parties’ contract” concept -- just provided a way for underlying claimants to plead into long-denied construction defect coverage for their contractors -- at least for a defense. And with a defense in hand, the insured may have taken the first step to get its insurer to provide indemnity. |

| |

| |

| |

|

|

|

|

Vol. 7, Iss. 2

March 7, 2018

Applying The Wrong Duty To Defend Standard = Bad Faith

|

|

|

|

When it comes to what to consider when determining an insurer’s duty to defend, it generally works like this. About 33 or so states require an insurer to consider, besides the complaint, information contained outside the complaint – so-called extrinsic evidence. The rest limit the duty to defend determination to the information within the four corners of the complaint. In addition, when a state requires an insurer to consider extrinsic evidence, it is almost always a one-way street. In other words, the insurer must consider extrinsic evidence to possibly find a duty to defend, but may not use extrinsic evidence to deny a duty to defend.

That last part is what got the insurer in 2FL Enterprises, LLC v. Houston Casualty Ins. Co., No. 17-676 (W.D. Wash. Feb. 5, 2018) in trouble. At issue was an insurer’s duty to defend a construction defect suit. MCS retained a construction company, 2FL Enterprises, to make improvements on an apartment building. Leaks were discovered and MCS sued 2FL. 2FL sought a defense from Houston Specialty, which had issued several general liability consecutive policies to the construction company. The insurer took no action and a default judgment was entered against 2FL. The insurer then denied coverage on several grounds. 2FL sough coverage from another insurer and that insurer undertook its defense and had the default vacated. Houston Specialty agreed to defend but 2FL rejected the defense.

Coverage litigation ensued and the court addressed whether Houston Specialty owed and breached its duty to defend, and, if so, whether the breach was in bad faith.

The court held that the insurer breached the duty to defend. When assessing whether a defense was owed, the claims administrator for the insurer visited the website of the King County Assessor’s Office and learned that the present use of the building at issue was “Condominium: Residential.” The policies at issue contained a Condominium Exclusion. The insurer used this as one of its justification for denying coverage.

But here are the problems with this, as the court saw it: “Williams Court is not a condominium complex, it is an apartment building (which is covered under the policy). The second problem is that, under Washington law, an insurer is not permitted to utilize information extrinsic to (a) the complaint or (b) the insurance policy to arrive at a decision regarding denial of a tender of defense. The insurer may not rely on facts extrinsic to the complaint to deny the duty to defend - it may do so only to trigger the duty. (citation omitted) (As noted supra, the complaint described the building as the ‘Williams Court Apartments.’).” (emphasis in original).

Putting aside some other issues, the court turned to the question whether the insurer’s denial of coverage was in bad faith. The court concluded that evidence of bad faith “abounds here:” “There are a number of instances throughout the chronology of this event where Defendant acted in contravention of Washington law. The first and most egregious is its use of extrinsic evidence (e.g., the determination, based on the King County Assessor’s website, that Williams Court was a condominium building) to deny a defense to its insured- a violation of Woo. Additionally, HSIC claimed in its declination letter that Plaintiff began and concluded its work outside of the coverage periods, and that Plaintiff's subcontractors did not maintain CGL insurance, information which is found nowhere in the complaint.”

Lastly, the court rejected the insurer’s argument that it successfully rebutted the presumption of harm to the insured that was imposed upon the finding of bad faith. As the insurer saw it, the presumption of harm was rebutted because the underlying litigation was still ongoing and the default judgment had been vacated.

However, the court was unconvinced that this took care of any harm sustained by the insured: “The Court can conceive of numerous harms underlying a lengthy delay which culminates in a non-meritorious decision to deny coverage - e.g., the expenditure of time and effort to find another carrier to defend against the claims, the damage to financial credit that the existence of a default judgment and/or judgment lien (even a temporary one) can wreak on a business enterprise, and the damage to credibility and goodwill that the existence of such a judgment can impose (even if it is ultimately withdrawn). Defendant has done little or nothing to dispel the presumption of harm which its behavior has created, and Plaintiff is entitled to summary judgment on that issue.”

