|

|

|

|

|

| |

|

Vol. 8 - Issue 10

November 20, 2019

|

|

|

|

|

|

| |

Not long ago I had the thrill of interviewing John Grisham in New York about his latest book – The Guardians. It is a classic Grisham thriller. A burned out public defender travels the country seeking to get the wrongly convicted exonerated. Of course, lots of twists and turns along the way. The book debuted at #1 on The New York Times best seller list.

The interview appeared on Law.com. Check it out here: |

| |

|

| |

|

|

|

Vol. 8 - Issue 10

November 20, 2019

Thanksgiving Special: Keeping The Turkey Safe

Encore: The Coverage Opinions Interview With Brian Rodgers - Director of Safety And Risk Management For Butterball, LLC

|

|

|

| |

Way back in November 2013, before you were probably a Coverage Opinions subscriber (and when I did insurance-related interviews), I spoke to Brian Rodgers, Director of Safety and Risk Management for famed turkey producer Butterball. Who better to speak to, about avoiding the risks of Thanksgiving, than the man in charge of keeping the guest of honor safe!

Has anyone ever choked on that little plastic thermometer that pops up to tell you when the bird is ready to come out of the oven? I’ve always wanted to know that. Of course I asked him.

Check out my interview, talking turkey with Butterball’s Director of Safety and Risk Management.

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Vol. 8 - Issue 10

November 20, 2019

|

|

|

|

|

|

| |

Believe me. I was shocked too. The folks at Macy’s are huge Randy Spencer fans and decided to show their love by including him in this year’s Thanksgiving Day Parade. Talk about a miracle on 34th Street.

To make room for their favorite insurance stand-up comic, this year Snoopy will be sitting on the sidelines. I am sure there won’t be a single kid who asks where’s Snoopy? But they’ll love Randy Spencer. Who knows? This could lead to Randy Spencer plush toys and action figures!

[Kudos to Frank Balderrama of Balderrama Design, Coverage Opinions’s web designer, web master and graphic artist for this brilliant work! Frank has been as much a part of CO as me since day 1. If you need an amazing website designer, with incredible graphic skills, you could not do better than Frank.] |

| |

|

| |

|

|

|

|

Vol. 8 - Issue10

November 20, 2019

Insurance Coverage For Pants Snug In The Waist

|

|

|

|

|

| |

I don’t know what to make of some menus having calorie counts on them. Of course it’s good information to have. But man, if there was ever a time when ignorance is bliss.

For Roger Winkler, ignorance was bliss. Then he became no longer ignorant. And then he was no longer bliss.

Winkler, an accountant in Kalispell, Montana, was headed home from the office one night when a craving for Mexican food hit. He stopped off at Big Sky Tacos. Perusing the menu, Winkler came upon the restaurant’s 7 Layer Nachos, described as a heap of homemade tortilla chips topped with mounds of salsa, guacamole, cheese, sour cream, refried beans, tomatoes and chili peppers.

Winkler, who considered himself fit and health conscious – 2-3 times a week at the gym – was curious about the calorie count for such gluttony. The menu listed it as just 250.

Winkler could hardly believe his good fortune. But the more he thought about it, it made sense, given that so many of the toppings were vegetables. Winkler ordered the gargantuan platter and savored every chip. In fact, Winkler was hooked and returned to Big Sky Tacos 14 times over the next month. On each visit he indulged in the restaurant’s mammoth delight.

At this point Winkler noticed that his pants were beginning to feel snug in the waist. It seemed curious since he was watching what he ate, as he always had, and making frequent visits to the gym.

On Winkler’s next visit to Big Sky Tacos he noticed that the menu listed the calorie count, for 7 Layer Nachos, as 2,500. It was odd since he had previously seen the calories listed as 250. He asked the manager about the discrepancy. She replied that there had been a printing error on the menus. She thought all of the incorrect menus had been taken out of circulation. But she now knew that one had slipped by. As the manager put it: “Since this is a Mexican restaurant, I guess I should say que sera, sera.”

Winkler was none too pleased with the situation – both that he had been eating such a huge meal for a month and the manager’s flippant attitude about it. Sorry Doris Day, Winkler said to himself. It was not going to be que sera, sera.

Winkler filed suit against Big Sky Tacos. In his complaint, in Roger Winkler v. Big Sky Tacos, District Court of Montana, Flathead County, No. 18-1489, Winkler alleged that Big Sky Tacos misrepresented the calorie count of its 7 Layer Nachos. He asserted claims for violation of all manner of Montana consumer protection statutes. He sought statutory damages and attorney’s fees, as well as “consequential damages caused by weight gain.”

Big Sky Tacos tendered the Winkler complaint to its insurer – Treasure State Mutual Property and Casualty Company. Treasure State disclaimed coverage, asserting that the damages being sought by Winkler were not because of “bodily injury,” “property damage” or “personal and advertising injury.”

Big Sky retained counsel and filed a motion to dismiss. After that was denied, Big Sky, looking to avoid on-going defense costs, reached a settlement with Winkler for $2,500. Outraged that Treasure State Mutual had denied coverage, especially since Treasure State had held its annual holiday party at Big Sky for the past two years, and gotten free jalapeno poppers, Big Sky filed suit against Treasure State Mutual, seeking recovery of its defense costs, the Winkler settlement payment and damages for bad faith.

