|

|

|

|

|

| |

|

Vol. 8 - Issue 9

November 6, 2019

|

|

|

|

|

|

| |

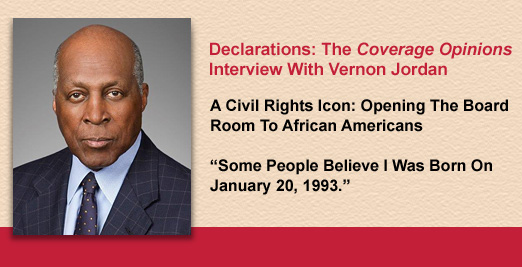

Vernon Jordan described the civil rights movement to me in terms of a hotel stay.

The 1950s and 1960s, he said, were about “defining rights—the right to check-in.” The 1970s were about having the means to check-out. To check-out, to be able to afford the bill, he explained, “You needed to have a job and get paid a fair salary.”

Early in his career as a civil rights lawyer, Jordan focused on checking- in. He worked to secure such things as voting rights for African Americans and desegregation in education.

But his greatest impact would be felt in the chapter of the civil rights story that gets less attention—checking out. As head of the National Urban League during the decade of the 1970s, Jordan’s focus was on achieving economic rights for African Americans. |

| |

|

| |

The civil rights movement is often thought of in terms of its major milestones, such as this year’s 65th anniversary of the U.S. Supreme Court’s decision in Brown v. Board of Education. But Jordan had the foresight to understand that it wasn’t enough for African Americans to have equal opportunity in the classroom. It was also needed in the job market.

Over the course of an hour, in his office at Akin Gump Strauss Hauer & Feld on K Street in Washington, D.C., Jordan, 84, recounted his career as a civil rights lawyer and later advocate pushing corporations to open their doors to African Americans. The lawyer, sometimes called the most-connected person in America, also shared, with a laugh, how you know that you are rainmaker.

Jordan’s work in the civil rights movement nearly cost him his life. In 1980, a white supremacist using a deer rifle shot him as he entered a hotel in Fort Wayne, Indiana. The bullet’s explosion left a hole in his back that could fit a fist.

Jordan’s role in civil rights was significant enough to warrant an assassination attempt. Yet, he noted with amusement, that this comes as news to some. As a close friend and adviser to President Bill Clinton, he received much attention in l’affair Lewinsky, after assisting the former intern with finding a lawyer and getting a job. “Some people believe I was born on January 20, 1993 [the day Clinton took office],” he chuckled.

Jordan, who splits his time between Akin Gump in the nation’s capital and Manhattan, serving as senior managing partner at financial advisory firm Lazard, was born into much different surroundings. He grew up in Atlanta, where living through segregation would dictate his career path.

As a teen he helped his mother in her catering business, which included serving dinner at meetings of The Lawyer’s Club of Atlanta. Jordan liked what he saw in the fellowship and camaraderie and decided he wanted to be part of something like that. But he also listened to the speeches “and I know I didn’t like what I heard when they were talking,” he said. “There was nothing that they were saying that had anything to do with my community or me. It was all in the interest of the continued segregated society.”

It was here that Jordan made the decision to pursue a career as a lawyer. The journey began at DePauw University in Indiana, where he was the only African American in his class.

From the Hoosier State, Jordan made his way to Howard University School of Law in Washington. After joking that the historically black school was a boon to his dating life, he recalled the nation’s leading civil rights lawyers coming to prepare for Supreme Court oral arguments. “To see Bob Carter [general counsel of the NAACP] making his argument, and to see all of these distinguished counsel prepping him, by asking tough questions, was really inspiring.”

Jordan graduated in 1960 and went to work as a law clerk, for a one-man firm, earning $35 a week. Needing to augment his salary, he worked for his mother at night, sometimes serving dinner to lawyers whom he had seen in the courthouse earlier in the day.

The would-be lawyer worked on the team that secured a federal court order mandating that the University of Georgia admit its first two African American students. An iconic picture from the civil rights movement shows the 6-foot-4-inch Jordan escorting his client, Charlayne Hunter, through an angry mob of segregationists as he took her to register for classes.

Jordan would fail the Georgia bar exam. He told me he believes he never had a chance. Georgia’s attorney general, displeased that Jordan was serving subpoenas on state officials in the University of Georgia case, told him that he needed to be taught a lesson. “You shouldn’t have to worry about passing the bar,” the state’s top lawyer said to him, “because it’s not going to happen.” Concerned that he was a marked man, he took the exam in Arkansas and waived into Georgia.

