|

|

|

|

|

|

Vol. 7 - Issue 5

June 6, 2018

|

|

|

|

|

|

| |

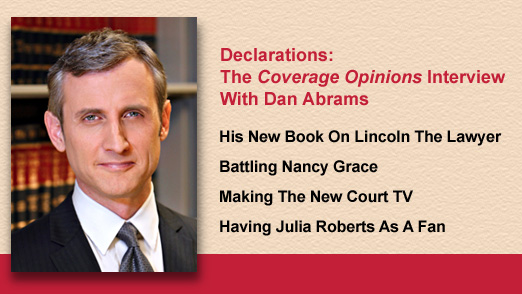

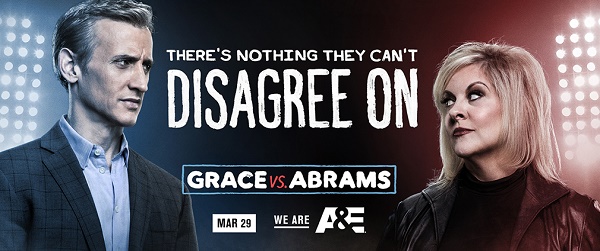

Dan Abrams was on his last spoonful of soup as I situated myself in his Midtown Manhattan office. I’m not surprised that his lunch was in a cup. The ABC News Chief Legal Affairs anchor has no room left on his plate. Earlier in the day he appeared on Good Morning America. We’re now at Abrams Media, his near ten-year old company that owns several news, culture and fashion websites, including Mediaite and another that he calls the next Court TV. Abrams has a twice-weekly, three-hour ride-along cop show on A&E – “Live PD” -- and just finished up a season of A&E’s “Grace vs. Abrams,” where he debates legal analyst Nancy Grace on celebrated cases. Abrams is also the doting father of a six-year old son. A Cirque du Soleil performer couldn’t pull off a juggling act like this. “I have to sneak in naps,” he says, in response to my look of wonderment about his schedule.

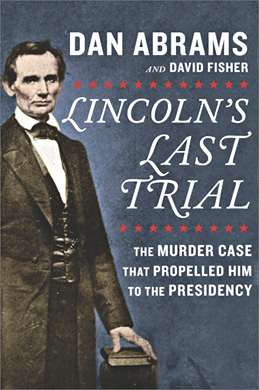

On June 5th he tossed another ball in the air when Hanover Square Press, a HarperCollins imprint, published Abrams and co-author David Fisher’s Lincoln’s Last Trial – The Murder Case That Propelled Him to the Presidency. To be sure, this is not just another book that looks at the familiar subjects that surround the 16th President. Instead, Abrams and Fisher offer a fascinating study of Lincoln’s 24-year career as a lawyer. The book’s centerpiece is a detailed account of Lincoln’s defense, just fourteen months before his 1860 election as President, of a man accused of stabbing another to death. The text has its genesis in a hand-written transcript of the trial -- discovered in 1989, wrapped in a ribbon, in a mouse-chewed shoe box in a garage. This rare find enabled the authors to uniquely showcase Lincoln’s courtroom presence.

The just-turned 52-year old Abrams was a gracious host, apologetic for running a little late and in no rush to be finished. The man who reportedly dated Renee Zellweger and Elle Macpherson, and who has been the subject of more than one New York Times profile on his personal life, has a regular-guy way about him. I tell him my mother is a huge fan. His appreciation upon hearing this news is nothing but genuine. When Julia Roberts came up to Abrams at a party to ask what Nancy Grace was like he says he thought, “Wow! Julia Roberts watches our segments.”

Timing Is Everything

If lawyering skills are genetic, Dan Abrams got as lucky as a Powerball winner. He is the son of First Amendment scion Floyd Abrams. The younger Abrams better have been prepared for class the day that The Pentagon Papers case was taught in Con Law. [Abrams’s sister, Ronnie Abrams, is a District Judge in the Southern District of New York.]

Abrams left Columbia Law School in 1992 and had his pick of prestigious law firms. A predictable path seemingly lay ahead. But he didn’t take that road. “Court TV started when I was in law school, which was the perfect combination of things I was interested in,” Abrams explains. “I came to the realization that I probably would excel at something other than the practice of law.”

Timing is everything, as the adage goes, and this was true for Abrams. “I’d been a reporter for six months [at Court TV] and I was definitely the low person on the totem pole,” Abrams explains. “It happened that the three main reporters were covering other trials, including one abroad, when O.J. happened.” So the trial of the century became Abrams’s assignment. “Like anything, I got lucky.”

Abrams spent five years covering trials for Court TV and then moved to NBC News, providing contributions to its Nightly News, Today and Dateline. His profile skyrocketed in 2001 with his nightly legal affairs program, The Abrams Report, on MSNBC. His namesake show spent five years on the air, followed by a variety of other television projects and positions, leading to his now near-daily appearances on ABC’s behemoth Good Morning America.

Dan Abrams has come a long way since Court TV. But his most ambitious project is to go back where he began.

Law & Crime Network

Trials as television programming started in earnest with the Juice. Abrams was in the room where it happened. He is a serious student of the genre and describes its evolution to me. It started in the early to mid-1990s, he explains, with Simpson, the Menendez Brothers, William Kennedy Smith and other trials that grabbed people’s attention. But in the early 2000s such television programming lost its appeal. “With the advent of reality shows, people saw reality on steroids. And the slow, methodical nature of trials as a means of entertaining took a back seat. Until people became frustrated with the lack of reality in the reality shows.”

“Trials are back,” Abrams declares. “Crime is an incredibly hot genre right now,” he says, pointing to the popularity of Serial, The Jinx, The Making of a Murderer and Discovery ID. There is also a factor dampening outlets for such programming: “If it weren’t for Donald Trump I think you would see a lot more trials on cable news.”

All of this has to do with Abrams’s decision to start the Law and Crime Network (lawandcrime.com) which offers live coverage of criminal trials throughout the country. Abrams takes me down the hallway to the studio where I am greeted by a news set featuring two well-dressed anchors who provide commentary. Next, we enter the control room, where several people are staring at a wall of televisions featuring the inside of courtrooms. It’s a tense place. Someone is giving directions to go from this screen to that one. I’m not sure anyone even noticed we were there.

Abrams has a deep understanding for the human interest that exists in trials. “Courtrooms have always had galleries,” he points out. A trial is “a combination of civic significance and entertainment.” Indeed. I point out to him that Alexander Hamilton (with Aaron Burr as co-counsel) represented the defendant in the first murder trial in the nation’s history. Hamilton’s well-known biographer, Ron Chernow, says in his tome on the ten Dollar founding father that on the first day of trial constables were needed for crowd control.

If the Law and Crime Network is premised on the public’s long-time fascination with criminal trials, more evidence of this abounds in Abrams’s new book. |

| |

Lincoln’s Last Trial

Abraham Lincoln had a 24 year career as a lawyer (one score and four years). He ran the nation for just four. Understandably his time as a lawyer is overshadowed by his presidency. In Lincoln’s Last Trial – The Murder Case That Propelled Him to the Presidency, Abrams and David Fisher seek to connect Lincoln’s two careers.

The book provides a detailed examination of Lincoln’s 1859 representation of the defendant in The State of Illinois v. “Peachy” Quinn Harrison. Harrison, age 22, was on trial in Lincoln’s hometown of Springfield, for the stabbing death of a rival. Lincoln argued self-defense. The book’s selling point is that the authors tell the story with the benefit of a 100-page handwritten trial transcript that was discovered nearly 30 years ago in the garage of a home in Fresno, California where Harrison’s great-grandson once lived. Trial transcripts from that time are a rarity – they were not required and resort to an expensive private scribe was required. The unearthed document provides a priceless and never before seen examination into Lincoln’s courtroom presence. Abrams shares with me the methodical and extensive research that went into the book, including accurate descriptions of things that Lincoln purchased during the trial.

|

|

|

|

| |

The case was personal for Lincoln on several grounds. The murder victim had trained to be a lawyer in Lincoln’s office. Lincoln’s client was the son of a close friend. Crucial to the defense was Lincoln calling as a witness a long-time enemy and political opponent. On account of the Lincoln-Douglas Debates the previous fall Lincoln came to the trial as a celebrity. A possible Presidential run was in the air. Just as with his client, Lincoln had much to lose with a loss. The press followed the case closely and it fascinated the public, who filled the courtroom each of its four days.

Hearing Lincoln’s own words in the Harrison trial, both addressing the court and questioning witnesses, makes for a fascinating and one-of-a-kind read. But the authors are wise to recognize that the book couldn’t stand on the trial alone. It needs context and to tell more than just a single story. This they provide in a lengthy introduction of Lincoln’s fascinating career as a circuit riding lawyer and other case studies told throughout. From this also emerges a look at how the legal system operated at that time. Many things are unimaginable today. A current client of Lincoln’s was on the jury. The prosecution knew him to be honorable and did not object.

