|

|

|

|

|

|

Vol. 8 - Issue 2

February 6, 2019

|

|

|

|

|

|

| |

“What does Larry want to hear?,” Anthony Scaramucci had asked himself. He’s explaining to me his final exam strategy that led to an A- in Laurence Tribe’s Constitutional Law class. “He wants to hear left-leaning judicial activism. So I wrote left-leaning judicial activism and tons of pablum and liberal shibboleths.” [Professor Tribe responds below.]

While Scaramucci went on to graduate from Harvard Law School, he is much better-known for something less cerebral – the eleven days he spent as White House director of communications for President Donald Trump. There are Jimmy Page guitar solos that have lasted longer.

Scaramucci’s tenure in the West Wing came to a quick halt after a profanity-laced telephone tirade to a New Yorker reporter about White House leaks, including an offensive statement about the President’s chief strategist, Steve Bannon. Scaramucci had thought the call was off the record. The reporter didn’t. Scaramucci was sent packing.

But I’m not sitting with the man known as “the Mooch” [“call me Mooch,” he says] to talk about his time in D.C. or the President for whom he worked. I have two pages of questions in front of me. Trump’s name appears nowhere.

Scaramucci’s father made his living shoveling sand that would become cement. He suffered a cut in pay during an economic downturn in the mid-1970s. Feeling the financial anxiety in the house, the eleven-year-old Scaramucci began delivering “Long Island Newsday.” Today the former paperboy and I are in a conference room in the Midtown Manhattan office of SkyBridge Capital, the hedge fund company he founded in 2005. It has just under $10 Billion in assets under management. On the same day as our meeting, a Bloomberg headline read: “In Awful Year for Hedge Funds, Scaramucci’s SkyBridge Made Money.”

“My father had a shovel in his hand,” Scaramucci tells me. “I’m going to Harvard Law School. That’s the American dream.” This is the story I’ve come to hear.

Over forty-five minutes, Scaramucci, gracious, funny, R-rated and in constant motion – manning two cell phones, directing his assistant, organizing a trip down town with another colleague, showing me pictures, trying to Face Time a friend and signing copies of his new book -- shared with me his journey from wrapping rubber bands around newspapers to the upper echelons of Wall Street.

Anthony Scaramucci has traveled a very long way. But not really. He’s still just a paper boy from Long Island.

|

| |

|

| |

“I Never Bought Into This Garbage”

The 55-year-old Scaramucci grew up in the Long Island, New York town of Port Washington, seventeen miles from Manhattan. The neighborhood was blue collar. His parents spoke mainly Italian in the house. But wanting their children to assimilate, Scaramucci and his siblings were not permitted to. His father, in addition to working in the sandpits, held a second job for most of his early adult life. “My parents didn’t even know it was Harvard Law School,” he says. “They thought it was Hartford Law School. There were no books in my house, you got that?”

Scaramucci understood early-on his family’s finances. It led to a paper route that would alter his life. His memory for this four decades ago experience is remarkable. Scaramucci explains that he arranged with his manager to get some free papers that he would deliver to non-subscribers. The next day he knocked on the recipients’ doors and sought to close the deal: “Mrs. Smith, how are you. It’s Anthony again. You know, Marie’s kid. How did you like the paper? And, by the way, do you want it daily or daily and Sunday or Sunday only?”

Scaramucci also saw an opportunity to increase his sales of “Newsday” by expanding into apartment buildings. “I used to go into the apartment buildings,” he explained. “My friends weren’t going into the apartment buildings. . . . The apartment buildings were a little lower class. But so what. I’d knock on the doors. ‘You guys need the paper.’”

Such entrepreneurship led Scaramucci to grow his paper route into the largest in town. But it offered more than just some money: “There was no better feeling than converting one of these people into a first time customer. . . . I loved the sense of pride I felt in building something. Of hustling day-in and day-out to earn my keep. Of being my own boss.”

Scaramucci’s White House financial disclosure form reveals a man who is wildly rich. But his blue collar roots are not for sale. On wealth, Scaramucci tells me, “your brain gets distorted. What happens is you think you’re grounded, you’re not an elitist, but you’re becoming an elitist because you’re hanging out with rich people. You have to be really careful.”

“I live two miles from my parents. I never bought into this garbage. It’s the way you stay grounded,” Scaramucci says. “I can’t have [my children] turn out like some of these people,” he says, pointing to the affluence outside his Madison Avenue office. “I don’t want my kids to be entitled train wrecks.” They need to work hard so they don’t end up as “rich dilettantes.”

Scaramucci speaks about his parents with reverence. But he can’t help poking a little fun at his 82-year-old mother. He tells me he renovated his parents’ house. But his mother wouldn’t let him take down the paneling in the living room. “Carol Brady called from The Brady Bunch,” Scaramucci says. “She wants her paneling back.” Scaramucci picks up his phone to show me a picture of his mother with President Trump. It’s in a frame hanging on her living room wall. Paneling.

Harvard Law School

Scaramucci entered Harvard Law School in 1986. It was a short trip from Tufts where he graduated with a degree in economics.

But despite signing up at the nation’s most renowned law school, Scaramucci had no interest in being a lawyer. Indeed, he has described his summer at Hughes Hubbard & Reed in New York, between Tufts and Harvard, where he did document review, as “a mind-numbing, soul crushing and career-questioning experience.”

So I ask Scaramucci the obvious question. “Survival.” That’s the reason he went. “It wasn’t like I was this intellectual genius. Oh I’m going to become Antonin Scalia.”

In 1985 Scaramucci had seen an article in Time that Cravath, Swaine & Moore was paying lawyers, right out of law school, $65,000 per year. Despite having always wanted to run his own business, he had experienced a lifetime of “financial anxiety.” He now knew what he’d be doing after Tufts. “I anchored myself to law school because I figured if I’m a professional, and everything goes bad for me, and I have this law degree and bar exam passed, I’ll be able to practice law somewhere.” Borrowing an investment term, Scaramucci descried law school as a “financial put” on his future career.

While Scaramucci figured out how to tackle Professor Tribe’s Con Law final, he shares the story of a very smart, conservative friend, who didn’t. Scaramucci starts out by calling him “genius guy.” Unlike Scaramucci, who gave Tribe what he thought the legendary Constitutional scholar wanted to hear, “genius guy,” he explains, “is writing constitutional originalism.” Scaramucci shares the fate of his friend: “My poor genius guy, he gets a B and it says ‘a hopeless equivocation,’ on the top of his essay. And I got an A- and it said ‘quite a few good points.’”

[I reached out to Professor Tribe for comment. He provided the following: “Mr. Scaramucci is making things up if he says what you quote him as saying. In the late 1980s and early 1990s I studied my grading patterns carefully to see whether there was any correlation between the ideological slant of a student’s answer (to the extent any such slant was evident in what the student wrote) and how high a grade I awarded and found that there was none at all. That’s why right-leaning students of mine like Ted Cruz tended to do every bit as well on my blindly graded exams as did more liberal students like Barack Obama. An exam filled with what Anthony Scaramucci told you was ‘left-leaning judicial activism and tons of pablum and liberal shibboleths’ wouldn’t have received a grade as high as an A-, and exams that did a good job explicating an originalist position would’ve received very high grades. More to the point, my exams always emphasized technical mastery of Supreme Court doctrine and left little or no room for ideological posturing.”]