Jordan next turned his attention to organizations that worked to achieve rights for African Americans, holding positions at the NAACP, Southern Regional Council and United Negro College Fund, where he served as president.

In 1971 Jordan took over as president and CEO of the National Urban League. He knew exactly what he wanted to achieve. In his first speech at the Urban League’s annual Equal Opportunity Day Dinner he told the 60 CEOs on the dais and 2,000 in attendance that “it’s not enough for you to come to this dinner. We want to come to your board rooms.’”

His speech resonated. Not long after, invitations to serve on corporate boards came in. Jordan would go on to serve on about 20, including Xerox, American Express, Bankers Trust and J.C. Penny.

But the man of many boards knew that African Americans were generally unaffected by the fact that a few African Americans were becoming corporate directors. His objective was to have an impact on the white corporate directors. He said: “Having a black presence in the boardroom was, quite simply, an education for them. Many of those men had never in their lives come into any serious contact with black people, other than the ones who cleaned their houses.”

Jordan also observed that there was no way to finish the civil rights movement without changing the assumption of what qualifies as “merit” to get a job. It could no longer be “those experiences possessed by a narrow class of white men, which automatically threw almost everyone outside the magic circle into the category of the presumptively unqualified.”

Jordan left the Urban League after a decade at the helm and joined Akin Gump. How did law firms compare to corporations in integration? “The companies were ahead of the law firms.” The reason, he told me, was because “they don’t have shareholders, and they’re not in the public. There was not much pressure on law firms. They didn’t have annual meetings.”

Jordan didn’t spare his own firm criticism for its integration efforts. For several years he made an annual trip to Dallas to speak to the firm’s summer associates. But then he stopped when the firm hired more African Americans for the summer program. What happened? “They found some black associates,” he said.

Jordan didn’t pretend that his job at Akin Gump was about anything other than to make it rain. “There were a lot of smart lawyers here, who knew the law, but they didn’t have anybody to tell it to,” he observed. “I knew the GC here and I knew the GC there.”

He recounted a time from his early days at Akin Gump. He had gone to the firm’s law library to look something up. Firm founder Robert Strauss got wind of it and summoned him to his office. Jordan, with a hearty laugh, recalled the reminder that Strauss told him: “We didn’t bring you here to go to the library.”

With a career spent at the highest heights of the civil rights, legal, financial, corporate and political arenas, Jordan is often referred to as one of the most connected people in America. How does he respond to that? “I don’t,” he told me. “There are some things you just leave alone.” But, he acknowledged, “I pretty much get my phone calls returned.”

It was at The Lawyer’s Club of Atlanta that Jordan made the decision to pursue a career as a lawyer. But his time there as a teenager wasn’t to be his last. In 1974 he was invited to speak to the club’s members.

He told the gathering that, having served many of these dinners himself, he’d made an observation: “The view from the podium is much better than the view from the kitchen.”

|

|

|

|

Vol. 8 - Issue 9

November 6, 2019

9 Year Old Sues Neighbor For Halloween Insult

|

|

|

|

|

| |

I’ve been holding this gem from this summer until Halloween.

On Halloween night in 2017, Timmy Murphy, and three friends, knocked on Oscar Rogers’ door, in Binghamton, New York, with candy on their minds. Mr. Rogers was known as the neighborhood grouch. He was a get-off-my-lawn kind of guy. The kind of person who might give loose candy corn to trick or treaters.

As Oscar was putting one Hershey’s Kiss in each of the kids’ bags, he asked Timmy what he was dressed as. Timmy said a Power Ranger. Mr. Rogers replied that Timmy was the third Power Ranger he’d seen that night -- and Timmy’s costume was the worst of all three. Timmy broke out in tears.

At school the next day, word got out about the Power Ranger incident and Timmy was ridiculed unmercifully, both for having a bad costume and crying. After two weeks of Timmy crying in bed every night about what had happened, Timmy’s father had enough. He had always disliked Mr. Rogers and decided that it was time to teach the cranky old man a lesson. That came in Rogers’ mail box in the form of a document titled Brad Murphy, as parent and guardian of Timothy Murphy, a minor v. Oscar Rogers, No. 4213/17 (Broome Cty. Sup. Ct.).

Brad Murphy alleged that Mr. Rogers slandered Timmy by saying that his Power Ranger costume was the worst he’d seen that night. Mr. Rogers did not take kindly to the lawsuit. He answered and filed a counter-claim against Timmy, alleging that Timmy had trespassed on Mr. Rogers’ property when he came to the door.