The book is fast-paced and easy to get through. You don’t need a degree in history nor three David McCullough books under your belt to understand it. It superbly combines the courtroom drama of a man with his life on the line, the novelty of hearing Lincoln’s own words in an effort to spare him and a lesson in the great emancipator’s quarter century at the bar. Of Lincoln’s jury selection tactics, we find out that he had a prejudice against men with a high forehead, believing that they were likely to form an early opinion and be hard to dissuade, unless he could discern through voir dire that the man favored his client. Lincoln also preferred corpulent men on his jury. “It was generally believed that men of great size prospered by his wits rather than his toil. That was the kind of man who might better appreciate the delicacy of his arguments and approach[.]”

But isn’t writing a book about Lincoln an order as tall as a top hat? The Wall Street Journal not long ago reported that about 16,000 books have been written about Honest Abe. I pose this challenge to Abrams. He is hardly oblivious to it. He is counting on the novelty of the story to break through the Lincoln log jam. Abrams stands up from his desk, walks over to a box of books and looks for CNN legal analyst Jeffrey Toobin’s blurb: “You didn’t know that Abraham Lincoln was the defense lawyer in a notorious murder case on the eve of his presidency? Neither did I.”

Live PD

Dan Abrams has his own contribution to crime television. He hosts “Live PD” on Friday and Saturday nights on A&E. The show places its viewers into the passenger seats of police cars in several urban and rural cities, offering a real-time look at the work of law enforcement. There is no predictability of what each police stop may bring: bar fights, shootings, domestic disputes, all manner of civil disturbances, drug busts and sometimes just odd people walking down the street. Assisting Abrams are two law enforcement professionals who provide insight and analysis of the actions of the officers.

The show owes its success to the huge number of police cars that are under surveillance. As soon as one police stop turns uninteresting the control room has the ability to cut to another one offering more action.

The show is entertainment for sure. But it also serves another function: demonstrating the actions of law enforcement at a time in which the subject is one of national conversation. Viewers are encouraged to post their comments about what they witness on social media. |

| |

|

| |

Grace vs. Abrams

Abrams six-episode season of “Grace vs. Abrams” just came to an end. In each one-hour show Abrams and Nancy Grace discussed well-known trials of the past. Actually, since it’s Nancy Grace, “discuss” may not be the correct word choice here. The two go at it pretty hard. This isn’t professional wrestling. It is clearly not staged. The A&E promo sums it up: “There’s nothing they can’t disagree on.”

But despite the temperature of their debates, Abrams and Grace often agree that a person did what they are accused of. Abrams is no William Kunstler here. “I tend to be pretty pro-law enforcement,” he tells me. But there is still a dramatic difference between the hosts. While Nancy Grace is pounding the table declaring someone guilty, Abrams may be concurring, but identifying elements of reasonable doubt. Abrams comparison to his co-host is simple: “I am rational and stick to actual rules of law.”

I tell Abrams that I enjoy writing jokes and I wrote one about Nancy Grace. He gives me a suspicious look, like I’m about to say something that I’ll regret. But I carry on: “How does Nancy Grace satisfy the burden of proof in a criminal case?” Abrams shrugs. “She reads the indictment.” Abrams lets out a long laugh. I tell him he can have the joke.

The risk for “Grace vs. Abrams” is that, by focusing on old cases -- Drew Peterson, Scott Peterson, Casey Anthony, Robert Blake – the show runs the risk of appearing to just be a retelling of well-worn stories. Abrams is keenly aware of this and the show meets the challenge by focusing on newly discovered evidence or featuring guests speaking out for the first time.

“The goal in every show,” Abrams tells me, “is to make sure that we move the story forward in some way, shape or form. The risk of the flip-side would be that it’s perceived as re-hashing old cases.” Abrams credits the passage of time for the show’s ability to book its unique guests. “People who would not have spoken before, when everything was crazy, are able to make a calm, reasoned, premediated decision about what they want to do or not do.”

Strangely, everything I saw through the glass walls of Abrams’s office shouted new media. But after an hour with him I came away realizing the secret of Dan Abrams’s success -- he understands a lesson that goes back to the time of pens dipped in ink.

|

| |

|

| |

| |

| Elizabeth Vandenberg, a student at University of Iowa College of Law, assisted with this article. |

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Vol. 7, Iss. 5

June 6, 2018

Legalized Sports Betting Is Coming:

The Gambler’s Protection Policy

|

|

|

|

|

| |

By now you’ve heard, a lot, that legalized sports betting will soon be available from sea to shining sea. Not long ago the U.S. Supreme Court struck down the federal law that prohibited states from allowing its citizens to wager on the Baltimore Orioles. For some this is the greatest thing to happen to sports since the yellow line on the television showing the first down marker. Others see it as the worst thing to happen since the NCAA Tournament play-in games. And there are those who worry about the possible human impact -- a world of degenerate gamblers, who’ve lost it all, now walking the streets begging for money to bet on the Orioles.

But no matter which way it turns out, legalized sports gambling offers the insurance industry an excellent opportunity for a new product offering. Insurers have a superb track record for responding to societal developments, and new technologies, with products designed to transfer their associated risks. Most recently, think cyber.

Of course sports gambling comes with an obvious and inherent risk. But what about all of the other risks, besides simply losing, that participants can encounter. For those willing to risk being on the wrong side of a wager -- but not more -- the insurance industry will now be able to take these added worries off the table.

Introducing the new Gambler’s Protection Policy. The policy will provide coverage in all of the following scenarios:

• Insured, in a rush to get a bet off before kick-off, mistakenly clicks the wrong box and wagers on the Cleveland Browns. Policy will pay one half of the losing wager, up to the Cleveland Browns sublimit.

• Insured wagers on a college football team and a player on the starting roster is subsequently ruled ineligible for the game, on account of losing his amateur status, after accepting a piece of Double Bubble from a fan. Policy pays a losing wager if the insured would have won based on the game-time point spread.

• Insured caught checking the score of a wagered-game, while at his wife’s co-worker’s engagement party. Policy pays for two nights hotel accommodations if insured not allowed to return home.

• Insured loses a wager after the opposing team runs a trick play that is shown on Sports Center more than five times in a twelve hour period. Policy pays for three large bottles of Pepto-Bismol.

• Insured bets on his college alma mater’s football team despite knowing that it’s the dumbest bet in the world. Insurer pays the wager if the company’s Dumbest Bet Committee concludes that it was the dumbest bet in the world.

• Insured destroys the television, after throwing the remote control at it, when the team he wagered on takes a knee at the end of the game, within the opponent’s five yard line, when a touchdown would have enabled his team to cover the spread. Policy pays – one time -- for the cost to replace the television.

• Insured spends eleven hours completing his NCAA Tournament bracket for the office pool and finishes behind Mabel in the H.R. Department, who thought that Xavier was spelled with a Z. Policy reimburses the cost of the pool entry fee. Cost of losing your dignity is excluded.

• Insured chokes to death on a chicken wing. Policy pays $250,000 upon proof that the insured had an active wager at the time of death.

• Insured, while staring at his smart phone, walks into an intersection and is struck and killed by a motorist. Policy pays $250,000 upon proof that the insured was checking the score of a wagered-game at the time of death.

• Insured loses baseball wager on account of a fan interference situation. Policy pays the wager. Policy days double if the television announcer compares the play to Bartman. |

That’s my time. I’m Randy Spencer. Contact Randy Spencer at

Randy.Spencer@coverageopinions.info |

|

Congratulations Sebastian Maniscalco

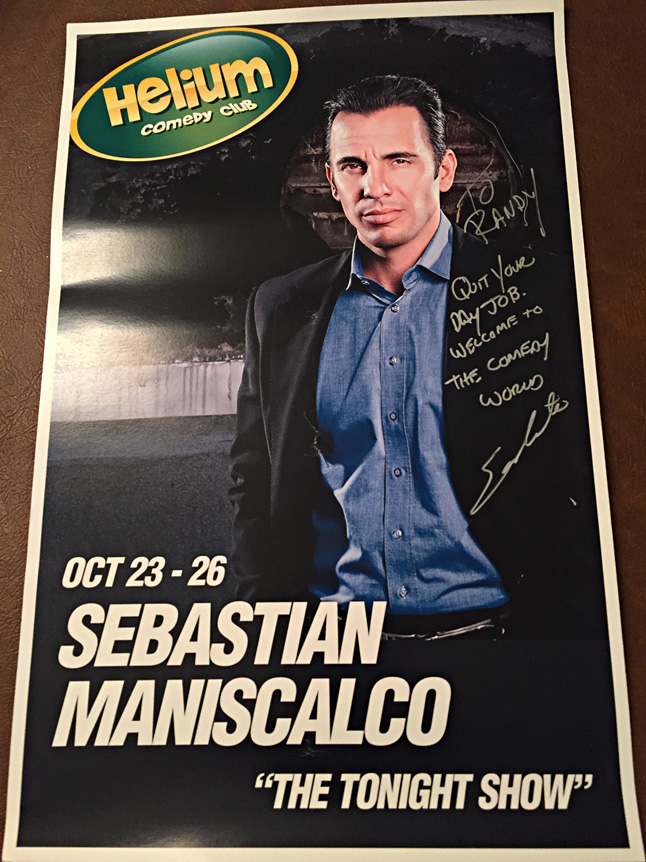

Back in 2013 I had the thrill of winning the John DeBella Stand-up Comedy Competition in association with Philadelphia radio station WMGK 102.9 FM. There was a nice cash prize, a huge trophy and the chance to open for comedian Sebastian Maniscalco at Helium Comedy Club in Philadelphia. [The trophy was particularly exciting. When you are 5’4” and Jewish you don’t win many trophies.]