Both sides filed motions for summary judgment. In Big Sky Tacos v. Treasure State Mutual Property and Casualty Company, District Court of Montana, Flathead County, No. 19-9267, the court granted Big Sky’s motion in part and denied Treasure State Mutual’s.

The court agreed with Treasure State Mutual that the damages being sought, for violation of the Montana consumer protection laws, were not because of “bodily injury,” “property damage” or “personal and advertising injury.”

However, the court concluded that a defense was owed to Big Sky Tacos on the basis that the Winkler suit sought damages because of “property damage.”

The court explained its decision as follows: “Plaintiff in the underlying suit alleged that he sustained ‘consequential damages caused by weight gain.’ Throughout the complaint, he alleged that his pants were snug in the waist on account of eating fourteen orders of 7 Layer Nachos in a one month period. That’s 98 layers of nachos. A reasonable reading of the complaint is that Plaintiff in the underlying action sustained ‘property damage’ because of his snug pants. This qualifies as ‘property damage’ as the definition of that term includes “loss of use of property that has not been physically injured.” Treasure State maintains that, because Plaintiff could still wear his trousers, he did not lose the use of them. However, use of trousers reasonably means the use of them with a degree of comfort desired by the wearer. On account of the actions of Big Sky Tacos, Mr. Winkler lost this ability. He suffered a loss of use of his property.”

The court also denied both parties’ motion for summary judgment on bad faith, concluding that, based on the denial of coverage, fact issues remained on whether damages are warranted for Treasure State Mutual’s decision.

|

That’s my time. I’m Randy Spencer. Contact Randy Spencer at

Randy.Spencer@coverageopinions.info |

|

| |

|

| |

|

|

|

|

Vol. 8 - Issue 10

November 20, 2019

Encore: Randy Spencer’s Open Mic

Thanksgiving And Insurance Coverage: They Go Together Like Peas And Carrots

|

|

|

|

|

|

| |

The amount of time and effort involved in hosting a Thanksgiving dinner is tremendous. Believe me, I know. I see what my wife goes through.

But while she’s crazy-busy dealing with the bird, stuffing, mashed potatoes, three kinds of cranberry sauce, five types of vegetables, side dishes I’ve never even heard of and five different pies (including one with a gluten free crust -- for her annoying cousin Barry, who doesn’t stop talking about cross fit), it’s not like I don’t have my own challenges. The Lions are 3-5 so far this season. And they’re not going to turn into the 1972 Miami Dolphins between now and November 22. Watching that Lions – Bears game is going to be a huge effort for me. It might be more enjoyable to stand at the sink and peel the potatoes.

But that’s not all I have to contend with. It is my job to make sure that the Spencer family’s annual Turkey Day blow-out doesn’t turn into a financial catastrophe worse than taking the Lions with the points. That give me the task of ensuring that our homeowner’s policy provides adequate coverage for all of the risks associated with having 20 people in the house -- each consuming as many as 4,500 calories -- except cousin Barry.

Thanksgiving is rife with risks for which insurance is needed. There are insurance companies named Mayflower Insurance Exchange, Pilgrim Insurance Company, Plymouth Rock Assurance Corp. and Pie Mutual Insurance Co. Really. I’m not kidding. All these companies must do is insure the hazards of Thanksgiving.

Thanks to reading my homeowner’s policy, we had liability coverage for all of the following Thanksgiving dinner mishaps over the years:

Aunt Mildred nearly choked to death on that plastic thing in the turkey that pops up to tell you when it’s cooked. She said she didn’t want to sue Butterball, because it’s her favorite company and “wouldn’t dream of doing that to them.” But she was fine suing me. Coverage was provided for “bodily injury” caused by an “occurrence.”

My wife told her sister that she’s grateful we stopped going to cousin Gladys’s for Thanksgiving because her turkey was always dry. Gladys overheard this, was outraged and sued my wife for defamation. Coverage was provided for “personal and advertising injury.”

Annoying cousin Rex insisted on showing off his new drone, along with pontificating about how drones will be changing the way we live. The drone crashed onto the hood of my neighbor, Frank’s, Jag. Coverage was provided for “property damage” caused by an “occurrence.” Drones may not change the way we live, but one drone changed the way Frank drove for a week. He had a Toyota Corolla rental.

Cousin Mitchell brought all of the gear needed to deep fry a turkey. It’s perfectly safe, he assured me. Coverage provided for the three houses that went up in flames. Cousin Barry commented that that’s what happens when you cook an unhealthy turkey.

My wife, accused by Aunt Shirley of using her mother’s string bean casserole recipe, was sued for theft of trade secrets. Coverage was provided for “property damage” caused by an “occurrence.” [See “Wow! Court Holds That Trade Secrets, Being Tangible Property, Are “Property Damage,” discussed in this issue of Coverage Opinions.]