At one time Scaramucci clearly had a good grasp on Con Law. But that was 30 years ago. What about today, I wonder. “What’s the Commerce Clause?,” I ask the former Constitutional law expert. I was thinking I might get hopeless equivocation. After all, it’s been a very long time. I had to look it up myself on Wikipedia. But Scaramucci didn’t need a lifeline. He dove into a lengthy lecture of the Constitutional provision, followed by its impact on national economics, and concluding with a study of Russian versus Western economics. Hmmm, quite a few good points, I’m left thinking. It’s hard to believe the guy needed three tries to pass the bar exam.

Scaramucci’s time at Harvard overlapped with that of Barack Obama. But he was two years older than the would-be President and has no recollection of him. Scaramucci tells me about a fundraiser he attended for Obama. He was about to hand the candidate a big check. But before doing so he asked the future President if he could tell people that the two were tight in law school. “If you double the check we’ll take it right back to Hawaii,” Obama replied. “Like we were in high school together.”

While Scaramucci never practiced a day of law, Harvard taught him plenty of lessons he tells me. Among others, “avoid law suits. In thirty years on Wall Street I’ve never had a law suit.” Law school, Scaramucci explains, also taught him “that there are very smart people on both sides of an argument. . . . I have to understand [the other side] of the argument and I have to really crystalize it in my head so I can either debate it, refine it or change my opinion. That’s what I learned in law school -- that mental flexibility.”

Scaramucci’s roots were on display at Harvard. “I used to tell my buddies in law school, these elites that had these fancy-pants parents: ‘You think you guys in your neighborhood were that much smarter than the kids in my neighborhood? They weren’t. The only difference was, the kids in your neighborhood, the parents ingrained studying, the father was a doctor, he pushed you. And this kid, his father was clamming all day out in Oyster Bay so he was too tired. When he got home he was laying on the couch. So that kid ended up not studying. He’s not stupider than you kid.’”

And his views on education have not changed. “You can’t systematize an equal outcome,” Scaramucci explains. “However, we should be smart enough to help people create equal opportunity. It shouldn’t matter what your skin color is, your sexual preference, your sex, none of that should matter, religion, or your economic upbringing. What should matter is, you’re an American, let’s get you a great education. And if you’re smart you won’t vape, and smoke and drink. You’ll go to work.”

Walking Away From A Million Bucks

Despite a sheepskin from Harvard Law School, Scaramucci experienced some early bumps. In addition to the bar exam failures, his first job, at Goldman Sachs, ended after just a year and a half. It was early 1991 and the first Gulf War had led to an economic downturn. Goldman responded with layoffs. Scaramucci included. But he knew he lacked the skills for the job and it was a terrible fit.

Scaramucci was hired back at Goldman two months later – in a positon that better fit his skill set. Human Resources told him that his re-hiring could be classified as an interdepartmental transfer and he wouldn’t have to tell people that he had been fired. All he had to do was return the $11,000 severance payment. “That’s OK,” Scaramucci replied. “I’d rather tell them I was fired.”

Scaramucci left Goldman in 1996 and started his own hedge fund. It was sold to another company. That company was then sold to Lehman Brothers. But the Lehman culture didn’t suit him. He left in 2004, despite having an annual compensation at the time of $1.1 million. In 2005 he founded SkyBridge Capital.

“I’m Mayhem”

Scaramucci has said that “as soon as you stop acting like a Harvard alumnus, the better off your career will be.” What does he mean?, I ask. “What ends up happening you get this level of self-importance,” he explains. But he sees a much greater downside, to a degree from the fabled law school, than just a change in personality. “The worst thing that can happen to you in your life . . . is that you stop talking risks” he explains. “I went to Harvard. I can’t be perceived as a failure in anything.”

But Scaramucci clearly does not suffer this affliction: “I’m mayhem from the Allstate commercial,” he tells me, in an animated fashion. “I’m coming through the roof and onto the car. And I’m getting up and I’m dusting myself off. What do I care?”

I share with Scaramucci that maybe I’m too risk-averse in my life. He looks me straight in the eye. His face says “listen-up:” “Hey, I got tabloided, boss. Do you know what tabloided is? I’m on the front page with my wife. We’re fighting over our marriage. We’re fighting over Trump. We’re fighting over everything. I’m tabloided. And then the left-wing media roasted me. It was in forty major newspapers around the country and non-stop for five, six, eight days in the American media. I dusted myself off and got back to work.”

Not the least bit surprisingly, Scaramucci’s White House departure was parodied by Saturday Night Live. Bill Hader’s portrayal of the Mooch is hilarious. But does the real Mooch think so? “I thought it was fantastic,” he tells me, without hesitation. “I can take a punch. You want to roast me on Saturday Night Live, I find it funny.”

Scaramucci jokes that he’s going to live to a hundred. “You know why I’m gonna live to a hundred?,” he asks. “I gotta outlive these haters. So I’m taking fish oil and anti-cholesterol medication.”

New Book: Trump – The Blue Collar President

Late last year Scaramucci published “Trump – The Blue Collar President” (Center Street). It’s his fourth literary effort. But the book is misnamed. While it discusses what he see as Trump’s awakening of the plight of the middle class, it is much more the story of Scaramucci – from his hardscrabble upbringing, to Harvard, his failure at Goldman and others and the risks and fears of starting his own businesses.

Scaramucci also chronicles in detail his eleven days in the White House. And he blames nobody but himself for that fateful call to reporter Ryan Lizza at The New Yorker. He says he was “politically naïve to the twentieth power.” Scaramucci says he should have told the reporter that the call was off the record. He thought it was implied, as he and Lizza were two Italian guys whose fathers knew each other from the construction business.

On the subject of the President, Scaramucci tells me that he’s “not here as a Trump apologist.” He calls him “a flawed guy. The tweeting is nonsensical. Don’t pick a fight with the media. Believe in the First Amendment.”

Those who don’t like Donald Trump probably don’t like the Mooch either. His guilt by association will never go away. They are most likely not rushing out to buy his book. But whether you like the President or not, “Trump – The Blue Collar President” is a very enjoyable read. It never gets slow. Scaramucci’s personal story, told with humor and colorful Mooch-language, offers many lessons on life and business. And his brutal honesty, about his time in Washington, is refreshing.

On that, Scaramucci puts it this way: “When my colleagues in finance ask me what it was like working in Washington, D.C., I tell them to imagine the worst, most manically ruthless person they ever worked with in business, Gordon Gekko with a genital rash, the kind of guy who would screw you over, burn your house down, rob you blind if it meant he would get ahead. That person, I tell them, would be an Eagle Scout in Washington, D.C.

SkyBridge Capital: Democratizing Hedge Funds

I have no idea what SkyBridge Capital does. I read the “About” page on the company’s website. I don’t understand a word of it. I tell Scaramucci that I have an account at Vanguard. In other words, keep it simple. He does. And he also sends me home with a copy of his 2012 book “The Little Book of Hedge Funds.”

Now I think I got it. A hedge fund, considered an alternative investment, holds assets that are not necessarily correlated to the equity and bond markets. SkyBridge offers a portfolio of about twenty-four hedge funds. So it’s a so-called fund of funds. By investing with SkyBridge you are investing in several hedge funds.