At the time, Sebastian was a successful comic, performing at well-known clubs throughout the country and making appearances on the late night shows. It was really fun to open for him and hang-out in the club’s green room. And the club was standing room only.

Cut to five years later and Sebastian will be back in Philadelphia on September 13. But this time not at the 250 seat Helium Comedy Club. Instead he’ll be performing at the Wells Fargo Center, with a capacity of 21,000! Congratulations Sebastian on your huge success! If you are nearby check out the show. He’s hilarious. You’ll become an instant fan. |

| |

|

| |

|

| |

|

| |

|

|

|

|

Vol. 7, Iss.5

June 6, 2018

Approved: ALI Restatement Of Liability Insurance

Free Seminar On The Now-Approved ALI Restatement Of Liability Insurance

|

|

|

|

On May 22 white smoke billowed from the chimney of the Ritz-Carlton hotel in Washington as the American Law Institute voted to give final approval to its Restatement of the Law of Liability Insurance (RLLI). This comes after eight years of arduous work, 29 drafts, the change from a Principles Project to a Restatement, a delayed final vote last year and significant debate between advocates for insurers and policyholders.

But while one chapter of the RLLI may now be over, a new one will just be getting underway. Expect to see the RLLI cited by some parties in coverage litigation, using it in an attempt to persuade courts to their side. This will likely result in disputes over the role that the RLLI should play in the court’s decision making. Numerous courts have already discussed the RLLI in decisions. The last issue of Coverage Opinions contains an article that addresses the possible role of the RLLI in coverage litigation. Click here.

Look for a more detailed analysis of the ALI’s Restatement of the Law of Liability Insurance in the next issue of Coverage Opinions.

WHITE AND WILLIAMS LLP PRESENTS:

FREE SEMINAR ON THE INSURANCE RESTATEMENT

The RLLI has been the most talked-about subject in liability circles for the past decade. If you are not familiar with the RLLI, the time to learn about it has now come.

To learn about the RLLI, including its key provisions, how they compare and contrast with case law and the role that the RLLI may play in courts’ decision making, White and Williams invites you to join University of Pennsylvania Law Professor Tom Baker, the Reporter for the RLLI, and myself, for a discussion of these issues. This free seminar will take place on Thursday, June 28th at 2:30 P.M. at White and Williams LLP’s Philadelphia office.

To register for the program, Click here.

Space is Limited.

The program has been approved for 1.5 hours of Pennsylvania CLE credit.

|

|

| |

| |

| |

|

|

|

| |

|

Vol. 7, Iss. 5

June 6, 2018

|

|

|

|

|

| |

Insurance Key Issues: This Is What Makes The Book Unique

50-state surveys of liability coverage issues are not unique. But there are two things that make them unique in Insurance Key Issues:

• All of the 50-state surveys – which are extremely current -- are conveniently available in one location.

• At nearly 1,000 pages covering 20 issues, the extent of detail and case law is far more extensive than many 50-state surveys. There is often enough information to provide one-stop shopping to answer your question. If not, you’ll know exactly where to begin your additional research.

Check out these sample pages to see what I mean:

http://insurancekeyissues.com/SamplePages.pdf

The Insurance Key Issues Promise: If you like Coverage Opinions, rest assured that the same effort has gone into Key Issues for the past ten years.

Visit the Insurance Key Issues website: http://insurancekeyissues.com

|

|

| |

|

|

|

| |

|

|

The Four Questions: Andy Lundberg

Finding A Picasso Behind A Paint-By-Numbers

In 2017 Andy Lundberg put down his pen after 35 years of representing policyholders at Latham & Watkins in Los Angeles. He chaired the firm’s global insurance recovery practice for many years and also chaired the office’s Litigation Department for five years. Andy certainly went out on top: the same year that he retired he was named Los Angeles Insurance Lawyer of the Year by Best Lawyers.

After three-plus decades in the trenches – sometimes literally, as Andy’s coverage work included environmental -- he surely has stories to tell. I asked him to share some with Coverage Opinions readers. He was kind enough to do so, including one about the day he found the insurance coverage equivalent of a Picasso behind a paint-by-numbers at a flea market.

Following his graduation from Stanford in 1978, a stint on the Harvard Law Review, and a clerkship on the D.C. Circuit, Andy’s early career included leading roles in the defense of complex environmental tort and product liability actions. However, a couple of opportunities to work on some early cutting-edge environmental coverage cases, including a piece of the many-headed Montrose litigation, soon turned him into a full-time policyholder lawyer. His practice expanded to all the major coverage lines and a few oddball ones, earning him a place among the leaders of the policyholder bar. From its inauguration of the category in 2007 forward, Chambers & Partners ranked Andy in Band 1, in California and nationally, of American policyholder counsel. |

|

|

|

| |

Outside the office, Andy is the outgoing president of the Chancery Club of Los Angeles, a bar group founded in 1925, and a past president of the Half-Norwegian (On the Mother’s Side)-American Bar Association. An outdoor enthusiast, he is a past board member of Outward Bound, honeymooned trekking in Bhutan, and climbs an occasional mountain (he has summited his home state’s Mount Rainier four times). When he isn’t engaged as an AAA-credentialed arbitrator or Master Mediator, he whiles away the hours attempting to make himself and others laugh. As a Stanford undergraduate, he was a contributor to “Hellbent on Insanity,” a best-of compilation of college humor, an inductee into the Hammer & Coffin Society (the national collegiate humor honorary society), and the producer of the cult-classic 45-rpm punk rock record, “Picked Off the Litter,” which was made as a parody but now sells as actual art for up to $1,700 a copy.

What was the best part of your practice as a policyholder lawyer?

Two things, mainly.

First was the same thing I liked about being a First Amendment and con law geek in law school and like about contract law generally: insurance coverage is a great practice if you like the “law” part of being a lawyer. I always had an academic bent, and as a philosophy major in a very Anglo-American department -- all caught up in trying to do philosophy by looking at language -- I got very interested in arguments about meaning, which predisposed me to be fascinated with all those rules of interpretation aimed at divining what the parties supposedly meant. I cited a philosopher more than once in a coverage brief (A.J. Ayer was my go-to). I confess I enjoy the prospect of talking to judges about law more than that of talking to jurors about facts, and I was very fortunate to stumble into Latham & Watkins, where I could actually start and build a practice in the very law-oriented coverage area, working on cutting-edge, big-money issues right out of the box. I was also very lucky that my best friend from law school, Mark Newell -- one of the best lawyers ever, and eventually the vice-chair of Latham -- also joined the firm and also became a policyholder lawyer. We had many wonderful years of successful collaboration and are still very close today.

Second, the complex coverage practice at the national level is a relatively small bar in which you develop ongoing relationships with both your opponents and your fellow sufferers/competitors. At least in some instances, that makes the job more interesting in a Borg-vs.-McEnroe sort of way -- OK, you got me that time, but I got you worse the time before that, let’s have a drink and tell some stories.

There is a small group of really good carrier lawyers out there who appreciate the intellectual elegance of many of these coverage issues, play fair, and make the contest fun. They embody the best qualities of professionalism, and some even end up being your friend at the end of it all. Among those worthy adversaries -- and I stress that it’s not an exhaustive list -- I’d include Stuart Cotton of Mound Cotton, Rich Goetz of O’Melveny, Paul Koepf of Clyde & Co. (against who I had my very first coverage case back in 1983), Paul Killion of Duane Morris, John Roth of Chubb, and Charlie Wheeler of Cozen. The week I retired, I called a bunch of those guys up and told them how much I appreciated their integrity and common sense and the opportunity to work against them over the years.

By the way, my Latham colleagues occasionally suggested that the best thing about the policyholder practice was that since jurors can be just as biased against insurers as they can against alleged corporate polluters, securities fraudsters and makers of dangerous products, I was picking only the easy fights. I deny it (they should have been there for Montrose and a few others!). And even if they were right, well, sorry, but plenty of gold medals have been handed out to folks who did a really good job of executing the easier dive . . .