Determining whether an insurer has a duty to defend can be challenging. But knowing what standard to apply – four corners or extrinsic evidence – should not be. |

| |

| |

| |

|

|

|

|

Vol. 7, Iss. 2

March 7, 2018

Insurer Knows That Insured Has Been Sued. Insured Does Not Request A Defense. What’s Insurer To Do?

|

|

|

|

Anyone who does insurer-side coverage on a regular basis has faced this scenario. Suit has been filed against an insured. The insurer is well aware of it. But, for whatever reason, the insured has not sought a defense. What’s the insurer’s obligation here? Step in and address coverage and undertake a defense, if warranted. Or do nothing until the insured asks the insurer to do something?

This was the question before the Texas appeals court in Egly v. Farmers Ins. Exchange, No. 03-17-467 (Tex. Ct. App. Feb. 15, 2008). Ismael Hernandez was involved in a motor vehicle accident with Victor Egly. Hernandez was insured under an automobile policy issued by Farmers Insurance. Egly sued Hernandez. While Hernandez never notified Farmers of the suit, Egly’s attorney did – several times. “Egly’s attorney warned Farmers that Egly would obtain a default judgment against Hernandez if no answer was filed. Farmers sent messages to Hernandez inquiring about the case, but Hernandez never responded to those messages.”

True to his word, Egly obtained a default judgment against Hernandez. Egly sued Farmers to collect. Farmers filed a motion for summary judgment, maintaining that it owed Egly nothing because Hernandez never informed Farmers of the suit as required by the policy. The trial court granted Farmers’s motion for summary judgment and Egly appealed.

The parties’ competing positions, before the Texas appeals court, were simple – “Farmers argues that it did not receive notice from Hernandez concerning the accident and Egly’s suit and that it was prejudiced by this lack of notice. Egly responds that, because Farmers undisputedly had actual notice of Egly's suit against Hernandez, Farmers failed to establish as a matter of law that it suffered prejudice.”

The Texas appeals court affirmed, pointing to ample precedent for its decision. The court looked to the Texas Supreme Court’s 2008 decision in National Union v. Crocker, where the Texas high court held that “[m]ere awareness of a claim or suit does not impose a duty on the insurer to defend under the policy; there is no unilateral duty to act unless and until the additional insured first requests a defense—a threshold duty that the insured fulfills under the policy by notifying the insurer that the insured has been served with process and the insurer is expected to answer on its behalf.” (emphasis in original).

The court’s decision was tied to a prejudice determination and it looked at the notice provision in the policy as having two purposes: “Here, the first purpose of the notice requirement is satisfied, because Farmers had actual notice of Egly’s suit and could have prepared a defense. However, the second purpose is not satisfied, because Hernandez never notified Farmers that he ‘expect[ed] the insurer to interpose a defense’ or was ‘looking to the insurer to provide a defense.’ Therefore, Farmers had no duty to defend against Egly's suit. And because Farmers had no duty to represent Hernandez, it cannot be liable to Egly under the policy. . . . Because Hernandez never notified Farmers of Egly’s suit or requested representation, and because Egly obtained a default judgment against Hernandez that it sought to enforce against Farmers, Farmers has established as a matter of law that it was prejudiced by this lack of notice.”

I am fairly certain that policyholder and claimant attorneys find this decision to be unnerving.

[Note: Elvis, my favorite canine CO reader, would not have acted like Hernandez. Elvis loves to tender. See nearby article “The King Reads Coverage Opinions.”] |

| |

| |

| |

|

|

|

|

Vol. 7, Iss. 2

March 7, 2018

How Much “Loss Of Use” Is Needed For “Property Damage”?

|

|

|

|

Most general liability coverage cases, that address whether “property damage” has taken place, focus on the “physical injury to tangible property” aspect of the definition. That’s a more common scenario than whether there has been a “loss of use” of property (the other component of the definition of “property damage”). In addition, whether there has been “physical injury” is usually answerable with the naked eye (or with some assistance). You can see that a building is no longer standing or that water intrusion has caused damage. On the other hand, whether there has been a “loss of use” of property can be more esoteric. So, between “physical injury” cases being more common, thereby providing more guidance, as well as involving a more easily identifiable injury, it is not surprising that “loss of use”-based “property damage” cases can be challenging.

This was on display in Mid-Continent Casualty Co. v. Adams Homes of Northwest Florida, No. 17-12660 (11th Cir. Feb. 13, 2018). It is a construction defect case, but with an unusual aspect.

Putting aside the non-relevant corporate background, Adams Homes of Northwest Florida built homes on land that had originally been designed for golf courses and holding ponds. Homeowners sued Adams seeking damages for Adams’ alleged negligence in failing to ensure the installation of adequate drainage.