But here’s the rub with SkyBridge. Hedge funds typically require a very large minimum investment, in the range of $100,000 to $1 million. But not Scaramucci’s. “Because I’m a blue collar kid,” he tells me, “I have democratized the hedge fund industry. I brought the minimums down to $25,000. That allows dentists and doctors and lawyers and mass affluent people to have access to the most famous money managers in the world through my product.”

With that, Scaramucci apologizes and says he has to run. He’s late. There’s an Uber waiting for him. But he has one more thing to tell me before disappearing out the door. He looks at me, smiles and says: “You didn’t think I knew what the Commerce Clause was.”

[Elizabeth Vandenberg, a student at the University of Iowa College of Law, assisted with this article.] |

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Vol. 8 - Issue 2

February 6, 2019

ISO Data Breach Exclusion

And The Scott Baio Bobble Heads

|

|

|

|

|

| |

Over the past few years talk in insurance coverage circles has been cyber, cyber, cyber, especially data breaches. Much of that discussion has been on the drafting, marketing of, and applicability of cyber policies. But ISO’s workhorse CGL policy – CG 00 01 – should not be ignored in this context. Arguments are still made that its coverage, offered for invasion of privacy, applies to a data breach. Indeed, ISO says it does in its August 28, 2013 Circular in conjunction with its filing of data breach exclusions (LI-CU-2013-059/LI-GL-2013-143).

In an attempt to remove such coverage from a CGL policy, and transfer the risk to stand-along cyber policies, ISO introduced a mandatory data breach exclusion. In general, it excludes coverage for “bodily injury,” “property damage,” and “personal advertising injury” “arising out of any access to or disclosure of any person’s or organization’s confidential or personal information, including patents, trade secrets, processing methods, customer lists, financial information, credit card information, health information or any other type of nonpublic information.” The exclusion then goes on to explain that it “applies even if damages are claimed for notification costs, credit monitoring expenses, forensic expenses, public relations expenses or any other loss, cost or expense incurred by you or others arising out of any access to or disclosure of any person’s or organization’s confidential or personal information.”

The applicability of ISO’s new data breach exclusion was before a New Mexico trial court in Wobbler, Inc. v. Land of Enchantment Property & Casualty Company, No. 17-2234 (N.M. Dist. Ct., 13th Judicial Dist., Cibola Cty., Jan 22, 2019).

At issue was coverage for Wobbler, Inc. for a claim arising out of the hacking of its website. Its list of customers and their purchases, within the past 18 months, was made available on the internet. The hacking incident was publicized in the media. The name Wobbler sounded familiar to Pete Clemenza. He had seen a co-worker, Luca Brasi, frequently receive packages from Wobbler. One time Clemenza had asked Brasi what was in the packages and Brasi gave an evasive answer. Clemenza went on line and found Wobbler’s hacked data. He discovered that, over the past year, Brasi had purchased five Scott Baio bobble heads from Wobbler. Clemenza revealed to numerous company employees that Brasi had made these purchases. Brasi was subjected to ridicule.

Brasi filed suit against Wobbler for invasion of privacy. Wobbler, based in New Mexico, sought coverage under its CGL policy issued by Land of Enchantment Property & Casualty Company. LoE disclaimed coverage to Wobbler on the basis of the policy’s data breach exclusion. The insurer saw it as a simple matter – Brasi’s claim against Wobbler was for “personal advertising injury,” specifically, invasion of privacy, arising out of disclosure of Brasi’s confidential or personal information. Wobbler undertook its own defense and settled the claim with Brasi for $65,000.

Wobbler filed an action against Land of Enchantment for recovery of its defense costs and the settlement – around $100,000. The parties filed competing motions for summary judgment. In Wobbler, Inc. v. Land of Enchantment P&C, the New Mexico trial court held that the data breach exclusion did not apply. The court awarded Wobbler $101,512.

It was revealed that Brasi had posted photos of the Scott Baio bobble heads on his Facebook page. Thus, as the court saw it, the information about Brasi’s purchases was not “nonpublic information,” as required to trigger the data breach exclusion. The court rejected Wobbler’s argument that, despite the information about Brasi’s bobble head purchases being on Facebook, it was de facto non-public, as nobody would have had a reason to look for it. In other words, Wobbler argued that it was not until the data breach and subsequent media stories, which gave rise to Clemenza’s web search, that the information about Brasi became public. At the time of the breach its was essentially non-public. But the court disagreed -- not willing to shake its head up and down.

|

That’s my time. I’m Randy Spencer. Contact Randy Spencer at

Randy.Spencer@coverageopinions.info |

|

| |

|

| |

|

|

|

|

Vol. 8 - Issue 2

February 6, 2019

Encore: Randy Spencer’s Open Mic

The Absolutely, Positively Dumbest Class Action -- Eve

|

|

|

|

|

| |

[From the September 7, 2016 Issue of CO.]

Class actions are a funny thing. Not funny ha-ha. But funny in that they serve such divergent purposes. On one hand, virtually every social movement since the 1950s has been augmented through class actions and they have served to protect constitutional rights. This is the case that Professor Arthur Miller made to Maniloff in the last issue of Coverage Opinions (which, I might add, is a useless publication except for the “Randy Spencer’s Open Mic” column).

On the other hand, Miller also acknowledged the well-known knock on class actions, that there have been some “downright silly” ones. Indeed, just a few days ago, a California federal judge dismissed a putative class action against Starbucks seeking damages from the coffee giant on the basis that its cold drinks contain ice, which lessens the amount of beverage in the cup. And don’t forget the class action against Subway because its “foot long” subs measured fewer than twelve inches. That one settled.

These types of consumer class actions get a lot of media attention because of their silliness and opportunity to portray the legal system as broken – especially when they involve a settlement that gives the class members a pittance and the lawyers gobs of money. These are simply irresistible stories for the media.

Well, when it comes to silly consumer class actions, the shark has officially been jumped. On August 19 a putative class action was filed in the Central District of California, against Envelope Corporation of America, alleging that the envelope behemoth is violating a variety of California consumer protection laws by not stating on its packaging that the glue on its envelopes contains no nutritional value. The plaintiff, for himself and on behalf of all others similarly situated, alleges that ECA is obligated to warn consumers that licking an envelope will not satisfy any of the government’s recommended daily nutritional requirements.

The plaintiff concedes in the complaint that envelopes are exempt from the Federal Food, Drug, and Cosmetic Act information panel requirement because envelopes are not a prepared food. [That’s the little box on the package that tells you the calories and fat content of a food and that three potato chips constitutes a serving]. So the complaint takes a different tack, maintaining that consumers could be led to believe that, because envelope glue enters their mouth when licking it, they are obtaining a nutritional benefit. As a result, the complaint warns that consumers may forego eating other foods, on the mistaken belief that the envelope has already satisfied an aspect of their daily nutritional requirements. Plaintiffs seek medical monitoring to be sure that they have not been physically harmed by inadequate nutrition, on account of NEC’s gross negligence by its omissions, as well as a host of damages for violation of various consumer protection laws, and, of course, the accompanying attorney’s fees allowed by these laws.

The case is Phillip Finley, and all others similarly situated v. Envelope Corporation of America, No. 16-cv-1259 (C.D. Calif. Aug. 19, 2016).