89 year old Uncle Max told Cousin Cindy’s two-year old son, Cody, that he was going to take Cody’s nose off. Max grabbed Cody’s nose -- but pulled too hard. Cody’s nose was detached. It was alleged that I was responsible because I should have known that Max sometimes pulls too hard on kid’s noses. Coverage was provided for “bodily injury” caused by an “occurrence.”

Potential coverage denial prevented when Uncle Peter stopped me from punching Cousin Phil for saying, for the ninth straight year, that we really ought to have a turducken.

And liability risks aren’t all that should be on your mind. Property losses have abounded too. Once again, thanks to the homeowner’s policy, we were safe and sound in all of the following scenarios.

Uncle Charlie used the fancy guest towels in the powder room. Sure, he was a guest. But even guests aren’t allowed to us them. The guest towels were covered property under an all-risks homeowner’s policy.

Aunt Matilda confused the urn, holding our beloved Scooter’s ashes, with a gravy boat. A cocker spaniel’s ashes are covered property under an all-risks homeowner’s policy. But a dispute arose over how to value them. It’s going to appraisal.

93 year old Uncle Sam fell into a deep tryptophan–induced sleep on the sofa after dinner. A steady stream of saliva dripped out of his mouth for an hour. The stained sofa cushion was covered property under an all-risks homeowner’s policy.

|

That’s my time. I’m Randy Spencer. Contact Randy Spencer at

Randy.Spencer@coverageopinions.info |

|

| |

|

| |

|

|

|

|

Vol. 8 - Issue10

November 20, 2019

Finally: Insurance Key Issues – Half Price Sale!

|

|

|

| |

|

| |

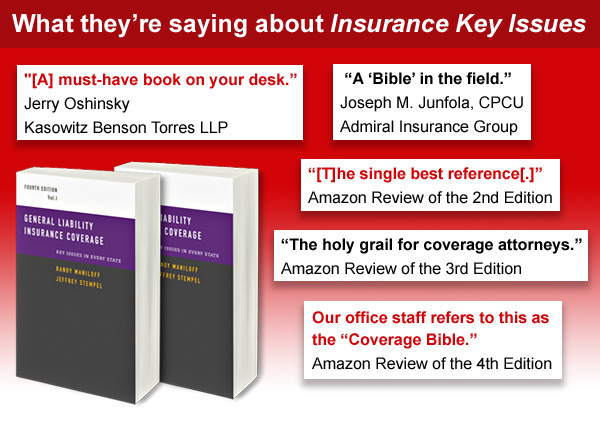

At last, General Liability Insurance Coverage – Key Issues In Every State is on sale. Half price! It took forever for it to go to 50% off, as sales have been humming along at full price. For those of you waiting for the big Insurance Key Issues door buster, here it is! Now’s your chance to see what all of the Key Issues hubbub is about. Or, for those of you who already have a copy, get one for the car. [Warning: Do not read Insurance Key Issues while driving.]

More about Insurance Key Issues and links to purchase on Amazon are here.

[The price listed on Amazon has been reduced by 50%.]

http://insurancekeyissues.com

|

|

| |

|

|

|

|

Vol. 8 - Issue 10

November 20, 2019

The Raccoon Sequel: Squirrels And Insurance Coverage

Meet “Hormone Hunter” - A Very Colorful Lawyer

|

|

|

| |

In the last issue of Coverage Opinions I mentioned the recent Pennsylvania federal decision in Capital Flip, LLC v. American Modern Select Insurance Company, No. 19-180 (W.D. Pa. Sept. 19, 2019), where the court held that no coverage was owed, under a property policy, for damage caused by raccoons that had entered the interior of a structure. The court concluded that coverage was barred as the damage was not caused by the covered peril of vandalism or malicious mischief: “Raccoons and their companions in the animal kingdom,” the court concluded, “cannot formulate the intent needed to engage in ‘vandalism,’ ‘malicious mischief’ or any other criminal or actionable conduct. Animals do not have conscious agency and are not subjects of human law.”

I was delighted to get a note from Coverage Opinions reader Arnold Young, of HunterMaclean in Savannah, Georgia, bringing to my attention a wonderful coverage decision from 1954 from the Court of Appeals of Georgia. It’s not about raccoons – but squirrels. The court found that coverage was owed for damage to a playhouse caused by a squirrel. Why? Because the court had fuzzy feelings for the critter. |

|

|

|

The decision is a gem. I’ll get to that in a second. But that’s just half the story. Arnold shared with me that the insured was represented by his former partner – Colonel E. Ormonde Hunter, who served in WWII and was part of the Office of Strategic Services, the predecessor to the CIA.

Hunter was quite a character, Arnold told me. An absolute gentleman, but tough. He was in the Georgia state legislature and served as vice-chairman of the Board of Regents of Georgia’s state university system.

Known as a bon vivant, Hunter was married for the first and only time at age 65 and, according to Arnold, known around Savannah as “Hormone Hunter.” As Arnold put it, “Only Colonel Hunter would provide a recipe for squirrel stew in an appellate brief.” The Colonel died in 1989 at about age 95.

The court’s decision in North British & Mercantile Insurance Company v. Mercer, 82 S.E.2d 41 (Ga. Ct. App. 1954), aff’d 84 S.E.2d 570 (Ga. 1954) speaks volumes about Colonel Hunter.