Adams sought coverage under a general liability policy issued by Mid-Continent. Mid-Continent denied coverage in 2009. Then, in 2015, Mid-Continent agreed to defend Adams, under a reservation of rights, after an 8th amended complaint was filed. Wow. Persistence.

Mid-Continent filed a declaratory judgment action. At issue was whether there was “property damage” alleged. The definition of “property damage” was the one frequently seen in CGL policies: “a. Physical injury to tangible property, including all resulting loss of use of that property. All such loss of use shall be deemed to occur at the time of the physical injury that caused it; or b. Loss of use of tangible property that is not physically injured. All such loss of use shall be deemed to occur at the time of the 'occurrence' that caused it.”

As the District Court saw it -- there was no “property damage” alleged as there was no “physical injury to tangible property.” The court stated: “In none of the one hundred and forty-seven paragraphs . . . is it alleged that Adams did anything that physically damaged [Homeowners’] homes.”

The Eleventh Circuit concluded that it did not need to decide whether that was correct, as the lower court failed to consider the “loss of use of tangible property that is not physically injured” aspect of the definition of “property damage.”

The Homeowners alleged that, on account of the manner of Adams’s construction – on land meant for retainage lakes -- “the streets adjacent to their homes, and the common areas they have access to, are now prone to flooding,” which has made “[Homeowners’] ordinary use or occupation of their property physically uncomfortable” and “disturb[ed] the [Homeowners’] free use . . . of their property.”

As the Eleventh Circuit saw it, these allegations created a factual issue whether the Homeowners alleged “property damage” on a “loss of use” basis. Thus, Mid-Continent had a duty to defend Adams.

The Eleventh Circuit went to the dogs for guidance in reaching its decision. It turned to the 1999 Florida appeals court decision in McCreary v. Florida Residential Property and Casualty Joint Underwriting Association. There the court held that an insured’s failure to control, supervise, and confine its dogs to its own premises was an “ongoing clear and present danger to the health, safety and comfort of [a neighbor]” that ultimately rendered him “unsafe and insecure in the use and enjoyment of his own property.” This, the McCreary court held, created a factual issue as to the loss of use of the neighbor’s property.

The court analogized the situation faced by the homeowners with the dog-fearing neighbor in McCreary: “These allegations [by the homeowner’s], fairly read, create a factual issue as to loss of use. Mid-Continent contends water is relatively harmless, unlike the McCrearys’ dogs, which entered Rebalko’s property and ‘caus[ed] an immediate danger to [Rebalko] and his pets.’ But the absence of allegations that the storm water run-off is placing Homeowners in immediate danger does not counsel a different result. Physical discomfort in the use of property, like insecurity and unsafety in the use of property, raises the specter of loss of use. Although it is unclear whether the physical discomfort caused by the run-off is severe enough to prevent Homeowners from using their property, the same was true of Rebalko’s allegations in McCreary. Rebalko did not allege he stopped using his property because of the McCrearys’ dogs; rather, Rebalko alleged he felt insecure and unsafe in its use. Like Rebalko, Homeowners are entitled to have any ambiguity about whether the physical discomfort caused by the run-off was severe enough to cause loss of use resolved in their favor. If the allegations of the complaint leave any doubt as to the duty to defend, the question must be resolved in favor of the insured.”

The take-away: In essence, at least for duty to defend purposes, the court read “loss of use” of property as “loss of enjoyment” of property. |

| |

| |

| |

|

|

|

|

Vol. 7, Iss. 2

March 7, 2018

Follow Form Excess Policy: Is There An Inconsistency Between Primary And Excess Terms?

|

|

|

|

It is well known that a follow form excess policy is subject to the terms of the underlying policy, except when they are inconsistent. In that case, the terms of the excess policy control. But how do you know when the terms of the two policies are inconsistent?

This was the issue before the court in Praetorian Ins. Co. v. Western Milling, LLC, No. 15-557 (E.D. Cal. Feb. 2, 2018). The facts stated by the court are thin. All we are told is that the case involves the availability of coverage for damaged cattle and, at issue, is the applicability of a “care, custody or control” exclusion. The exclusion in the primary policy precludes coverage for property in the “care custody or control of the insured.” The exclusion in the excess policy precludes coverage for property in the “care custody or control of any insured.”