Thank goodness the post office switched to sticker stamps a while back. Can you imagine?

|

That’s my time. I’m Randy Spencer. Contact Randy Spencer at

Randy.Spencer@coverageopinions.info |

|

| |

|

| |

|

|

|

|

Vol. 8 - Issue 2

February 6, 2019

Winners Of The Coverage OpinionsSuper Bowl Contest

|

|

|

|

|

|

| |

Well, you probably won’t be surprised to hear that nobody picked 16 as the total points scored in Super Bowl LIII. If your guess was off by 50 or 60 points don’t fret. You are not alone.

Congratulations to the following “winners” of the Coverage Opinions Super Bowl Contest:

Ted McKenna

Annandale, New Jersey

Patriots - 21 points

Andy Miller

Clyde & Co.

San Francisco

Patriots - 27 points

Each of them will be sent a copy of the 4th edition of Insurance Key Issues.

To learn more about Insurance Key Issues visit its website:

http://insurancekeyissues.com

|

| |

|

|

|

| |

|

|

|

| |

|

| |

Vol. 8 - Issue 2

February 6, 2019 |

| |

Show Your Love For Coverage Opinions: Get The New CO License Plate |

| |

|

| |

The number of license plates these days that show the driver’s support for a college or a charity or sports team or some other seemingly obscure organization have reached epic levels. The state of Missouri lists eleven pages of options. And in many cases only a handful of people have them. Like, under 20.

I think a cub scout troop can now get its own license plate. And even your fantasy football league. My mother’s eight-member book club is thinking about getting one. And only three of the woman in it drive.

So maybe it’s time for Coverage Opinions to get in on the action.

If it’s not too much effort and cost maybe I’ll try to get Pennsylvania to issue one for CO. |

| |

|

| |

|

|

|

| |

|

|

|

|

Vol. 8 - Issue 2

February 6, 2019

WSJ: How Old Is AIG?

|

|

|

|

Last week’s Wall Street Journal (the paper’s insurance reporter -- Leslie Scism) had a fascinating front page article about AIG celebrating its 100th anniversary. However, the company’s former chief executive, Hank Greenberg, disputes the company’s math.

AIG makes the claim to being 100 years old by tracing its roots to 1919, when Cornelius Vander Starr began insurance businesses in Shanghai. However, as Mr. Greenberg sees it, AIG dates back only to 1967. That’s when, writes Scism, Mr. Greenberg says he “pulled together various operations that had grown from that original Shanghai company—to take public.”

“Mr. Greenberg says the insurance business he has been expanding since he left AIG—known as Starr Cos.—is the legitimate claimant to the 100th anniversary. Starr Cos., not AIG, is the one which connects to the Shanghai start, he says.”

Mr. Greenberg added: “You think I’m going to sit quietly by and let them take credit for being 100 years old? They’re not, and I know the answer to that because I formed AIG.”

It’s a fascinating story and something that CO readers, the risketeers that we are, will enjoy.

[I had the privilege of interviewing Hank Greenberg (an email Q&A) several years back. Shortly after it was published a package arrived in the mail. Inside was his just published book with a very nice inscription. As an insurance guy, I’ve always cherished it.]

|

|

|

|

|

|

|

| |

Vol. 8 - Issue 2

February 6, 2019 |

| |

Insurance Company Shortens Its Name: Will Save A Lot Of Time

|

| |

|

| |

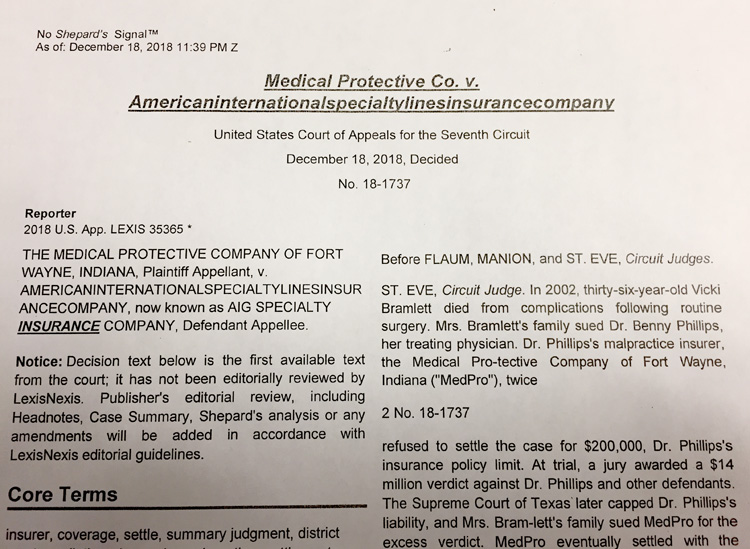

As this recent decision from the Seventh Circuit reveals, American International Specialty Lines Insurance Company has shortened its name. No doubt this was done to save time. When typing its name, employees will no longer have to hit the space key five times. Very wise. |

| |

|

| |

|

|

|

| |

|

|

|

|

Vol. 8 - Issue 2

February 6, 2019

New York’s Disclaimer Rules: Two Courts Demonstrate Their Importance

Guest Authors: Anthony Miscioscia and Timothy Carroll

|

|

|

|

[Tony Miscioscia a partner at White and Williams, LLP and Tim Carroll, an associate, prepared this excellent article as a firm client alert.]

As two recent cases demonstrate, a coverage disclaimer in New York is only as good as its compliance with that state’s various rules for perfecting a disclaimer in connection with a bodily injury claim. Under New York Insurance Law § 3420(d)(2): “[i]f under a liability policy issued or delivered in this state, an insurer shall disclaim liability or deny coverage for death or bodily injury arising out of a motor vehicle accident or any other type of accident occurring within this state, it shall give written notice as soon as is reasonably possible of such disclaimer of liability or denial of coverage to the insured and the injured person or any other claimant.”

The most common mistakes in failing to comply with Section 3420 include failing to issue the disclaimer within a reasonable time, failing to send a copy of the disclaimer to both the insured and the injured person (or other claimant) and failing to state all defenses to coverage that are available to the insurer at the time it issues the disclaimer. But, as two recent New York cases illustrate, there are also other pitfalls to keep in mind when contemplating a disclaimer.

In Dynatec Contracting, Inc. v. Burlington Insurance Company, 2019 N.Y. Misc. LEXIS 187 (N.Y. Sup. Ct. Jan. 7, 2019), for example, an insurer was estopped under Section 3420 from disclaiming coverage based on a policy exclusion because the disclaimer was not issued soon enough after receipt of the claim. There, a contractor sued a subcontractor and the subcontractor’s insurer for coverage as an additional insured under the subcontractor’s general liability policy, in connection with an underlying action seeking damages for bodily injuries sustained in a scaffolding accident. In April 2017—the dates are relevant—the contractor tendered its defense to the subcontractor’s insurer. Thirty days later, in May 2017, the contractor’s insurer disclaimed coverage on several grounds, including that the subcontract requiring that the contractor be named an additional insured on the subcontractor’s policy was not fully executed.