Murphy and Rogers both tendered the claims to their homeowner’s insurers. Murphy’s insurer disclaimed coverage for the counter claim as the trespassing claim did not seek damages for “bodily injury,” “property damage” or “personal injury.” Mr. Rogers’ insurer undertook his defense on the basis that the claim for slander triggered coverage for “personal injury.”

The parties filed motions for summary judgment. The court dismissed Mr. Rogers’ trespassing counter claim on the basis that, as it was Halloween, and Rogers’ was giving out candy, even if just a single Hershey’s Kiss, Timmy had implied permission to be on his property. The court dismissed Murphy’s claim on the basis that, while Rogers’ comment was insensitive and boorish, as the court noted, it did not qualify as actionable slander. It was simply Mr. Rogers’ opinion.

The court also called Mr. Rogers’ trespassing claim sufficiently baseless to be worthy of sanctions. However, it declined to order them, given how little effort Murphy’s counsel needed to address it. The court added: “Ordering sanctions against Mr. Rogers and his counsel would only prolong this litigation. The court is not inclined to do anything that could delay the ending of this insanity.”

I got Brad Murphy on the phone on Friday to see how Timmy’s Halloween was. Good news. Timmy is doing fine. And it turns out that it was a positive experience after all. Timmy now wants to be a lawyer. He says he wants to help other kids who are mistreated by “meanies.” In fact, Timmy dressed as a lawyer for Halloween this year, donning a coat and tie and having people put candy in a briefcase. Did he and his friends go to Mr. Rogers’ door? I asked. Yes they did. Mr. Rogers gave each of them loose candy corns.

|

That’s my time. I’m Randy Spencer. Contact Randy Spencer at

Randy.Spencer@coverageopinions.info |

|

| |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Vol. 8 - Issue 8

September 25, 2019

Encore: Randy Spencer’s Open Mic

Thanksgiving And Insurance Coverage: They Go Together Like Peas And Carrots

|

|

|

|

|

|

| |

|

| |

You would think that Thanksgiving is one of a few days a year when insurance coverage could just take a break. A day when insurance policies and claims could just sit down on the sofa and drift into a deep turkey-induced nap. But insurance coverage gets no rest – even on one of the most restful and lazy days of the year. Consider the amount of coverage litigation over the years involving Thanksgiving and its many symbols. These are all real cases. I promise.

Capel v. Plymouth Rock Assurance Corp., 62 A.3d 582 (Conn. Ct. App. Apr. 2, 2013)

Jenkins v. Mayflower Insurance Exchange, 380 P.2d 145 (Ariz. 1963)

Hodgate v. Pilgrim Insurance Company, 2013 WL 812178 (Conn. Super. Ct. Feb. 1, 2013)

Puritan Insurance Co. v. County of Wayne, 536 N.W.2d 777 (Mich. 1995)

Duryee v. Pie Mutual Insurance Co., 1998 WL 832180 (Ohio Ct. App. Dec. 1, 1998)

American Traditions Ins. Co. v. Whirlpool Corp., 2013 WL 4648476 (M.D.Fla. Aug. 29, 2013)

Thanksgiving Home, Inc. v. U.S. Distributing, Inc. v. St. Paul Travelers Companies, 2006 WL 2726139 (N.D.N.Y. Dec. 15, 2006)

Farmers Mutual Hail Insurance Co. v. Fox Turkey Farms, Inc., 301 F.2d 697 (8th Cir. 1962)

State Insurance Fund v. David A. Gobble, 755 P.2d 653 (Ok. 1988)

Corn v. Farmers Insurance Co., 2013 WL 5946942 (Ark. Nov. 7, 2013)

Irwin Potato Farms v. Mutual Service Casualty Ins., 2003 WL 21419427 (Mich. Ct. App. June 19, 2003)

Essex Insurance Co. v. The Great Pumpkin, LLC, 2008 WL 550038 (D.S.C. Feb. 26, 2008)

MISR Insurance Co. v. El-Yam Bulk Carriers, 80 F.R.D. 438 (1978)

Hartford Insurance Co. v. Ocean Spray Cranberries, 1999 WL 529302 (E.D. Pa. July 23, 1999)

Food Parade, Inc. v. Liberty Mutual Fire Insurance Co., 968 A.2d 724 (N.J. Sup. Ct. App. Div. 2009)

Thursday A. Booker v. Classified Insurance Corp., 568 N.W.2d 320 (Wisc. Ct. App. 1997)

John Smith v. Lexington Insurance Co., 2007 WL 4374229 (E.D. La. Dec. 13, 2007)