What do you consider to have been your most interesting or challenging cases?

As I say, I was very fortunate to end up at Latham & Watkins in the early 1980s, when the environmental coverage wars were just getting under way. My “tenure piece” was one of the very first cases against the infamous London EIL program, the first generation of what is now known as Pollution Legal Liability coverage. That program was cooked up from whole cloth; the lead underwriter was a British chemistry professor who had never written insurance before (I deposed him for, I believe, 20 days). I took so many depositions in that case that I’m pretty sure at one point I knew more about that program than anybody who had worked for it (one of the deponents asked me when we were finished if I had been at one of the meetings I had questioned him about). Based on that learning curve, I then got involved in Montrose’s claim against the same insurers involving the Stringfellow site and others. What an incredible education those two cases gave me in just about every conceivable aspect of insurance coverage.

I had a similarly robust and fascinating experience against another first-generation coverage product when I represented a bank in a series of cases arising out of the short-lived insurance-backed independent film financing program. Another fine lesson in “you can spot the pioneers -- they’re the folks with the arrows in their chests.” The underwriters of that program thought they were going to make a fortune guaranteeing bank loans to independent movie producers. They greatly underestimated the role of adverse selection, and also discovered, guess what, it’s hard to predict if a movie is going to be a hit or not. Again, I got to spend quite a lot of time being one of the first lawyers to pick apart a novel insurance concept and showing how it really hadn’t been thought through before it was launched.

You are credited as “the guy who found the lost chord” -- California Insurance Code Section 520 -- that resulted in Fluor v. Superior Court (2015), in which the California Supreme Court stunningly overruled its earlier ruling on the hugely important consent-to-assignment, Henkel v. Hartford (2003). How’d that come to pass?

Well, in a very unusual way, especially in this day of full-text legal research. I was sitting in my office one Friday afternoon in, oh, 2009 or so. That was a point in the week when, with the phones and email cooling off, I often found time to spend an uninterrupted hour or two doing some research I’d had to defer (I always did a lot of my own research). I was working on some claim or other having absolutely nothing to do with consent to assignment -- some insurability issue, I think. I was flipping through my paper copy of the California Insurance Code, thinking that there was some statute dealing with whatever the issue was somewhere in those juicy code sections around the 300s to the 600s. So I’m just flipping pages and skimming, and wait a minute, what’s this? Here’s Section 520, enacted in 1872, one sentence long, and it seems to say exactly the opposite of what the Supreme Court held in Henkel! Long story short, I reread Henkel, pulled the Supreme Court briefs, then pulled the Court of Appeal briefs, and then pulled the original motion papers -- not a mention of it anywhere. It appeared to be the statute that time forgot. (It had been cited in exactly one case, and never in any law review or commentary, in its 130-year history).

So through sheer caprice, I had discovered what seemed like a completely novel argument for overruling Henkel . . . but I had no case in which to make it! But one of the virtues of working for a great big law firm that operates on the “one-firm firm” model is that you have a lot of colleagues fighting a lot of issues every day and a lot of communication about them. Lo and behold, I soon learned that our client Fluor had a case, which my partners Brook Roberts and John Wilson were handling, with a consent-to-assignment issue (ironically, unlike most of our cases where we’re the plaintiff, that case was a dec relief action that Hartford -- the winning insurer in Henkel -- had filed against Fluor).

The rest is history -- and when Fluor came out I was tickled to call Carlos Moreno, a now-retired Justice who had been the lone dissenter in Henkel, to tell him that his dissent had been vindicated. (We had lost resoundingly in the two lower courts, by the way, which made it all the sweeter.) The research on that case, including the legislative history of Section 520 going back to the original Field Code and beyond, and development of the argumentation we ultimately prevailed on was one of the most fascinating projects of my career.

Funny footnote to all that: early on in our litigating the consent issue in Fluor, before we had a ruling in the trial court and others were aware of the case, my dear then-colleague Alexandra Roje, now a partner at Lathrop Gage, rolled into my office one day and said “hey, I just noticed this Section 520 -- isn’t that contrary to Henkel?” I guess Latham is a culture of page-flippers.

I actually think there’s an even better argument against the insurance industry’s consent-to-assignment position that nobody has made yet. Maybe I’ll write an article about it one of these days.

Lawyers are famous for thinking they all have the Great American Novel inside them, and many make the mistake of letting it out. Is it true you’ve found a middle way?

Yeah, I was at risk of being one of those -- in my tenth high school reunion report, one of the three things I said I still hoped to accomplish was “publish a novel.” It turns out writing a decent novel requires a lot of time and inspiration, which sounds an awful lot like practicing law.

On the other hand, writing a terrible novel is pretty easy -- just ask the friends of most lawyers who have taken pen in hand. So a couple of years ago, I entered the long-running Bulwer-Lytton Fiction Contest for the first time. It recognizes the composition of the first sentence of “the worst of all possible novels.” I was delighted to receive a Dishonorable Mention (i.e., almost the worst) for a sentence featuring my superhero Swordfish and his every-loyal sidekick Ling Cod Boy gearing up to battle the arch-villain Avenging Tuna. Encouraged, I entered again in 2017, and won the Adventure and Science Fiction categories. I’m still after the Grand Prize, though. By the way, I know it still sounds like a lot of work to write an entire awful novel and then submit the first sentence of it to a contest, but you don’t think I’m to cheat and just write the one sentence, do you?

|

|

| |

|

|

Vol. 7, Iss. 5

June 6, 2018

Winners Of The Insurance Coverage Haiku Contest

|

|

|

|

Well that was a surprise. Based on past experience I had been expecting 10 entries in the insurance coverage haiku contest. Instead I received 125 or so. [No doubt the offer to send all entrants a fantabulous Coverage Opinions pen is what got so many people’s creativity going.]

With all those entries I decided to name four winners instead of two. Even that was no easy task. Here they are:

Dude owned the Lakers

Tried to get his money back

Repaid some instead

Stephen Berry

Dentons

Atlanta

Not covered all years?

Pro rata seems to make sense

But terms say all sums

Jeffrey Davis

Quarles & Brady LLP

Milwaukee

Ambiguity?

A tie goes to the runner

Insured is runner

Pam Touchstone

Stacy Conder Allen LLP

Dallas

And, as discussed in the last issue of CO, there was an early winner:

At first, Principles

But they’re aspirational

Restatements change law

Lance D. Meyer

O’Meara Leer Wagner & Kohl, P.A.

Minneapolis

|

| |

|

| |

I sure have a lot of Coverage Opinions pens to mail out. I need to order more in fact. Give me a little time to order them and get them out the door. It’s worth the wait. Past Coverage Opinions pen recipients have described it as life-altering.

The Coverage Opinions Prize Patrol will be delivering copies of the 4th edition of Insurance Key Issues to these insurance coverage bards |

|

|

| |

| |

|

|

|

|

Vol. 7, Iss. 5

June 6, 2018

Encore: Declarations:

The Coverage Opinions Interview With Ben Brafman – Attorney For Harvey Weinstein

|

|

|

|

Ben Brafman is representing Harvey Weinstein against the rape charges that the movie producer is facing in New York. Last year I spent an hour sitting across the table from the renowned criminal defense attorney in his Manhattan office. It was prescient: Brafman explained to me why he has one of the hardest job in America.

Check out my prior interview with Ben Brafman. That he got the call to represent Harvey Weinstein is not surprising. Surprising would have been if he didn’t get it.