However, three months later, in August 2017, the subcontractor’s insurer sent a supplemental letter disclaiming coverage on the additional basis that an exclusion in the subcontractor’s policy excluded coverage. The contractor argued that the subcontractor’s insurer was estopped, under Section 3420(d)(2), from disclaiming coverage based on that exclusion because notice was not given “as soon as is reasonably possible.” The trial court agreed, concluding that “the basis alleged for the disclaimer was available on the face of the underlying amended complaint.” The court rejected the insurer’s argument that its delay in disclaiming coverage under the exclusion was “due to its desire to conduct further investigations,” since no further investigation was necessary. As a result of the insurer’s failure to comply with Section 3420, the Dynatec court held that the insurer was obligated to defend the contractor as an additional insured in the underlying action.

In County of Niagara v. Liberty Mutual Insurance Company, 2019 U.S. Dist. LEXIS 1898 (W.D.N.Y. Jan. 3, 2019), a coverage disclaimer was upheld because the insurer complied with Section 3420’s disclaimer rules. There, the owner of a window-installation project tendered its defense and indemnity to the general and excess liability insurer of the window-installation contractor, in connection with an underlying action by one of the contractor’s employees seeking damages for bodily injuries he sustained while working on the project. Within one week of receiving the project owner’s tender, the contractor’s insurer disclaimed coverage for the project owner on several grounds, including that certain exclusions in the contractor’s policy applied to the allegations in the worker’s complaint. Having agreed that coverage for the accident was subject to the policy exclusions, the New York federal court moved to “consider[ ] whether the Disclaimer Letter timely and sufficiently disclaimed coverage for the accident” under Section 3420(d).

The project owner in Niagara argued that the contractor’s insurer was estopped from disclaiming coverage because the insurer did not address a copy of the disclaimer to the project owner; it was addressed only to the named insured contractor with a “cc” to the project owner. But, “under relevant New York case law,” the court observed, “a disclaimer letter is effective as against an additional insured so long as the additional insured received a copy of it,” including where it receives “only a carbon copy” of the letter. The project owner also argued for estoppel because the insurer did not reference the project owner’s claim for additional insured coverage; it only referenced “generic” claims made in connection with the underlying action (including the named insured’s claim).

The court disagreed, concluding that “the Disclaimer Letter consistently and repeatedly states coverage is being denied for the ‘above captioned matter’ and the ‘incident,’” which satisfies Section 3420’s notice requirement. The project owner further argued for estoppel because the insurer did not include with the project owner’s copy of the disclaimer a hard copy of the relevant policy exclusions. But the court also rejected that argument, finding the insurer’s full quotation of the exclusion’s language in the disclaimer satisfied Section 3420’s notice requirement.

These two recent cases highlight the importance of complying with N.Y. Ins. Law § 3420’s coverage disclaimer rules—and the danger insurers face in failing to do so. An insurer can, and will, be estopped from disclaiming coverage under even the most cast-iron defense if the disclaimer is not both timely and sufficient under Section 3420.

|

|

|

|

|

|

| |

|

Vol. 8 - Issue 2

February 6, 2019

Washington’s Keodalah Decision Hits Close To Home:

Attempts Made To Hold Insurer’s Outside Counsel Liable For Bad Faith

|

|

|

|

Much has been written about the Washington Court of Appeals’s 2018 decision in Keodalah v. Allstate Insurance Co., which held that an insurance adjuster, employed by an insurer (and not simply the insurer itself), can be liable for bad faith as well as violation of the state’s Consumer Protection Act.

Keodalah is now before the Washington Supreme Court. So its ultimate impact is to be determined.

In late January, Washington Defense Trial Lawyers filed an amicus brief in the case with the Washington high court. WDTL argues that Keodalah should be reversed – but not simply because the decision is incorrect.

Instead WDTL argues that Keodalah opens Pandora’s box. Specifically, if insurance adjusters can be sued for bad faith, then outside counsel for insurers could be next. The strength in WDTL’s argument is that it is not being Chicken Little. To the contrary, WDTL points out in its brief that there have already been at least two cases where outside insurer counsel has been sued for bad faith -- alleging that they were engaged in the business of insurance. [Both filed by the same law firm.]

In Scudder v. GEICO, filed on November 7, 2018 in the Superior Court of Washington, King County, the Scudders alleged that GEICO (and the insurer’s counsel) committed bad faith in the handling of a claim under an auto policy. WDTL states that insurer counsel was retained to represent GEICO and perform an examination under oath. In Sharp v. State Farm, filed on November 13, 2018 in the Superior Court of Washington, King County (and removed to federal court), Sharp likewise alleged that State Farm committed bad faith in its handling of a claim under an auto policy. WDTL states that insurer counsel was retained to represent State Farm with respect to coverage issues. The complaints do not allege what outside counsel may have done that alleged bad faith.

In addition to arguing that, as a matter of law, an insurer’s outside counsel should not be liable for bad faith or a violation of the CPA, WDTL also sets forth a litany of adverse consequences that could flow from permitting outside insurer counsel to be sued for such things.

It’s a slippery slope as WDTL points out. In other words, if you give a mouse a cookie…

[If you are interested in this issue further please send me a note and I’ll send you the WDTL brief.]

|

|

|

|

|

|

|

Vol. 8 - Issue 2

February 6, 2019

The Fab Four Corners: The Most Unique Products-Completed Ops. Case I’ve Ever Seen

|

|

|

|

Northland Casualty Company v. Mulroy, No. 13-232 (D. Mont. Jan. 11, 2019) involves coverage for property damage caused by beetle infestation of logs used to build a log home. With peculiar facts like that, an initial response may be that the decision is of little value beyond log homes. But, in fact, the decision offers an interesting look at whether property damage comes within the products-completed operations hazard. And, based on the court’s analysis, the decision can have applicability to all sorts of claims.

The court described the facts as follows: “Joseph S. Mulroy hired Duane Keim’s company, Northwest Log Homes, LLC, to build a log home near Trego, Montana. Among other responsibilities, Keim was to build and stain the log component of the home. He also partially remodeled a guest home using logs. Keim purchased logs from a log broker, and he did not treat the logs for insects. Several years later, Mulroy noticed signs of an active wood-boring powderpost beetle infestation in both the main home and the remodeled guest home. The infestation caused substantial damage to both structures, and it remains ongoing.”

Mulroy sued Keim. Keim sought coverage from Northland Casualty Company under a commercial general liability policy. Northland provided a defense under a reservation of rights. Mulroy and Keim -- without Northland’s consent -- settled the claim. Keim admitted liability and assigned his rights, under the Northland policy, to Mulroy. Following a damages hearing, the court awarded $208,824.58 in damages for remediation costs and $120,000 for loss of value.

At issue in the coverage action is whether Northland had a duty to indemnify Keim for the damages. Northland argued that, for various reasons, it did not. Of note here, Northland (acknowledging that the property damage and occurrence requirements were met) argued that coverage was precluded by exclusion j(6).

Exclusion j.(6) precludes coverage for “property damage” to “[t]hat particular part of any property that must be restored, repaired or replaced because ‘your work’ was incorrectly performed on it.” Exclusion j(6) does not exclude coverage if the “property damage” falls under the “products-completed operations hazard.” In relevant part, the “products-completed operations hazard”: a. Includes all . . . “property damage” occurring away from premises you own or rent and arising out of “your product” or “your work” except: (1) Products that are still in your physical possession; or (2) Work that has not yet been completed or abandoned . . . .”