A squirrel descended the chimney of an insured’s playhouse and damaged a maple table, chair, brass lamp, lampshades and sofa cushions. Coverage was sought under a policy that insured “all risks or loss of or damage to property” except “loss or damage caused by moth, vermin and inherent vice.”

The insurer disclaimed coverage on the basis that a squirrel is vermin. Suit was filed and the jury returned a verdict for the plaintiff for the amount sued for -- $179.50 -- plus $50 attorney fees for bad faith.

The Georgia appeals court affirmed the verdict by agreeing with Colonel Hunter that squirrels have much to offer society:

“The brief of counsel for the defendant in error (which, incidentally, includes an excellent recipe for squirrel stew) concludes with the following words, with which this court is inclined to agree: “‘Vermin’ is a mighty harsh word to hurl at our little friend the squirrel. He has long been well considered and much thought of as a pet and an attractive addition to the scenery of any city, garden, or country yard. He is praised in song and story as a shining example to mankind of industry and thrift. It is respectfully submitted that this court should not label the little fellow as nothing more that ‘vermin.’”

Thank you to Arnold Young, of HunterMaclean, for bringing this great case and colorful lawyer to my attention.

|

|

| |

|

|

|

|

Vol. 8 - Issue 10

November 20, 2019

Winners Of the Insurance Haiku Contest And Autographed Grisham Book

|

|

|

| |

|

| |

The response to the Insurance Haiku Contest was overwhelming. Haiku contests have always done well, but this one was off the charts. There were about 150 entries! As I said, CO readers love a challenge.

The only downside was that I could not respond to everyone who entered to say thanks and for the kind words about CO that many included. Believe me, I appreciated everything said. And the haikus about me were funny (as was the limerick about me that someone submitted). Please do not think of me as a jerk if I did not reply to say thanks.

With that many entries it was no easy task to choose a winner. After a lot of thought and more thought and hand wringing and asking a colleague for his thoughts, I am pleased to announce the following winners:

First Prize

We reserve our rights

We cite the whole policy

Insured screams bad faith

Bill Sterling

Westfield Insurance

Minneapolis

Bill will get an autographed copy of The Guardians, John Grisham’s just-released legal thriller.

Second Prize

Intentional stabs

Insurer says no cover

Now negligent stabs

Robert Chemers

Pretzel & Stouffer

Chicago

Robert will get a copy of the 4th edition of Insurance Key Issues.

Honorable Mentions

Construction Defect

Will it be an occurrence?

What state are you in?

Gregory O’Brien

Cavitch Familo & Durkin

Cleveland

The policy gives

The exclusions take away

Confusion remains

Andy D’Entremont

Epic Brokers

Birmingham

Within coverage?

If an ambiguity

Answer will be yes

Anonymous

Greg, Andy and Anonymous will have their lives changed by receiving a fantastic Coverage Opinions pen.

Thank you to all who entered!

|

|

| |

|

|

|

|

Vol. 8 - Issue 10

November 20, 2019

Is This Warning Sign Really Necessary?

|

|

|

| |

I came upon this gem of a hotel room warning sign.

I have no doubt that messing with a hotel room fire sprinkler could lead to some problems. But is it really necessary to warn guests not to hang clothes from the sprinkler? When was the last time you stayed in a hotel and had so many things to hang in the closet that you needed to find additional space?

Maybe the problem is that guests were hanging clothes from the sprinkler, to set it off, to use as a washing machine. In that case, there should have been a sign on the microwave warning people not to use it as a dryer.

|

|

|

| |

| |

|

|

|

|

Vol. 8 - Issue 10

November 20, 2019

Court Sanctions Insurer For Adjuster’s Attendance At Mediation -- By Phone

What Does Attendance With “Settlement Authority” Mean?

|

|

|

| |

In Long v. American Family Mutual Ins. Co., No. 19-4036 (D. Kan. Nov. 7, 2019), a federal district court in Kansas addressed questions that I’m sure lots of people have wondered about when it comes to court-ordered mediation. I certainly have.

The court ordered a mediation of a coverage dispute over a residential fire loss. The parties retained a private mediator who reminded them, prior to the mediation, about their obligations under Kansas local rule 16.3(c)(2), which governs who must attend mediation – each party or its representative with settlement authority along with the party’s attorney responsible for resolution of the case.

The insured and its counsel attended the mediation. The insurer’s counsel attended, but without an in-person representative of the insurer. The opinion suggests that the insurer’s representative was available by phone. The insured’s demand was $320,000. The insurer’s counsel had $20,000 in settlement authority. The mediation was not successful.

The insured filed a motion for attorney’s fees and costs, and sought an order for a second mediation, arguing that the insurer did not act in good faith because the insurer’s counsel lacked full settlement authority and by sending only counsel to the mediation.

The court addressed whether a party attends a mediation with adequate settlement authority.