In the matter at hand, the excess policy, standing alone – with its “any insured” verbiage -- would preclude coverage. However, the primary policy contained a severability of interests clause and the excess policy did not. The issue before the court was whether the excess policy, as a follow form policy, included the severability of interest clause. If so, then the excess policy’s “any insured” care, custody or control exclusion, in conjunction with the now-included severability of interest clause, would be read as care, custody or control of “the insured.” In that case coverage would be owed.

The insured argued that the primary policy’s severability of interest clause was included in the excess policy since it was not inconsistent with the excess policy. Indeed, the excess policy did not have a severability of interests clause. So how could it be inconsistent? The insured maintained that “a provision of the primary policy is only inconsistent if it is in direct conflict with another term found in the excess policy: for instance, the excess policy requires notification of a claim ‘promptly in writing,’ whereas the primary policy requires notification of a claim ‘as soon as practicable.’”

But the court did not see it that way. It examined whether the provision in the primary policy, to be incorporated into the excess policy, is facially inconsistent with a term in the excess policy. Using that test, the court found a facial inconsistency: “The severability provision of the primary policy states that the policy applies ‘[a]s if each Named Insured were the only Named Insured.’ The ‘care, custody, or control’ exclusion in the excess policy excludes coverage for losses to ‘[p]ersonal property in the care, custody or control of any insured.’ The severability provision of the primary policy therefore purports to treat each insured’s coverage separately, while the exclusion of the excess policy applies collectively regardless of which insured is claiming the loss and which insured had control of the property at issue. The inconsistency is apparent on the face of the primary and excess policies.”

Accordingly, on account of this inconsistency, the court held that the severability provision of the primary policy was not incorporated into the excess policy. Therefore, the excess policy’s exclusion, for property in the “care custody or control of any insured” applied in “full force.” |

| |

| |

| |

|

|

|

|

| |

|

|

Get Stopped For Driving Without Insurance – Buy A Policy While Sitting In The Car

This is remarkable. Robert Weaver, Jr. was stopped by the Pennsylvania State Police at 5:22 P.M. on November 26, 2016. He was cited for operating a motor vehicle while his operating privilege was suspended and for operating a motor vehicle without the required insurance. No problem. During the course of the stop Weaver used his phone to purchase a Safe Auto policy (I “signed up for it right then and there,” he said.) Seventeen minutes after being stopped Weaver was insured under an automobile policy. Really, I’m not making this up. See Weaver v. Commonwealth, No. 1115 (Pa. Commw. Ct. Feb. 15, 2018).

Weaver was convicted of both citations and did not appeal that. Then the Pennsylvania Department of Transportation suspended his operating privileges for three months for operating a motor vehicle without insurance. That Weaver appealed to the trial court – and won! The DOT appealed to the Pennsylvania Commonwealth Court, which handles appeals in cases involving state agencies. But then the trial court changed its mind. Anyway it’s procedurally confusing. In any event, the Commonwealth Court held that Weaver could not produce clear and convincing evidence that his vehicle was insured at the time that it was driven. Weaver admitted that he did not obtain the required liability insurance until 17 minutes after the traffic stop was initiated. The decision seems pretty obvious. But Weaver gets credit for trying. I can only imagine the Pennsylvania State trooper’s response [no doubt an all-business – no joking around type] if Weaver handed him his phone and said “what do you mean I’m not insured?”

Insured Cannot Sue Defense Counsel -- Even When It Was Staff Counsel -- For Malpractice

In Kapral v. GEICO, No. 17-11511 (11th Cir. Jan. 23, 2018), the federal appeals court held that an insured, under a GEICO automobile policy, could not maintain a malpractice action against the defense counsel retained by GEICO to defend him, even when counsel was the insurer’s “staff counsel.” The court cited two Florida decisions (the relevant state) holding that an insurer cannot be liable for the negligence of counsel that it retains for its insureds. Of note, the fact that the case at hand involved “staff counsel” did not dictate a different result: “Although it appears that the [two decisions] involved outside counsel, not salaried staff counsel, nothing in those decisions indicates that the result would be different in a case involving staff counsel. Nor should the result be different because under Florida law an insurer has no more right to exercise control over staff counsel’s professional conduct and independent judgment than it does over outside counsel's conduct and judgment.” The court added that its decision did not preclude the insured from pursuing a legal malpractice claim against the attorney.

|

|

| |

|

|

|

| |

|

|

|

|

|

|

|

|

|