Step 1, the court concluded that exclusion j.(6) – without regard to an exception -- applied: “In the underlying action, Mulroy alleged—and the state court found—that Keim was negligent in failing to chemically treat the logs for insects. The use of the untreated logs constitutes Keim’s ‘work,’ which was ‘incorrectly performed,’ causing ‘property damage’ to Mulroy’s home and guest house. Thus, upon a first read, the ‘unambiguous language’ of the policy excludes coverage for remediation of at least a ‘particular part’ of Mulroy’s property unless the PCOH provision applies.”

However, a second step was required. Did the “products-completed operations hazard” exception apply? The court explained that it did: “The applicability of the PCOH provision depends on timing; if the damage occurred after Keim completed its work, then the PCOH provision is in play, and Northland cannot rely on exclusion j(6). Northland argues that the provision does not apply because Mulroy’s property damage occurred when the logs were selected and placed, well before Keim finished the project. Mulroy counters that the property damage did not occur until several years after the home was finished, when he noticed beetle holes throughout the logs. Mulroy argues that although the beetles were present in the logs at the time of construction, they were ‘dormant,’ and that the ‘emergence, spread, and active re-infestation occurred after Northwest’s work was completed.

Here, the PCOH provision encompasses Mulroy’s property damage, and exclusion j(6) is inapplicable. Property damage does not occur until there is ‘physical injury to or loss of use of tangible property.’ (citation omitted) A ‘physical injury’ is ‘a physical and material alteration resulting in a detriment.’ (citation omitted) In this instance, although the beetles were dormant in the logs at the time the home was built, the integrity and appearance of the home did not suffer until the later infestation. The use of untreated logs created the right conditions for the later property damage, but the damage did not occur at the time of construction.”

Ultimately the court concluded that no coverage was owed on account of the “your work” exclusion. However, claims involving latent property damage are not unusual. So, despite it involving beetles, Northland Casualty Company v. Mulroy provides guidance on the treatment of latent property damage vis-à-vis the applicability of the “products-completed operations hazard.”

|

|

|

|

|

|

|

Vol. 8 - Issue 2

February 6, 2019

Policyholder – For Now – Navigates Around Kvaerner For Pennsylvania CD Coverage

Court Applies Indalex To A Faulty Workmanship Claim

|

|

|

|

For a long time policyholders in Pennsylvania have had a rough go at getting coverage for property damage caused by defective construction. The principal hurdle has been Metals Div. of Kvaerner U.S., Inc. v. Commercial Union Ins. Co., 908 A.2d 888 (Pa. 2006), where the state supreme court held that “the definition of ‘accident’ required to establish an ‘occurrence’ under the policies cannot be satisfied by claims based upon faulty workmanship. Such claims simply do not present the degree of fortuity contemplated by the ordinary definition of ‘accident’ or its common judicial construction in this context.”

Then, in the second of a one-two punch, the Pennsylvania Superior Court took Kvaerner a step further in Millers Capital Ins. Co. v. Gambone Bros. Dev. Co., Inc., 941 A.2d 706 (Pa. Super. Ct. 2007), holding that the natural and foreseeable acts of faulty workmanship also “cannot be considered sufficiently fortuitous to constitute an ‘occurrence’ or ‘accident’ for the purposes of an occurrence based CGL policy.”

The combination of Kvaerner and Gambone have led to Pennsylvania decision after decision holding that no coverage was owed, usually to a contractor, for property damage caused by its defective construction.

On January 30, the Eastern District of Pennsylvania held – at the judgment on the pleadings stage – that Kvaerner was not an impediment to an insured’s entitlement to a defense for claims for the defective construction of residences.

At issue in Nautilus Ins. Co. v. 200 Christian Street Partners, Nos. 18-1364, 18-1545 (E.D. Pa. Jan. 30, 2019), was coverage, for a defense, for 200 Christian Street Partners, for suits filed against it for its defective construction of two homes in Philadelphia. Specifically, owners of homes alleged that 200 Christian Partners marketed itself as a seller of luxury homes, yet sold homes that were “riddled with construction defects.”

Nautilus undertook 200 Christian Partners’s defense under commercial general liability policies and the insurer filed actions, seeking declaratory judgments, that it was not obligated to defend the insured.

The decision addresses a number of issues. The crux is this: “Nautilus contends that all of the allegations in the Underlying Complaints stem from issues regarding Defendants’ faulty workmanship. The parties agree [as did the court] that Pennsylvania law does not consider faulty workmanship to be an ‘occurrence’ that is covered under a Commercial General Liability (‘CGL’) policy. However, Defendants and the Owners counter that Pennsylvania law does recognize product-related tort claims, such as product malfunctions, as ‘occurrences,’ and the Underlying Complaints allege such malfunctions.”

In essence, the insureds and owners were arguing that Indalex, Inc. v. National Union, 83 A.3d 418 (Pa. Super. Ct. 2013) applied. In Indalex, in general, the Superior Court distinguished Kaverner [and Gambone] in the context of a “products” case. Specifically, windows and doors were defectively designed or manufactured by the insured and resulted in water leakage that caused physical damage, such as mold and cracked walls, in addition to personal injury. The court held that the issues were framed in terms of a bad product, which could be construed as an active malfunction, and not merely bad workmanship. An active malfunction, the court concluded, is fortuitous enough to constitute an “occurrence.”

However, in general, courts have consistently concluded that Indalex does not apply in cases involving faulty construction. See Hagel v. Falcone, No. 614 EDA 2014, 2014 Pa. Super. Unpub. LEXIS 464 (Pa. Super. Ct. Dec. 23, 2014) (declining to distinguish Kvaerner and Gambone) (“[T]he most critical element in Indalex was that the appellant’s claims were product-liability/tort claims that were based on damages to persons or property, other than the insured’s product. Such claims are absent here, where workmanship is at issue, rather than an active malfunction or product liability, as such. Hence, Indalex cannot carry the day for Appellants.”); Northridge Vill., LP v. Travelers Indem. Co., No. 15-1947, 2017 U.S. Dist. LEXIS 140541 (E.D. Pa. Aug. 31, 2017) (noting that “Indalex did not announce a new majority rule, but instead carved out a discrete scenario where a claim based in products liability could constitute an ‘occurrence’” and that the claims at issue did not “amount to an ‘active malfunction’ in any product, nor do they state a product liability claim”); MMG Ins. Co. v. Floor Assocs., No. 15-4814, 2017 U.S. Dist. LEXIS 124883 (E.D. Pa. Aug. 8, 2017) (“Because this case is about shoddy workmanship, Floor Associate’s reliance on Indalex, Inc. v. National Union Fire Insurance Co., is misplaced.”).

Despite these decisions, declining to apply Indalex to a faulty workmanship case, the court in 200 Christian Partners did so: “Here, although the Owners primarily allege claims for faulty workmanship, they also explicitly bring a claim for negligence, stating broadly that Defendants should be liable for negligently constructing the homes in a manner that presented a danger to the Owners. The Owners also make allegations specific to a product defect theory of negligence, such as that Defendants used faulty materials and that specific materials have caused problems. Moreover, the underlying complaint in Nautilus I alleges physical injury, such as respiratory issues, to in persons the home as a result of the issues with the home.” [More specifically, the complaints alleged, multiple times, that “[t]he Home was not free from ... faulty materials” and detailed specific concerns with certain products, including the windows, which caused water damage and mushrooms inside the home.”]