On one hand, the court concluded that it does not mean automatically mean “authority to meet the other party’s demand.” However, that could be a factor in some cases. The court described the test for awarding sanction as follows: “[A] plaintiff seeking sanctions on the basis of the party representative having inadequate settlement authority must, at a minimum, demonstrate that the plaintiff’s settlement demand was reasonable and that the defendant’s settlement offer was unreasonable. Here, Mr. Long has not presented any evidence suggesting that his $320,000 demand was reasonable or that American Family’s $20,000 offer was unreasonable. On the other hand, American Family provides at least some minimal basis for its settlement offer, which Mr. Long addresses only by generally disputing the applicability of the policy exclusions. But, even setting aside whether any policy exclusions apply, the record is insufficient for the court to determine that plaintiff's $320,00 settlement demand is reasonable. So, based on the record, the court cannot find that defense counsel lacked full, meaningful settlement authority solely because he only had $20,000 in settlement authority. The court therefore declines to award sanctions[.]”

However, the insured fared better with its argument that the insurer should be sanctioned for its failure to have a representative present at the mediation. The court ordered the insurer to pay the insured’s counsel’s attorney’s fees and costs of the mediation, explaining its decision as follows:

“American Family does not explain how sending only counsel to mediation met the purpose of mediation outlined in the local rules—‘to improve communication among the parties and provide the opportunity for greater litigant involvement in the earlier resolution of disputes[.]’ D. Kan. Rule 16.3(a). The mediator’s letter to the parties also expressly contemplated attendance by the ‘parties and their counsel’ and reminded the parties that D. Kan. Rule 16.3 governed mediation in this case. If American Family did not intend to bring a client representative with settlement authority to mediation, it should have notified the mediator and Mr. Long about this sufficiently in advance of the mediation so that they could have determined how to proceed, and/or American Family should have sought the appropriate permissions to have the client representative excused from personally attending the mediation. American Family did neither.”

|

|

| |

|

|

|

|

Vol. 8 - Issue 10

November 20, 2019

$6 Million E-Mail Spoofing Claim: Professional Liability Policy Exclusion Does Not Apply

|

|

|

| |

There has been much discussion of coverage for email spoofing losses under crime/computer fraud policies. These are first-party policies and ones that were written before such claims were contemplated. Thus, arguments have abound whether coverage is owed.

As SS&C Technology Holdings v. AIG Specialty Insurance Company, No. 19-7859 (S.D.N.Y. Nov. 6, 2019) demonstrates, e-mail spoofing losses can give rise to liability claims too.

As e-mail spoofing losses go, the one at issue in SS&C Technology Holdings is large dollar. The opinion describes it like this. SS&C is a global provider of software and software-enabled services to thousands of clients, including Tillage Commodities Fund, L.P. "In March 2016, unknown third parties using stolen credentials sent transfer requests via e-mail to SS&C, falsely claiming to be acting on behalf of Tillage. SS&C believed these requests to be from Tillage and processed those requests. As a result, over the course of three weeks, SS&C transferred over $5.9 million from Tillage's accounts to certain bank accounts in Hong Kong, as requested by the fraudsters."

Tillage filed suit against SS&C alleging all manner of causes of action. SS&C was insured under an AIG policy that provided coverage for negligence, errors, or omissions relating to the performance of its professional services. AIG undertook SS&C’s defense but asserted that, based on certain exclusions, it had no obligation to provide coverage for any of SS&C’s liability. SS&C’s effort, to defeat the suit on motions, was not successful. The case settled, for an unstated amount, just prior to trial.

Of relevance here, AIG maintained that exclusion 3(a) excluded “coverage for losses in connection with claims: alleging, arising out of, based upon or attributable to a dishonest, fraudulent, criminal or malicious act, error or omission, or any intentional or knowing violation of the law; provided, however, [AIG] will defend Suits that allege any of the foregoing conduct, and that are not otherwise excluded, until there is a final judgment or final adjudication against an Insured in a Suit, adverse finding of fact against an Insured in a binding arbitration proceeding or plea of guilty or no contest by an Insured as to such conduct, at which time the Insureds shall reimburse [AIG] for Defense Costs.”

As AIG saw it, “Exclusion 3(a) applies not only to ‘dishonest, fraudulent, criminal or malicious act, error or omission, or any intentional or knowing violation of the law’ committed by SS&C, but also broadly to such acts committed by third-party fraudsters, such as here.” (emphasis added).

The court was not convinced. While AIG’s argument, the court noted, may have been successful, based on a reading of a portion of the exclusion, the exclusion, read in its totality, did not apply to such wrongful acts committed by third-party fraudsters.

The court explained its decision:

“But even though reading the first clause in isolation might support AIG’s interpretation, this interpretation falters when the sentence is read in its entirety. For coupling the first clause with the ‘provided, however’ clause of the same sentence clearly indicates that Exclusion 3(a) applies only to dishonest, fraudulent, criminal, or malicious acts committed by SS&C, and not to these such acts committed by third-party fraudsters. This is because the ‘provided, however’ clause, which modifies the first clause, refers specifically to ‘Suits that allege any of the foregoing conduct’ against SS&C. This reading also comports with what the parties most likely intended when they entered into the Policy. Indeed, the very rationale of such exclusionary provisions is that a tortfeasor may not protect himself from liability by seeking indemnity from his insurer for damages, punitive in nature, that were imposed on him for his own intentional or reckless wrongdoing.”