http://www.coverageopinions.info/Vol6Issue7/Declarations.html

|

|

| |

|

|

|

| |

|

Vol. 7 - Issue 5

June 6, 2018

|

|

|

|

|

|

| |

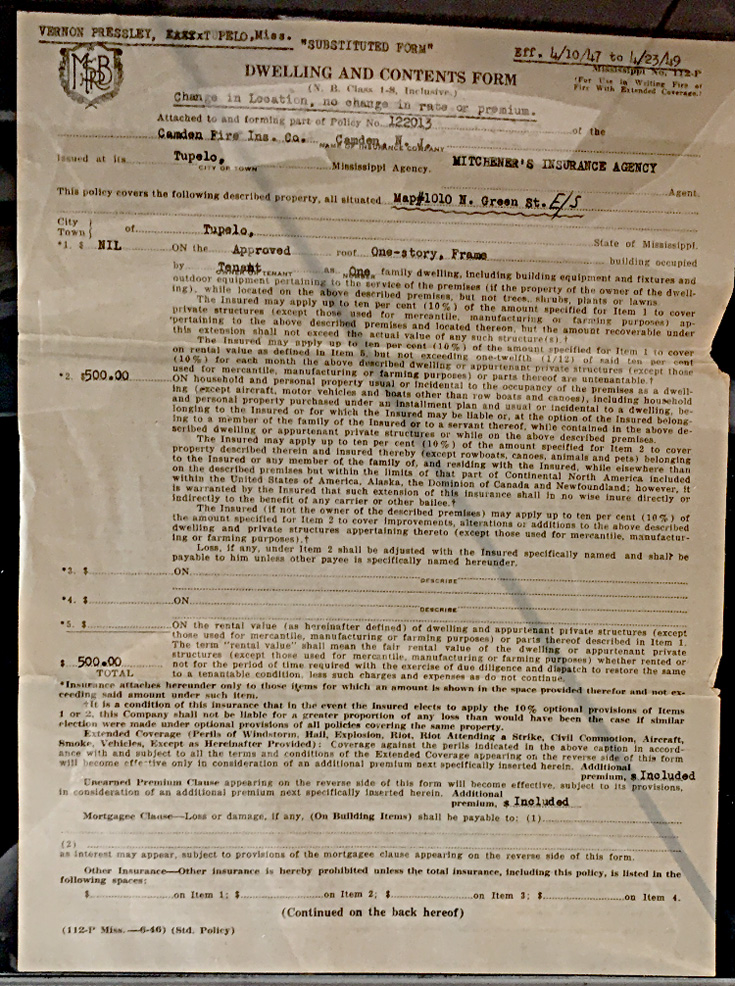

I recently visited Graceland in Memphis. [Many CO readers kindly responded to my request for things to do in Memphis and their favorite BBQ joints.]

Elvis was clearly a pack rat as the number of the King’s artifacts on display, both in his Graceland home, and its accompanying museum, is incomprehensible. Imagine my surprise when the first thing I saw upon entering the museum [first, not second, not third, first] was Elvis’s parents’ homeowner’s policy from 1947. Issued by Camden Fire Insurance Company, the policy covered their residence in Tupelo, Mississippi. Elvis was eleven years old when it was issued.

Thankfully, for the document’s sake, it was in a glass case, as I spent ten minutes drooling over it.

|

| |

|

|

| |

| |

|

|

| |

|

|

|

|

Vol. 7, Iss. 5

June 6, 2018

Blind Melon: Seeing A Coverage Opinions Interviewee In Concert

|

|

|

|

Late last year I had the thrill of interviewing Rogers Stevens for Coverage Opinions. Rogers is a fourth year associate in the Labor and Employment Group in the Philadelphia office of Ballard Spahr. But Rogers has a second gig. He is the guitarist for 90s mega-band Blind Melon.

The band that Rogers founded exploded onto the music scene in 1993 when the video for its song “No Rain,” featuring a young girl dancing in a bumble bee costume, owned the MTV airways. Rogers and his bandmates appeared on the cover of Rolling Stone, had an album go quadruple-platinum and reach number three on Billboard, and were nominated for two Grammys.

Blind Melon still performs around the country and I had the chance to see them last month at the Theatre of Living Arts on South Street in Philadelphia. It was a great show (despite my favorite song not being played) and the place was packed.

When I met Rogers last year I posed this riddle to him: How do you know that the guitarist for Blind Melon is a lawyer? Answer - Because he’s checking his work emails during a drum solo.

As I watched Rogers Stevens on stage at the TLA, totally engrossed in his guitar playing, I’m pretty sure he wasn’t thinking about non-compete clauses.

|

|

|

|

|

|

Rogers Stevens (right) |

|

|

|

|

|

Vol. 7, Iss. 5

June 6, 2018

Insurance Coverage Talk Radio:

What Is The Most Important Pollution Exclusion Decision?

|

|

|

|

Some of the most entertaining sports talk-radio is when listeners are asked to weigh-in with their choice for the best of something, such as left-handed pitchers (Steve Carlton) or sports movies (Field of Dreams) (sorry, Rudy fans). Since talk radio thrives on controversy, and because people are passionate about things that they believe are the best of something, it is not surprising that a lively and entertaining debate can be counted on when peoples’ strongly held beliefs are challenged.

So if such a thing as an insurance coverage talk-radio show existed (work with me here), surely there would be a night where the host invites listeners to call in with their vote for the most important judicial decision to address this or that coverage issue.

What if that topic were the pollution exclusion. Here’s how I see it going:

[Let’s go to the phones and talk to Jeff from Sacramento.] “Hey guys, first-time caller, long-time listener.” [Jeff - turn down your radio.] “When it comes to the pollution exclusion, I’d have to say that the most important decision is Pipefitters v. Westchester Fire Ins. from the Seventh Circuit in 1992. It was this court’s observation that, without some so-called limiting principle, the absolute pollution exclusion would lead to some absurd results, such as excluding coverage for bodily injury suffered by a person who slips and falls on the spilled contents of a bottle of Drano. The Drano example led to some courts limiting the pollution exclusion to traditional environmental pollution.”

[Thanks for the call Jeff. Amy from Piscataway in the Garden State is on the line. She must know a thing or two about pollution. Go ahead, Amy, you’re live on Coverage Call-In.]

“Thanks for taking my call. Love your show. I’ve gotta disagree with the guy from Sacramento. You have to go back to when it all began. I think that Lansco v. DEP is the most important pollution exclusion decision. Sure, it’s a 1975 New Jersey trial court decision, but that’s just the point. It was the first to address the meaning of ‘sudden’ in the ‘sudden and accidental’ exception to the pollution exclusion. Lansco concluded that sudden means unexpected or unforeseen. And defining sudden as something other than temporally abrupt is what opened the door for insureds to seek coverage for gradual discharges of pollution. And we all know how contentious and significant that issue was in the large environmental coverage cases in the 1980s and 90s. And it was the litigation over the sudden and accidental exclusion that led to the adoption of the absolute and total pollution exclusions – which has brought another 25-plus years of hotly contested coverage litigation. You could say it all goes back to Lansco.”

Well thanks everyone for listening to Coverage Call-In and to Jimmy Smith for the great job, as always, behind the glass. Tune in tomorrow night when we’ll be joined by Bill Roberts to discuss his new treatise on the definition of “mobile equipment.” You won’t want to miss it.

|

|

| |

|

|

|

|

Vol. 7, Iss. 5

June 6, 2018

U.S. Open Preview:

What You Need To Know About Getting Hit By A Golf Ball At A Professional Tournament

|

|

|

|

The U.S. Open tees off next week at Shinnecock Hills Golf Club in Southampton, New York. It’s a funny thing about golf – it’s the only sport where the spectators have a greater risk of sustaining a serious injury than the players. Golfers risk back injuries. Some spectators, on the other hand, stand unprotected, just slightly to the side of someone who will be hitting a rock hard ball at lightning speed. If you are going to the Open, and meet Phil Mickelson because he comes up to apologize and check on your well-being, will you be able to recover for your injuries?

The obvious starting place to answer this question is the huge body of case law that addresses liability for spectators injured by a foul ball at a baseball game. In general, courts across the board have made it very difficult for those injured in this way to recover from the owner or operator of the stadium. Many have adopted the so-called “baseball rule,” which generally provides that a baseball stadium owner or operator is not liable for a foul ball injury as long as it screens the most dangerous part of the stadium and provides screened seats to as many spectators as may reasonably be expected to request them.

Will a spectator injured at next week’s U.S. Open suffer the same fate as an unlucky baseball fan? At least one case says no.

I consider myself a golf fan. Despite that, I’ve never heard of a professional golfer named Dow Finsterwald. Shame on me. While he played long before my time, he was no here-today, gone-tomorrow pro. Finsterwald won eleven tournaments between 1955 and 1963, including the 1958 PGA Championship. He played on four Ryder Cup teams and served as non-playing captain for the 1977 U.S. Ryder Cup team. In 1958 he was honored as PGA Player of the Year. He is fifth on the list for consecutive cuts made (72). And he’s probably a whiz at getting a golf ball through the moving blades of a wind mill.

On June 29, 1973, Finsterwald was playing in the Western Open at Midlothian Country Club not far from Chicago. On that date Alice Duffy and a companion were in attendance as spectators. Shortly after arriving they watched Arnold Palmer tee off at the first hole. The women then walked toward the first green, stopping at a concession stand set up between the first and eighteenth fairways. While watching play on the first hole, Ms. Duffy was hit by Dow Finsterwald’s tee shot on eighteen. Ms. Duffy lost all sight in her right eye and was forced to wear a prosthetic shell over her eye for cosmetic purposes.

[I did some checking. Here is how the 1973 Western Open turned out. Billy Casper won (-12). Arnie finished 7th (-8). Dow Finsterwald made the cut, but it wasn’t his tournament any more than it was Alice Duffy’s. He came in 76th place at +11.]

Litigation was filed against the club, the Professional Golfers Association of America, Western Golfers Association and Mr. Finsterwald. The litigation was protracted. The accident took place in 1973. There is a second Appellate Court of Illinois decision from 1985. And who knows if that was really the end. Those who think that golf moves slowly now see that something moves even slower.