The court concluded that the underlying complaints “could encompass product-related tort claims.” Thus, the court could not “foreclose the possibility that Defendants used a third party’s product that actively malfunctioned in an ‘occurrence.’ Even though these allegations are far from specific or cohesive, we are required to resolve all doubts in favor of the insured.”

There is a world of difference between the product-related aspect of Indalex and that at issue here. Indeed, several courts have declined to apply Indalex to a faulty workmanship case. Nonetheless, the court held that Nautilus had a duty to defend until it became clear that there was no longer a possibility of a product related tort claim.

|

|

|

|

|

|

|

Vol. 8 - Issue 2

February 6, 2019

Insured Versus Insured Exclusion Does Not Survive Death

|

|

|

|

Gemini Insurance Co. v. 33 East Maintenance, Inc., 17-7393 (D.N.J. Jan. 22, 2019) is a fascinating decision. The court held that a “Named Insured versus Name Insured” exclusion did not apply to a claim seeking damages for the death of a named insured’s employee. I don’t often say here whether I believe a case was rightly or wrongly decided. But this case was seriously wrongly decided.

The case is a little complex and involves various suits and parties. I’ll distill it here to the aspects that are relevant.

Brian Pancoast, an employee of Freehold Cartage, Inc. – that’s important -- died during the course of his employment. He was working on a specialty roll-off tank/container when the hatch closed on him. Dana Pancoast and Brian’s Estate filed a wrongful death and survivorship action against various Freehold parties. Following various procedural comings and goings, the only remaining defendant was FCI Transport.

The Estate and Dana Pancoast entered into a settlement/consent judgment with FCI Transport for $3,750,000. FCI Transport assigned to the Estate and Dana Pancoast all of its rights against Gemini Insurance, under an excess liability policy. [A primary policy tendered its limit of $1,000,000.]

Freehold Cartage, Inc. and FCI Transport were both Named Insureds under the Gemini Policy. Thus, Gemini maintained that, based on the policy’s “Named Insured versus Name Insured” exclusion, it had no obligation to provide coverage for the settlement. The exclusion provided as follows: “This Insurance does not apply to: Any liability, costs or expenses of any Named Insured or its ‘employee’ arising out of, caused or contributed to by any ‘bodily injury’ or ‘property damage’ claimed by any other Named Insured or its ‘employees.’” (emphasis added).

As the court saw it, the exclusion did not apply because, even though Brian Pancoast was an employee of Freehold Cartage, Inc., a Named Insured, he was not the one claiming bodily injury. Rather, it was Mr. Pancoast’s widow and the Estate that were claiming bodily injury.

Gemini argued that the exclusion “applies to the Estate and Dana Pancoast, even though they are not Named Insureds, because there is nothing in the Exclusion that looks to who has brought a claim or . . . even what theory of liability is pled. Instead, it looks whose [sic] injuries the Named Insured is liable for. As such, Gemini contends that because the bodily injury at issue was regarding Brian Pancoast, an employee of a Named Insured, Freehold Cartage, Inc., the Exclusion applies.”

Gemini also argued that “even if the Exclusion looks to who has brought the claim, the claims brought by the Estate and Dana Pancoast are the equivalent of a claim brought by Brian Pancoast because, under New Jersey Law, the Estate stands in the shoes of the decedent. Further, under New Jersey law, the claim and damages asserted by Dana Pancoast do not exist independent of the Estate’s Wrongful Death claim for the bodily injuries and death of [Brian] Pancoast.”

The court did not accept these arguments: “This Exclusion is unambiguous and unequivocal, and undoubtably revolves around who is asserting the claim, not who it initially belonged to or what claim is being asserted. By its plain terms, the Exclusion is expressly limited to claims asserted by a Named Insured or its employees, not an estate or family member.” (emphasis added). The court added that “if Gemini wanted the Exclusion to bar coverage for claims by a Named Insured’s deceased employee’s estate or spouse, it should have drafted it accordingly. Gemini could have, for example, drafted the Exclusion to exclude coverage for liability claimed by or on behalf of a Named Insured or its employees, or claims made by estates or decedent’s widows.” To this point, the court identified other provisions, in the Gemini policy, that purportedly would have supported the interpretation that Gemini sought.

Simply put, it belies common sense for coverage, under a general liability policy, to turn on whether a person, injured by an insured, lives or dies. The claims brought by the widow and Estate are the equivalent of claims brought by Brian Pancoast. The Estate stands in the shoes of Brian Pancoast. The claims of the widow do not exist independent of the Estate’s Wrongful Death claim. But, even more importantly, the court’s focus on the “claimed by” language in the exclusion does not support its decision. The exclusion is clearly tied to whose injuries the Named Insured is liable for. The court impermissibly reads “claimed by” as “who is making a claim.”

|

|

|

|

|

|

|

Vol. 8 - Issue 2

February 6, 2019

Court Addresses Whether A Gunshot Is An Assault Or Battery

|

|

|

|

Capitol Specialty Insurance Company v. Tayworksky LLC is your basic coverage action involving the applicability of an “Assault or Battery” exclusion, in a general liability policy, to a claim involving a injury sustained in a bar. However, it comes with a pretty unique argument in an effort to avoid applicability of the exclusion.

Melissa Tate was injured by a gun shot while at the Monkey Barrel Bar in Charleston, West Virginia. She filed suit against the operators of the bar (Tayworski) alleging that they failed to keep the bar in a safe condition and that her injury was a result thereof. Tayworsky held a commercial general liability policy issued by Capitol Specialty. The insure filed an action seeking a determination that, on account of an “Assault or Battery” exclusion, it had no obligation to defend or indemnify Tayworsky for any claim asserted in Tate’s suit.

After concluding that the policy’s accident requirement had been satisfied, and there was no basis to preclude coverage on account of intentional acts, the court moved to the potential applicability of the “Assault or Battery” exclusion, which provides as follows:

This insurance does not apply to, nor shall we have a duty to defend, any claim or ‘suit’ seeking damages or expenses due to ‘bodily injury,’ . . . arising out of, resulting from, or in connection with any of the following acts or omissions regardless of their sequence or any concurring cause:

a. “Assault or Battery”, whether or not caused or committed by or at the instruction of, or at the direction of or arising out of the negligence of you, any insured, any person or legal entity, or any causes whatsoever;

b. The suppression or prevention of, or the failure to suppress or prevent ‘assault or battery’ by you, any insured, or any person or legal entity;

c. The failure by you, any insured, or any legal entity to provide an environment safe from ‘assault or battery’, including but not limited to the failure to provide adequate security, or the failure to warn of the dangers of the environment which could contribute to ‘assault or battery’ or failure to maintain the premises by you, any insured or any person or legal entity;

The policy defined “assault” as “any threatened harmful or offensive contact between two or more persons, whether or not caused or committed by or at the instruction of, or at the direction of, or arising out of the negligence of you, any insured, any legal entity, or any causes whatsoever, regardless of fault or intent” The policy defined battery as “any actual harmful or offensive contact between two or more persons, whether or not caused or committed by or at the instructions of, or at the direction of, or arising out of the negligence of, you, any insured, any legal entity, or any causes whatsoever, regardless of fault or intent.” (emphasis added).