And as with the crime policies, I suspect that most liability policies also did not have email spoofing claims in mind when written. Thus, here too, arguments concerning coverage are likely to arise.

|

|

| |

|

|

|

|

Vol. 8 - Issue 10

November 20, 2019

Passenger Injured By 2 Vehicles, 1 Second Apart = 2 Limits [More Than An Auto Case]

|

|

|

| |

Number of occurrence cases can sometimes be very fact intensive. The Pennsylvania federal court decision in Busby v. Steadfast Insurance Co., No. 19-2225 (E.D. Pa. Oct. 31, 2019) is for sure. The court even made this point. Despite this, it is worthy of discussion here. While the decision involves an auto claim, which I know a lot of CO readers don’t handle and don’t pay attention to, the lesson from the decision could have applicability to general liability claims.

At issue in Busby v. Steadfast Insurance Company, No. 19-2225 (E.D. Pa. Oct. 31, 2019) was the extent of coverage, for a motor vehicle accident, in which a passenger’s vehicle was struck by two other vehicles – one second apart. One limit or two was the issue.

The court described the stipulated facts as follows: “On October 29, 2016, [Robin] Busby was a passenger in the backseat of a 2013 Nissan Altima driven by Thomas Curtain, who Busby had hired as a driver through Lyft, Inc. Curtain was traveling eastbound on the Schuylkill Expressway in the left-hand lane near mile marker 334.3. The traffic came to a stop in front of Curtain’s vehicle. Curtain drove his vehicle into the rear of the car in front of him which was stopped in traffic.

After Curtain hit the car in front of him, a 2005 Dodge Grand Caravan driven by Gerald Crossley collided with the rear of Curtain’s vehicle. Curtain’s vehicle was equipped with an event data recorder which recorded ‘two separate events.’ The data was retrieved and analyzed by plaintiff’s and defendants’ respective experts. The data established that approximately one second had passed between the two crashes. The data also demonstrated that Curtain had been travelling in the left lane for at least six seconds before Crossley hit the rear of Curtain’s car. Curtain’s car was not moving and had come to a complete stop at the time it was rear-ended by Crossley.”

Busby was clearly seriously injured. She settled her claims for an amount not shared, but we are told that she was paid the limit of $1,000,000 under a Steadfast policy issued to Lyft for its drivers, $300,000 as the limit of Crossley’s policy and $200,000 from USAA, her own UIM insurer.

Busby filed suit, seeking an additional $1,000,000 in coverage from Steadfast and an additional $200,000 from USAA for what she terms the “second accident involving the Crossley vehicle.” The insurers responded that the events of October 29, 2016 constituted one accident and, thus, their limits are exhausted. The court’s task was to determine whether Busby was involved in one or two motor vehicle accidents.

Starting with the policy language, as it should, the court stated that the “Steadfast policy provides an aggregate limit of one million dollars in liability and UIM coverage for each ‘accident.’ It defines accident as ‘continuous or repeated exposure to the same conditions resulting in ‘bodily injury’ or ‘property damage.’” The USAA policy does not define “accident," so the court turned to how the term is treated under Pennsylvania law: “an unexpected and undesirable event occurring unintentionally.”

The court reviewed Pennsylvania law and concluded that its arithmetic was to be governed by the “cause test.” This is not a surprise as Pennsylvania number of occurrences law goes.

But even under the “cause test,” the court concluded that there were two accidents. The key to the court’s decision – here and for purposes of possible further impact of the decision – was its conclusion that one accident was not the proximate cause of the other: “Even if Curtain had stopped the Lyft vehicle prior to striking the back of the vehicle in front of him, Crossley still would have rear-ended Curtain’s vehicle. The crash caused by Curtain was not the proximate cause of the crash caused by Crossley. Nor were the two crashes one continuing and uninterrupted cause. In the words of our Court of Appeals, there simply was not ‘one proximate, uninterrupted, and continuing cause which resulted in all of the injuries and damages.’”

As for the language in the policy that, regardless of the number of vehicles involved in the accident, the most the insurer will pay for all damages is the accident limit, the court concluded that its purpose was “merely [to] make clear that an ‘accident’ may involve multiple vehicles.” It did not speak to whether there was one or two accidents.

The court was quick to note that its decision was fact intensive, the situation at issue quite unique and not akin to a chain reaction crash, where one car goes into another which goes into another. That, even Busby acknowledged, would have been one accident.

It is easy to see why an insurer would treat this as a single accident – the multiple vehicle policy language, Pennsylvania’s “cause test” and a one second gap between the collisions. But the court resisted all of those invitations and came to a different conclusion.

|

|

| |

|

|

|

| |

|

Vol. 8 - Issue 10

November 20, 2019

Supreme Court: Walking To Your Vehicle Is Not “Occupying” It (Really)

|

|

|

| |

Necessity is the mother of creative arguments for insurance coverage. Clearly that was what drove the insured’s argument in Lavoie v. Peninsula Insurance Companies, No. 2018-0711 (N.H. Nov. 8, 2019). It was not successful. But the insured made the most of what it had to work with, which wasn’t a lot.