The trial court in Duffy v. Midlothian Country Club granted summary judgment for the defendants. But in a 1980 opinion the Appellate Court of Illinois reversed, holding, among other things, that a material question of fact existed as to whether defendants fulfilled their duty to plaintiff as a business invitee. The case went to trial and a jury awarded Ms. Duffy $498,200, which was reduced by 10% for her own negligence. [The PGA had been dismissed by plaintiff and the jury found for Finsterwald and against plaintiff.]

In a 1985 opinion in the case the Appellate Court of Illinois upheld the award. The decision is heavy on the legal. The court concluded that the doctrine of secondary implied assumption of the risk (plaintiff implicitly assumes the risks created by the defendant’s negligence) is abolished by the introduction of comparative negligence. Thus, plaintiff’s assumption of the risk will not operate as an absolute bar to recovery in a negligence action, but, rather, merely aid in the apportionment of damages.

It appears that an important part of plaintiff’s case was the affidavit of Tim Mahoney as an expert witness. Mr. Mahoney was a member of Midlothian, had played there for 35 years, won the 1973 Western Open Pro-Am Tournament and he attended the 1973 Western Open. Mahoney was aware of the club’s preparations for the tournament. The court described his affidavit: “He stated that concession stands were placed in areas in which balls had regularly landed in the past, and that the fairways were so close together that the spectators located between the fairways are within range of balls likely to be hit by golfers. He further stated that the spectators would not be able to see the player hitting the ball as the shrubbery and hills interfered with visibility.”

The take-away from Duffy v. Midlothian Country Club is that, while many courts have adopted the so-called “baseball rule,” here the court applied no such special “golf rule” to determine the standard of care owed to a business invitee.

It is customary for a professional golfer that hits a spectator with a ball to give the spectator an autographed glove. That’s a nice gesture. If you’re that unlucky person, accept it. But make clear that it is not a release of any other claims.

|

|

| |

|

|

|

|

Vol. 7, Iss. 5

June 6, 2018

“Continuing Injury Exclusion” Not Upheld In Multiple Plaintiff Case

|

|

|

|

I’ve been saying this for a while. In general, insurers have had mixed results in construction defect cases when it comes to enforcing exclusions (usually added by endorsement) that are intended to preclude coverage for “property damage” that took place before the policy period, even if such damage is continuing into the policy period, and even if such damage was not known by the insured to exist. These exclusions sometimes go by the name Continuing Injury Exclusion or First Manifestation Exclusion or something else along those lines.

Some courts have interpreted these exclusions narrowly and applied a strict “sameness” test (my term) between the “property damage” that existed pre-policy inception date and that which took place during the policy period, for which coverage was being sought. Further, it has generally been the “property damage” itself that must be known by the insured prior to the policy period -- and not simply the cause of the “property damage.”

One interesting aspect of these cases is that they are sometimes “insurer vs. insurer.” Generally, a defending insurer takes issue with another insurer’s attempt to enforce an exclusion that saddles the defending insurer with greater exposure.

Add Century Surety Company v. United Specialty Insurance Company, No. 17-6589 (C.D. Calif. Apr. 24, 2018) to the list of decisions that has given a narrow interpretation to a Continuing Injury Exclusion (and it’s insurer v. insurer).

In 2016, 55 tenants of an apartment building filed suit against its owners, Bonnie Brae and Ramin Akhavan, alleging “slum conditions,” including uninhabitable units and a lack of security. The complaints alleged that problems at the building existed since 2006: “Consistent deferrals of maintenance allegedly resulted in faulty electrical wiring and plumbing, a lack of hot water, insect and rodent infestations, and other unsanitary living conditions.” Open and dangerous criminal activity in the building was also alleged.

The tenants alleged a host of damages such as (1) bug bites, asthma and other respiratory problems, (2) personal property damage, including having to throw out microwaves, dressers, refrigerators, hot plates, and food due to rodent and insect infestations, (3) being threatened with eviction for making complaints to management and city or county agencies, and (4) invasion of privacy from having their units entered by others without consent.

Bonnie Brae sought coverage from several insurers and there were numerous policies in play. Certain insurers undertook the defense and shared costs. United Specialty Insurance Company disclaimed coverage. One of the defending insurers filed suit against United Specialty for contribution for defense costs.

United Specialty acknowledged that the complaints alleged bodily injury, property damage and personal injury, but denied that it alleged an occurrence on account of the intentional nature of the allegations. At least for duty to defend purposes, the court dismissed this argument: “USIC argues that notwithstanding the tenants’ use of the ‘negligence’ label, there are no factual allegations in the Chavez complaints showing that the insureds’ acts or omissions were accidental, unintended, or unexpected. . . . Although the Chavez complaints allege intentional conduct, and the Xec and Geronimo actions lend support to this allegation, the Court nevertheless finds that coverage depends on the unresolved factual issue of whether at least some part of the insureds’ injury-producing conduct was intentional or rather accidental.”

Turning to trigger of coverage, the court rejected United Specialty’s argument that its policies – on the risk from March 2013 to January 2016 -- were not triggered on account of the Continuous Injury Exclusion, which precluded coverage with respect to “any ‘claim’ or ‘suit’ against any insured which is alleged to be ongoing and continuing in nature, if the ‘bodily injury’ or ‘property damage’ [or ‘personal injury’] is alleged to have existed prior to the effective date of this policy.”

As United Specialty saw it, the exclusion served to preclude coverage because the complaints alleged consistent deferrals of maintenance since at least 2006. Thus, so the argument went, the claim or suit was ongoing and continuing in nature.

However, the court did not see the Continuous Injury Exclusion having across the board applicability: “[N]ot all of the alleged bodily injury, property damage, and personal injury suffered by the tenants is alleged to have existed prior to the effective date of this policy, that is, March 27, 2013 in the case of the first consecutive policy. On the contrary, the action involves 55 individual tenants joined in a single lawsuit who have lived in the apartment building during different time periods. Many of these tenants allege that they first moved into the building after the effective date of USIC’s first consecutive policy, and accordingly suffered bodily injury, property damage, and personal injury for the first time during the policy period. While the continuous injury exclusion may apply to some tenants who have lived in the building and therefore suffered continuous injury prior to the policy period, USIC cannot employ this exclusion to negate coverage with respect to all plaintiffs in the Chavez action.” (emphasis added).

The court held that United Specialty owed the defending insurers an equitable share of all defense expenses incurred to date and, going forward, must contribute an equal share of defense costs until its duty to defend is discharged.

Like several cases before it, the court interpreted the Continuous Injury Exclusion narrowly and applied a strict “sameness” test between the bodily injury and property damage that existed pre-policy inception date and that which took place during the policy period, for which coverage was being sought.

|

|

| |

|

|

|

|

Vol. 7, Iss. 5

June 6, 2018

New York State Of Bind: The Post-Carlson Issue Is Here

Insurers Ignore At Your Peril

|

|

|

|

You can’t overstate the significance of the New York Court of Appeals’s late-2017 decision in Carlson v. American International Group. There New York’s highest court significantly expanded the reach of New York Insurance Law Section 3420(d). That’s that New York statute that can invalidate a disclaimer letter, for a bodily injury or wrongful death claim, that is not sent expeditiously. It is also the statute that can invalidate such a disclaimer letter where a copy of it was not sent to the claimants.

Many insurers have fallen afoul of Section 3420(d)’s requirements and paid for it. Carlson sets the stage for more of this to come. But not because Carlson expanded the requirements under Section 3420. Those remain unchanged.

Rather, Carlson’s impact is that it expanded the extent of situations in which the statute may be in play. Claims that you would have never before considered being subject to Section 3420(d) may now be. But that’s still not telling the whole story. The real issue presented by Carlson is that it did not provide any substantive guidance on whether one of these new “3420(d) situations” exists. This is a serious problem for insurers.

This issue was on display last week in Vista Eng’g Corp. v. Everest Indemnity Ins. Co., No. 302991/15 (N.Y. App. Div. May 24, 2018). The court addressed coverage for a general contractor, as an additional insured, under a policy issued to a subcontractor, for an injury sustained by an employee of the subcontractor on a New York construction site. The insurer for the subcontractor disclaimed coverage based on the policy’s “third party action over” exclusion.

Not so fast – literally -- said the general contractor. It commenced litigation and maintained that the insurer failed to timely disclaim coverage as required by Section 3420(d). The insurer responded that Section 3420(d) applies only to insurance policies “issued and delivered” in New York. As the insurer saw it, this was not a 3420(d) situation as it is a New Jersey insurer and the policy was issued to its insured, a New Jersey Company.

The trial court agreed with the insurer that the policy was issued and delivered outside of New York, so, therefore, the timeliness requirements of Section 3420(d) did not apply.