The insured argued that, as the harmful contact “was made between Ms. Tate and a bullet fired from a gun, no contact was made between two or more persons.” As the court described it, the insured argues “that the exclusion requires not only harmful or offensive contact but also bodily or direct contact.”

The Court rejected the insured’s argument: “While West Virginia courts have not defined or given legal significance to the word ‘contact’ in the context of insurance policies, this Court is of the view that the exclusion applies to harmful or offensive contact—whether achieved through direct or indirect means—between two or more persons. . . . The policy defines an assault and battery in clear, simple terms. Under neither definition must contact between two persons be bodily or direct. Rather, the policy exclusion is concerned with ‘harmful’ and ‘offensive’ contact—contact that is either ‘actual’ or ‘threatened.’ A narrow construction of the term ‘contact’ as Defendants propose would lead to unreasonable and absurd results. Indeed, an interpretation that presumes the policy is intended to provide special protection for injury resulting from a deadly weapon ‘regardless of fault or intent’ but not for injury caused by a physical altercation is illogical. Thus, the Court will not rewrite or construe the policy contrary to its plain language and apparent object and intent.”

|

|

|

|

|

|

| |

|

Vol. 8 - Issue 2

February 6, 2019

Exclusions J(5) And J(6): Appeals Court Provides A Simple Tutorial

|

|

|

|

Decisions addressing the applicability of exclusions j.(5) and j.(6), given their often fact-intensive nature, are sometimes complex. But not MTI, Inc. v. Employers Insurance Company, No-17-6206 (10th Cir. 2019). It is simple and clearly explained. And that’s why the decision could become a go-to one for courts confronting the double Js. [I just made that term up. Maybe it’ll stick.]

At the outset, the facts at issue are straightforward. That helped to keep the decision simple. Western Farmers Electrical Cooperative, which owns cooling towers in Oklahoma, hired MTI to replaced corroded anchor bolts in a tower. MTI employees removed all 64 corroded anchor bolts. However, because the adhesive applicator had not yet arrived, “MTI did not immediately install new anchor bolts. Further, MTI did not provide any temporary support to ensure the stability of the tower. On the night of May 24, extremely high winds struck the tower, causing it to lean and several structural components to break. Due to the extent of the structural damage, removal and replacement of the tower was determined to be the only viable option. Although at least some internal operational equipment was not damaged, this equipment was deemed too dangerous to access and recover.”

Even the procedure is simple: “WFEC demanded MTI pay the cost of removing and replacing the entire tower, which totaled over $1.4 million. MTI filed a claim for coverage with its insurer, Wausau, under the [CGL] Policy. After Wausau declined to provide coverage, MTI directly negotiated a settlement of $350,000 with WFEC. The balance of the tower replacement cost was borne by WFEC’s insurer.” MTI filed a coverage action seeking recoupment of its settlement amount from Wausau.

At issue before the court was the potential applicability of exclusions J(5) and J(6):

j. Damage To Property

“Property damage” to:

. . . .

(5) That particular part of real property on which you or any contractors or subcontractors working directly or indirectly on your behalf are performing operations, if the “property damage” arises out of those operations; or

(6) That particular part of any property that must be restored, repaired or replaced because “your work” was incorrectly performed on it. (emphasis added)

As the court noted, the key to the scope of these exclusions is the meaning of the phrase “that particular part.” The court observed that these exclusions have received inconsistent treatment from courts around the country. It provided several examples on both sides. But inconsistent treatment, the court pointed out, does not mean that the language is necessarily ambiguous.

The court identified two schools of thought nationally on the interpretation of “that particular part” - narrow and broad.

Courts in the narrow camp have “determined the scope of coverage by looking to the ‘distinct component parts’ on which an insured conducts operations. Courts in the broad camp have held that “that particular part” could “apply to those parts of the project directly impacted by the insured party’s work.”

The court saw both ways as being reasonable -- but only one could apply: “Because both readings are permissible, the exclusions are facially ambiguous.” At that point, the outcome is easy to predict: “Because the exclusions are ambiguous, they must be strictly and narrowly construed in a manner favorable to the insured party. . . . In this case, interpreting ‘that particular part’ to refer to the distinct components upon which work is performed best comports with these rules of interpretation.” [Even so, the court acknowledged that it’s a fact intensive and case-by case-issue: “In some instances, a larger unit will properly be considered “the particular part.”]

Applying a narrow interpretation, the court held: “As applied to the facts of this case, we conclude the ‘particular part’ on which MTI was ‘performing operations’ and upon which work ‘was incorrectly performed’ should reasonably be understood as the anchor bolts. Those bolts constitute ‘distinct component parts’ of the tower[.] . . . MTI performed work incorrectly by removing them without promptly replacing them or bracing the structure. We further conclude it is objectively reasonable that MTI would expect coverage for the cost of replacing the entire tower, including all of its operational elements, given the ambiguous language of exclusions j(5) and j(6).”

|

|

|

|

|

|

| |

|

|

Court Holds That Raising Cattle Is Not A Domestic Duty To Create Insured Status

West Bend Mutual Ins. Co. v. Calumet Equity Insurance Company, No. 2018AP435 (Wis. Ct. App. Jan. 17, 2019) addressed coverage, for a rear-end collision, that resulted from cattle in a roadway that had escaped from a farm. At issue in the subsequent coverage action, growing out of the underlying bodily injury claim, was the applicability of a provision, in a liability policy, that created insured status for “persons in the course of performing domestic duties that relate to the ‘insured premises.’” The court held that the fencing of cattle on a farm is not a “domestic duty: “David’s activities on Raymond’s property are not ‘domestic duties’ under the holding in Marnholtz [v. Church Mut. Ins. Co., 815 N.W. 2d 708 (Wis. Ct. App. 2012)] for the inescapable reason that David’s activities are not concerned with the management of a private place of residence. There is no connection between either the operation of a cattle business, or the maintenance of a fence on the premises to corral the cattle, and the management of a household or residence as required by Marnholtz.”

A Poor Squirrel And Efficient Proximate Cause

In City of W. Liberty v. Emplrs Mut. Cas. Co., No. 16-1972 (Iowa Feb. 1, 2019), the Iowa Supreme Court rejected the applicability of the efficient proximate cause rule as a basis to find coverage. The court’s decision was summarized as follows: “In a story that probably would not have been written by Beatrix Potter, a squirrel found its way onto an electrical transformer owned by a municipality, triggering an electrical arc that killed the squirrel and caused substantial damage to the municipality’s property. The municipality sought coverage under its ‘all-risks’ insurance policy. The insurer denied coverage based on the policy’s electrical-currents exclusion, which excludes ‘loss caused by arcing or by electrical currents other than lightning.’ Disagreeing with this reading of the insurance policy, the municipality filed suit. The district court granted summary judgment to the insurer and the court of appeals affirmed. On further review, we too affirm the district court. We find that the loss was indeed ‘caused by arcing.’ Therefore, it is excluded even though something else (i.e., the squirrel) triggered the arcing. This is not a situation where two independent causes, one covered and one excluded, may have contributed to the loss.”

|

| |

|

|

|

| |

| |

|

|

|

|

|

|

|

|

|