David Lavoie was struck by a vehicle while crossing the first of two streets between him and his insured vehicle. He was covered only if he had been “occupying” the vehicle at the time of the accident. The policy in fact defined “occupying,” which is “in, upon, getting in, on, out or off.” I would have thought the definition was simpler -- “sitting in it.” But, it was broader than that, which opened the door to Mr. Lavoie arguing that “occupying” a vehicle includes walking toward it.

You are no wondering what the insured argued to make this leap: “Here, the plaintiff acknowledges that he severed his connection with the vehicle when he left it to go to dinner. He argues that he ‘reconnected’ with the vehicle when he finished dinner and began walking toward the vehicle to retrieve a tire that he had repaired at the request of one of his customers — a dinner companion — because his ‘physical orientation was in the direction of the Vehicle and his conscious attention was oriented on the Vehicle.’ He contends that whether he was ‘getting in’ the vehicle depends, not upon ‘a myopic review of the facts,’ but upon his, apparently subjective, ‘perspective on where he was going and what he was doing’ when injured. He places no limit on how long one can be ‘vehicle oriented’ or on what one can do while being ‘vehicle oriented.’”

But the court concluded that Mr. Lavoie was not “occupying” the vehicle as he did not satisfy the “vehicle orientation” test: “This test requires that a claimant be engaged in an activity essential to the use of the vehicle when the accident occurs. A claimant need not have physical contact with the vehicle to be ‘occupying’ it. ‘Occupying’ may include the process of moving away from the vehicle to a ‘place of safety,’ but does not include the process of moving away from the vehicle when no unsafe condition exists. If a claimant has severed connection to the vehicle, then the claimant is no longer occupying the vehicle. To be ‘occupying’ a vehicle, the claimant must be ‘vehicle-oriented’ as opposed to ‘highway oriented’ or ‘sidewalk oriented.’ Subtle factual distinctions can make the difference in questions of coverage.” (citations omitted).

The court made the obvious observation that “plaintiff’s position would result in coverage any time a claimant was traveling toward the insured vehicle, regardless of how long the claimant journeyed before reaching the vehicle or what he did during the journey.”

While I didn’t think much of Mr. Lavoie’s argument, maybe I’m not much different. When my wife asks me to clean out the attic, I respond that I am thinking about doing it. And somehow I expect her to believe that that’s enough.

|

|

| |

|

|

|

| |

|

|

|

Vol. 8 - Issue 10

November 20, 2019

Court Teaches A Coverage Lesson From Porky’s Cabaret’s “Back To School Party”

|

|

|

| |

Ordinarily, as we all know, whether an insurer has a duty to defend is based on a comparison between the policy and, depending on the jurisdiction, complaint or complaint and extrinsic evidence. In either case, the policy says what it says, the complaint says what it says, and you do the comparison to determine if a defense duty is triggered. Of course, an analysis of case law, addressing the relevant coverage issue, may be included in the calculus.

But once in a while, answering the duty to defend question requires a further step. In addition to comparing the complaint (and perhaps extrinsic evidence) with the policy, there can be a requirement to examine substantive issues in the underlying action -- and perhaps undertake legal research.

This was the duty to defend scenario in AIX Specialty Ins. Co. v. Dginguerian, No. 18-24099 (S.D. Fla. Sept. 20, 2019). A comparison, between the underlying complaint and the policy, revealed no duty to defend. But then the court, in the coverage case, started asking questions about the underlying complaint and did some legal research. When it was finished, the duty to defend had been triggered.

The facts are set out by the court as follows: “Ms. [Sara] Underwood is a model, actress, and television host. She has modeled for Playboy magazine and appeared in films and several episodes of reality television programs. Ms. Underwood alleges [Porky’s] Cabaret posted a stolen image of her to its Facebook page on August 26, 2014, to advertise for a ‘back to school party,’ implying Ms. Underwood was a stripper at Cabaret. She further alleges Xcitement magazine posted an image of her on August 26, 2014 as part of an advertisement for Cabaret, insinuating Ms. Underwood was a stripper for Cabaret. According to Ms. Underwood, Cabaret did not seek permission to use her image, and she was never hired by nor compensated to advertise for Cabaret.”

Ms. Underwood filed suit against Porky’s Cabaret setting forth causes of action for (1) violations of the Lanham Act (False Advertising and False Endorsement; (2) violation of Florida Statutes concerning “Right of Publicity” and “Unauthorized Misappropriation of Name/Likeness;” (3) violation of the “Common Law Right of Publicity” for “Unauthorized Misappropriation of Name and Likeness;” (4) conversion; and (5) unjust enrichment.

At issue in the coverage case was the availability of coverage for Porky’s Cabaret for “personal and advertising injury.” The insurer argued that it had no duty to defend or indemnify the Cabaret.

The policy included an Intellectual Property exclusion, which precludes coverage for “personal and advertising injury” arising out of the infringement of copyright, patent, trademark, trade secret or other intellectual property rights.

Reading various policy provisions together, the court explained that coverage for personal and advertising injury “includes damages arising from (1) oral or written publication that slanders or libels a person or organization or disparages a person’s or organization’s goods, products or services; (2) violations of privacy; (3) use of another’s idea in the insured’s advertisement; and (4) copyright, trade dress or slogan infringement. And read together, coverage for personal advertising injury excludes damages arising from (1) patent, trade mark, and trade secret infringement; and (2) other intellectual property rights.”