But the Appellate Division did not see it being so cut and dry. The court based its decision on Carlson, which is described holding as follows: “[T]he applicability of Insurance Law § 3420(d)(2) depends on (1) a policy covering risks located in New York, and (2) the insured being located in New York. The Carlson Court, for the first time, determined that a company was ‘located in’ New York if it had a ‘substantial business presence’ there.

To put it another way, prior to Carlson, the question whether 3420(d) was in play was a relatively objective test – a New York insurer or an insured with a New York address on its declarations page. Now the test is not so easy, and can’t be determined simply based on a zip code. Post-Carlson the question is whether the insured has a “substantial business presence” in New York. But what does that mean? How much of a presence is required to be substantial? It is not clear -- as Carlson does not set forth a specific definition of this term.

The Vista Eng’g Corp. seemed inclined to conclude that the insured had a “substantial business presence” in New York, pointing to the fact that the price under the subcontract was close to $1,000,000 and there was some evidence that it was the insured’s main job.”

However, the court was not willing to end it there. It held that “[b]ecause the Carlson Court did not set forth a specific definition of substantial business presence, and because the record is insufficiently developed concerning East Coast’s business presence in New York, we remand to allow the parties to develop the record and give Supreme Court an opportunity to meaningfully review the case in light of Carlson.”

A lengthy dissenting opinion, on the other hand, was willing to call it quits, concluding that 3420(d) applied and the case should be remanded to determine if the disclaimer was timely. This is a dissent worth reading for further guidance.

To put all of this into perspective… Section 3420(d), pre-Carlson, was a statute that presented challenges for insurers. And the consequences for failing to abide by it are draconian. Now, the number of claims potentially subject to Section 3420(d) has been expanded. But there is no clear guidance whether a claim comes within this new reach of 3420(d). This has to be figured out by the insurer, using the undefined “substantial business presence in New York” test. How can the insurer know this without getting a lot of information from the insured about its business? But it better do so, and quickly, as the clock is ticking on the insurer to comply with Section 3420, if so required.

The moral of the story is that some insurers will err on the side of caution and comply with Section 3420(d) so long as it might apply, such as in those cases involving a New York injury, despite the policy having been issued to a non-New York insured. You just don’t know if the insured has a substantial business presence in New York” test. And there’s probably not enough time to figure out.

|

|

| |

|

|

|

|

Vol. 7, Iss. 5

June 6, 2018

It Looks, Walks And Quacks Professional -- But It’s Not A “Professional Service”

|

|

|

|

Whether conduct by an insured qualifies as a “professional service” can have a far-reaching impact in insurance coverage. First, it is the touchstone of the entire body of professional liability claims -- regardless of the nature of the profession being insured. The meaning of the term also arises with frequency in the context of determining whether a certain act of the insured is excluded from coverage by a “professional services” exclusion in a commercial general liability policy. For these reasons, the number of decisions addressing the issue are numerous. They can also be all or nothing when it comes to the availability of coverage.

Figuring out if an insured’s conduct was “professional” or “non-professional” can be no easy task. Disputes in this area are frequently fact intensive and often involve conduct undertaken by the insured, in one way or another, in the course of his or her profession. In other words, any insurer attempting to prove that certain conduct of a doctor was non-professional will likely have to overcome the fact that the insured was wearing a white jacket when it was committed.

Moreover, some courts also conclude that, notwithstanding that the insured was performing an activity that required specialized knowledge or training -- the earmark of a professional service -- the act in question nonetheless did not qualify as a “professional service,” because it involved the commercial, and not the professional, aspect of the insured’s business.

In Lindsey Financial v. American Automobile Insurance Co., No. E067037 (Cal. Ct. App. May 8, 2018), the California Court of Appeal recently addressed whether the acts of a financial planner qualified as a professional service for purposes of an Errors and Omissions Policy. The case demonstrates how complex the issue can be and that an insured can clearly be performing a service as a professional, but not performing a covered “professional service.”

The Walkers paid Lindsey Financial $115,000 for financial planning advice. However, the financial plan that Linsey put together – some sort of complex LLC arrangement that’s hard to understand – was known by Lindsey to have been deemed a “tax avoidance scheme” by the Internal Revenue Service.

The Walkers sued Lindsey. Lindsey sought coverage under its Life Insurance Agents Errors and Omissions Policy issued by American Automobile Insurance Co. AAIC denied coverage for a defense and any liability for the reason that the Walkers’ suit did not allege the potential for liability based on the rendering or failure to render “professional services” concerning a “covered product,” as defined under the policy. Coverage litigation ensued. The trial court held that no coverage was owed on the basis that “the alleged wrongful acts within the Walker complaint relate to improper tax advice, with no indication such tax advice involved the tax consequences or benefits in obtaining life insurance or other insurance.”

Lindsey appealed. The appellate court did a nice job of simplifying the definitions of “professional services” and “covered product,” which are rather lengthy in their full versions: “The AAIC policy defines ‘Professional Services,’ in pertinent part, as ‘[p]roviding advice or consulting solely related to a Covered Product, including financial planning or consulting solely related to a Covered Product . . . .’ ‘Covered Product’ means certain products offered by a ‘Product Provider,’ and includes ‘[l]ife [i]nsurance products’ but not variable life insurance products.”

The appeals court affirmed: “The Walker complaint did not assert any claims based on or arising out of Lindsey’s ‘financial planning or consulting solely related to a Covered Product.’ Instead, it asserted fraud and other tort claims based on Lindsey’s financial planning and consulting services in connection with the so-called ‘tax avoidance scheme’—using the LLC and the tax exempt entity to reduce the Walkers’ tax liabilities. As alleged in the Walker complaint, Lindsey’s financial planning and consulting services were not ‘solely related to’ any ‘Covered Product.’ Indeed, Lindsey’s complained-of financial planning and consulting services to the Walkers had nothing to do with any ‘Covered Product.’”

Further, the appeals court observed that, not only were the claims not covered, but they were also excluded under the policy, based on an exclusion for tax advice or financial planning services that were not directly related to a Covered Product.

But, as Lindsey saw it, it wasn’t as simple as this. In support of coverage, Lindsey pointed to its Financial Planning Agreements with the Walkers, which provided that “Lindsey would ‘review and analyze,’ among other things, the Walkers’ ‘life and disability insurance,’ ‘estate and tax planning,’ ‘fee planning needs,’ and ‘money management and investment portfolio,’ all as part of a ‘substantive and comprehensive discussion integrating relevant options and possible solutions in regards to [the Walkers’] Financial Status, which shall include the following financial aspects as they relate to [the Walkers’] needs: i) Insurance; . . . v) Retirement planning.”

But while Lindsey’s pointed out that its Financial Planning Agreements with the Walkers discussed insurance, that was not the test for coverage as the court saw it: “This argument is unavailing, because the Walker complaint did not allege a claim arising out of a ‘Wrongful Act’ by Lindsey in connection with Lindsey’s solicitation for sale, recommendation, negotiation, or other act in connection with any covered product, including any insurance or individual retirement annuities. Instead, the Walker complaint alleged claims based solely on Lindsey’s tax advice and financial planning services rendered in connection with the ‘tax avoidance scheme’ involving the Walkers’ use of the LLC and tax exempt entity to reduce their tax liabilities. The AAIC policy both did not cover and expressly excluded coverage for these claims.”

The services performed by some professionals can be varied and seemingly far afield from their core profession. But insureds can likely explain why they are still related to what they do as professionals. The moral of the story for insurers that issue professional liability policies is clear – defining “professional services” in specific terms [as opposed to generally, or, worse, not at all] will enable them to limit their exposure to intended professional services. Just because an insured is performing a service as a professional may not make it a covered “professional service.”

|

|

| |

|

|

|

|

Vol. 7, Iss. 5

June 6, 2018

Insurer Has Right To Settle. Insured Refuses To Sign The Settlement Agreement:

Now What?

|

|

|

|

It is widely acknowledged that an insurer does not need its insured’s consent to settle a claim under a general liability policy. Professional liability policies can be a different story. But for CGL policies the insurer calls the shots. The insured may not be happy about the settlement, and object to it, but its hands are tied. [I’m sure that people can tell me exceptions, but I’m speaking of the general principle.]

But this can be easier said than done. What happens when the insurer wants to settle a claim and the insured objects. The insurer responds that it can, and will, settle over the insured’s objection. But then what happens when the insured, given its displeasure over the situation, refuses to sign the settlement agreement? Hasn’t the insured just used the back door to obtain a right for which the front door was bolted shut?

This was the situation in McCain v. Promise House, Inc., No. 05-16-714 (Ct. App. Tex. May 2, 2018). In December 2014, Glen McCain sued Promise House, a residential social services care facility, alleging various claims after his eleven-year-old son was physically and sexually abused by an “older male individual” while a resident of the facility.