Here’s where the duty to defend analysis went beyond simply comparing the insurance policy to the complaint. Ms. Underwood brought several causes of action, but none of them were for defamation. However, as Porky’ Cabaret put it, the underlying claims “sound in defamation.”

The court agreed, describing Ms. Underwood’s allegations as follows: “Ms. Underwood alleges Cabaret published a ‘stolen image of Underwood’ on its Facebook page to advertise for a ‘back to school’ party. She alleges Cabaret used the picture ‘to intentionally give the impression that Underwood is either a stripper working at the strip club or that she endorses [Cabaret].’ According to Ms. Underwood, this publication ‘impugns [her] character, embarrasses her and suggests — falsely — her support for and participation in the strip tease industry.’ She further alleges Cabaret’s publication ‘has caused irreparable harm to [Ms. Underwood’s] reputation and brand by attributing to [her] the adult entertainment and striptease lifestyle and activities at [Cabaret’s] strip club.’”

In concluding that Ms. Underwood asserted a claim for defamation, despite not including one specifically, the court considered the crux of Ms. Underwood’s allegations, in conjunction with an examination of the elements of defamation under Florida law (and related case law).

The test for the duty to defend, the court observed, can include the “fairly read grounds for liability expressed by allegations of fact in the underlying complaint — not the specific label of the cause of action.” To carry this out, the court delved into the law at issue in the underlying action.

Porky’s Cabaret instructs that, in certain cases, determination of the duty to defend can expand from the usual task, of comparing the complaint (and perhaps extrinsic evidence) with the policy, to undertaking an analysis of legal issues and grounds for liability in the underlying action.

|

|

| |

|

|

|

|

| |

|

|

Insurer Can’t Hand Over Limits And Bid Adieu-T To Defend

In United States Fire Insurance Company v. Mother Earth School, No. 18-1762 (D. Ore. Oct. 31, 2019), the court concluded that the insurer’s duty to defend was not extinguished after it deposited into the court’s registry $100,000 – the amount the insurer believed it owed in coverage for an underlying suit. Putting aside that the court was not convinced that the insurer’s maximum liability was capped at $100K – that remained to be seen -- the court was not persuaded that the insurer could drop off its limits and wash its hands of its duty to defend:

“[T]he policy provides, in relevant part, that the ‘right and duty to defend ends when [Plaintiff] ha[s] used up the applicable limit of insurance in the payment of judgments or settlements[.]’ Plaintiff does not argue that ‘judgment’ or ‘settlement are ambiguous terms, subject to more than one plausible interpretation. Instead, Plaintiff argues that payment of a sum into the court’s registry ‘is tantamount to settlement,’ therefore extinguishing Plaintiff's duty to defend. Plaintiff provides no relevant authority to support this argument.

The policy does not define ‘judgment’ or ‘settlement.’ When a policy does not define a particular term, a court may look to dictionary definitions to ascertain the term’s plain meaning. Black’s Law Dictionary defines ‘judgment’ as ‘[a] court’s final determination of the rights and obligations of the parties in a case.’ The term ‘settlement’ is defined as ‘[a]n agreement ending a dispute or lawsuit.’ Under these definitions, Plaintiff's payment of $100,000 into the court’s registry is not a payment of judgment or settlement. . . . Thus, Plaintiff's duty to defend Defendant Mother Earth School remains active at this time.”

What Is A Consumer Protection Law For Purposes Of An Exclusion

In Evergreen Real Estate Services, LLC v. Hanover Ins. Co., No. 1-18-1867 (Ill. Ct. App. Nov. 4, 2019), the court rejected the insurer’s argument that no coverage was owed to a real estate manager, under a professional liability policy, for claims that the insured violated the Chicago Residential Landlord Tenant Ordinance (RLTO). The insurer argued that coverage was precluded on account of an exclusion for claims arising from “unfair or deceptive business practices” including “violations of any local, state or federal consumer protection laws.”

The court concluded that the exclusion did not apply on the basis that the RLTO is not a consumer protection law: “Consumer protection laws are designed to protect the public—the purchasers of goods and services—against oppressive practices by merchants. The RLTO, on the other hand, has the purpose of balancing the rights and obligations for both tenants and landlords. For example, the principal consumer protection law in Illinois, the Illinois Consumer Fraud and Deceptive Business Practices Act (815 ILCS 505/1 et seq. (West 2016)) was enacted as a regulatory and remedial statute for the purpose of protecting consumers and other purchasers of goods and services against fraud, unfair methods of competition, and unfair or deceptive acts or practices in the conduct of any form of trade or commerce. The RLTO meanwhile is a two-way street enacted to ‘establish the rights and obligations of the landlord and the tenant’ and to ‘encourage the landlord and the tenant to maintain and improve the quality of housing.’ Both landlords and tenants derive direct benefit from the RLTO, while only purchasers of goods and services derive direct benefit from consumer protection laws.”

|

| |

|

|

|

| |

|

|

|

|

|

|

|

|

|