Promise House had a commercial general liability insurance policy with Arch Insurance that contained a “sexual or physical abuse liability endorsement.” Arch retained counsel to defend Promise House. The following month, counsel for Promise House sent a letter to McCain’s counsel, confirm a $400,000 settlement and stating that the settlement will be memorialized in a final settlement agreement. Counsel for Promise House signed the letter as did McCain’s counsel. This is called a Rule 11 Agreement.

Promise House objected to the settlement and stated that it refused to sign the settlement agreement. McCain’s counsel filed the Rule 11 agreement with the court and asserted breach of contract claims against Promise House and Arch. The trial court found for Promise House.

The Texas appeals court reversed. Putting aside how it got there, the appeals court discussed whether the Rule 11 Agreement was enforceable and held that it was.

Turning to the consent issue, the court stated the widely acknowledged rule that “[w]hen the language of an insurance contract unambiguously vests the insurer with an absolute right to settle third-party claims in its own discretion and without the insured’s consent, we will not engraft any consent requirement onto the contract.” Further, lest there be any doubt about this, the court went on: “[T]he policy did not provide Promise House the right to object to any settlement. By purchasing a policy that did not provide Promise House the right to veto settlement of third-party claims, Promise House gave up the right to complain that any settlement Arch entered somehow damaged Promise House.”

But what about the practical issue -- Promise House refused to sign a formal settlement agreement. This was not necessary, the court concluded, as the Rule 11 Agreement was enough to constitute a final settlement. But what about the fact that Promise House did not sign the Rule 11 Agreement. Also not necessary, the court concluded: “An insurer which, under the terms of its policy, assumes control of a claim, investigates the claim and hires an attorney to defend the insured, becomes the agent of the insured and the attorney becomes the sub-agent of the insured.”

|

|

| |

|

|

|

|

Vol. 7, Iss. 5

June 6, 2018

Shoulda Bought Key Issues: Insurer Drops The Ball On The Independent Counsel Rule

|

|

|

|

For the most part, an insured must prove that a reservation of rights creates a conflict before it is possibly entitled to independent counsel at the insurer’s expense. There are a handful of states where a reservation of rights, despite the specifics of the situation, creates a per se conflict, automatically giving rise to the insured’s right to independent counsel. One of those states is Mississippi, as established by the Mississippi Supreme Court’s 1996 decision in Moeller v. American Guarantee. The 4th edition of Insurance Key Issues discusses Moeller and its progeny. See Vol. 1, pp. 242-43. [Shameless plug. Sorry.]

But the insurer in Grain Dealers Mut. Ins. Co. v. Cooley, No. 17-60307 (5th Cir. May 14, 2018) retained counsel for its insured, in a Mississippi case, and did not offer the insured the right to select its own counsel to defend the claim. The insurer was penalized for this violation of the Moeller rule. However, the decision can be read as one that is pro-insurer.

The Cooleys, the former owners of a gas station, sought coverage from Grain Dealers Mut. Ins. Co. for an environmental contamination claim brought by the Mississippi Department of Environmental Quality. Grain Dealers responded by stating that it owed no coverage for any clean-up costs, but would provide a defense. Grain Dealers hired an attorney to defend the Cooleys, but did not offer them, ala Moeller, the opportunity to hire an attorney of their choice.

The MDEQ concluded that the Cooleys and Pine Belt Oil Co., the purchaser of the Cooley’s gas station, must remediate the spill site. “The order stated that if the Cooleys were ‘aggrieved’ by that conclusion they could ‘request a hearing before the [MDEQ] . . . within 30 days after the date of [the] Order.’ Neither the Cooleys nor Grain Dealers’ hired counsel did so. Nor did Grain Dealers’ hired counsel inform the Cooleys of their right to request a hearing.”

Years later Pine Belt demanded indemnification from the Cooleys for the cost of compliance with the MDEQ order. The Cooleys sought coveage from Grain Dealers, which denied the request, citing a Total Pollution Exclusion. Grain Dealer filed a declaratory judgment action seeking a determination of no duty to defend or indemnify.

At issue was the impact of the failure of Grain Dealers to offer the Cooleys independent counsel. The trial court held that this failure did not estop Grain Dealers from denying coverage as the Cooleys were not prejudiced by the lack of independent counsel.

The Fifth Circuit disagreed. First, the appeals court rejected the insurer’s argument that it was not a Moeller situation: “Grain Dealers argues that Moeller does not control because Grain Dealers did not defend under a ‘reservation of rights.’ The Moeller court, however, was concerned with conflicts that occur when an insurer provides a defense ‘while at the same time reserving the right to deny coverage in event a judgment is rendered against the insured.’ We see no relevant distinction between Grain Dealers’ outright denial of coverage from the start versus a reservation to later deny coverage. Grain Dealers’ refusal to ultimately cover the claim creates the same conflict of interest addressed in Moeller.”

More importantly, from a global and offering a take-away standpoint, the court held that the Cooleys were prejudiced by the lack of independent counsel: “Grain Dealers’ attorney never informed them of their right to challenge the MDEQ decision. That right has since lapsed. The loss of the right to challenge the underlying administrative order with the benefit of non-conflicted counsel is clearly prejudicial.”

While Grain Dealers lost, and the entire affair was caused by its failure to comply with Moeller, the decision is actually pro-insurer. While Moeller mandates that a reservation of rights automatically gives rise to the insured’s right to independent counsel, Cooley rejects the notion that a failure to follow Moeller mandates estoppel of the insurer’s right to apply coverage defenses. The insured must prove that it was prejudiced by the Moeller violation. While that was easily doable here, it is unlikely to be so easy in most situations, as panel counsel will likely handle the case in the similar manner as independent counsel. Grain Dealers lost the battle. Insurers won the war.

|

|

| |

|

|

|

|

| |

|

|

Words You’ll Only Hear In A Coverage Decision

“This case has been pending for nearly three decades.” Johnson Controls, Inc. v. Central National Ins. Co., No. 2014AP2050 (Wis. Ct. App. April 25, 2018).

Being Wrong Is Not Bad Faith

Given that some policyholder counsel are so fond of alleging that a wrongful coverage determination is bad faith, it never hurts to see another court make this observation: “In their summary judgment briefs, the parties agreed that the disposition of the bad-faith claims turned on whether plaintiff’s conduct in declining to defend WARF in the underlying litigation and subsequent refusal to pay on the policy was based on a ‘reasonable or plausible interpretation of the policy.’ (citation omitted). Here, plaintiff’s interpretation of the applicable exclusions was ultimately incorrect, but it was not unreasonable. For example, a letter mailed to WARF’s counsel on December 30, 2014, parsed the policy language and provided relevant case law in an effort to justify why plaintiff was not obligated to defend the underlying suit.” Scottsdale Ins. Co. v. Byrne, No. 16-11435 (D. Mass. May 2, 2018).

Court Changes Its Mind: Goes From Pro-Rata To All Sums Allocation

On November 15, 2016, the Eastern District of Missouri, in Zurich v. Ins. Co. of America, predicted that Missouri courts would apply pro-rata allocation to coverage for an asbestos bodily injury claim that triggered multiple policy years. Subsequently, the Missouri Court of Appeals held in Nooter Corp. v. Allianz Underwriters that “all sums” allocation applied to an asbestos bodily injury claim that triggered multiple policy years. The court in Zurich v. Ins. Co. of America, No. 14-1112 (E.D. Mo. May 8, 2018) responded to Nooter: “Missouri law requires an ‘all sums’ allocation method to hold targeted-insurer ZAIC liable for the entire asbestos exposure loss incurred by its insured A-B [Anheuser-Busch]. Justice requires that the interlocutory Order of November 2016 be vacated. Because Nooter holds that the targeted insurer is liable to its insured for the entire loss under an ‘all sums’ policy, ZAIC is liable to its insured A-B for the entire amount of the settlement and defense costs, and it may not avoid its obligations under the contract through equitable contribution from the insured.”

Wisconsin Supreme Court: Failure to Train/Supervise Not An “Occurrence”

A lot of ink has been spilled lately addressing Liberty Surplus Insurance Co. v. Ledesma and Meyer Construction Co. Inc., currently pending before the California Supreme Court. The court is poised to answer whether a construction company’s negligent hiring and supervision of an employee, who sexually assaulted a student at a middle school, where the company had been working, qualified as an accident (occurrence) for purposes of a CGL policy. The case was argued in early March and the decision is highly anticipated, especially since it may shed light on the larger question, under California law, of what’s an accident, and not simply the narrow negligent supervision question presented.

But while all eyes have been on Ledesma, the Supreme Court of Wisconsin quietly got the scoop. On May 11th the highest court in the Badger State held in Talley v. Mustafa, No. 2015AP2356 (Wis. May 11, 2106) that “[w]hen a negligent supervision claim rests solely on an employee’s intentional act of assault and battery without any separate basis for a negligence claim against the employer, no coverage exists.” In other words, if it’s not an accident when an employee strikes someone in the face, the employer’s failure to prevent the assault is also not an accident.