New World Frontier, Inc. v. Mount Vernon Fire Insurance Co., 676 N.Y.S.2d 648 (App. Div. 1998)

Mom’s Old Fashioned Gravy v. USF&G, 784 P.2d 936 (Mont. 1989)

National Farmers Union Ins. Companies v. Crow Tribe of Indians of Montana, 560 F.Supp. 213 (D. Mont. 1983)

|

That’s my time. I’m Randy Spencer. Contact Randy Spencer at

Randy.Spencer@coverageopinions.info |

|

| |

|

| |

|

|

|

|

Vol. 8 - Issue 9

November 6, 2019

|

|

|

|

| |

I am excited to report that this issue marks the 7th Anniversary of Coverage Opinions. In traditional terms, that’s the copper anniversary. On the modern list, 7th is the desk set anniversary. I swear I’m not making that up. The desk set anniversary. Check it out. If you are thinking about a gift, I could use a new kettle, as well as some new toilet pipes. Either one is fine. I don’t need a desk set, but thanks anyway.

Of course, there could be no seven-year anniversary to mark if it were not for you – the dear Coverage Opinions reader. I can’t thank CO readers enough for taking the time to do so, despite having such busy schedules and being inundated with other newsletters, and the like, competing for their time.

I also appreciate all of the reader email that I receive – mostly positive, but sometimes taking me to task for something I said or didn’t say -- and that’s fine too. I am also lucky for the friendships that I have made with CO readers who reached out about something they saw. Drop me a note. I’ll respond. I’ll be happy to do so.

Please accept my sincere appreciation for enabling me to send a Coverage Opinions seven-year anniversary announcement.

Comments, questions, criticism, hate mail, how’s my driving, ideas for making Coverage Opinions better -- I’m all ears. Please write to me at maniloff@coverageopinions.info.

|

|

| |

|

|

|

|

Vol. 8 - Issue 9

November 6, 2019

Finally: Insurance Key Issues – Half Price Sale!

|

|

|

| |

|

| |

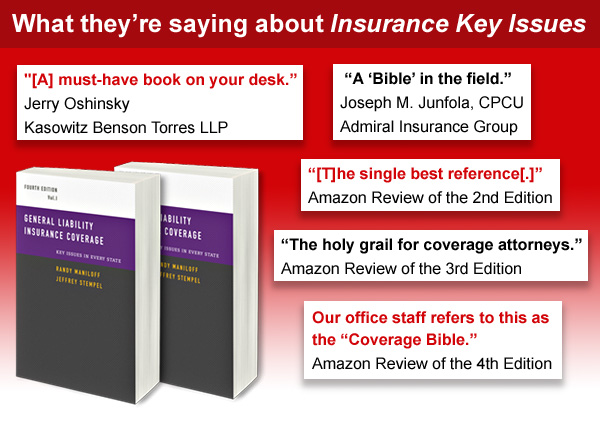

At last, General Liability Insurance Coverage – Key Issues In Every State is on sale. Half price! It took forever for it to go to 50% off, as sales have been humming along at full price. For those of you waiting for the big Insurance Key Issues door buster, here it is! Now’s your chance to see what all of the Key Issues hubbub is about. Or, for those of you who already have a copy, get one for the car.

More about Insurance Key Issues and links to purchase on Amazon are here.

[The price listed on Amazon has been reduced by 50%.]

http://insurancekeyissues.com

|

|

| |

|

|

|

|

Vol. 8 - Issue 9

November 6, 2019

Insurance Haiku Contest

Win An Autographed John Grisham Book

|

|

|

| |

|

| |

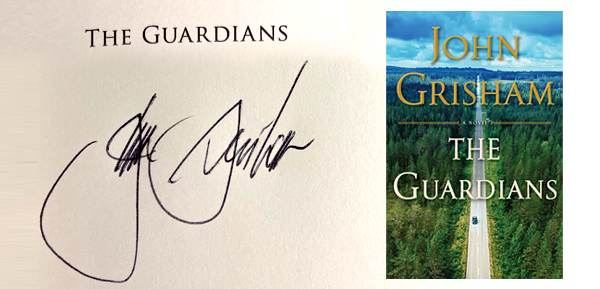

It’s time for another Insurance Haiku Contest!

What an amazing prize for the winner - an autographed copy of “The Guardians,” John Grisham’s just-released legal thriller that is currently #1 on The New York Times best seller list for fiction.

I interviewed John a couple of weeks back about his new book. And he was kind enough sign a copy of “The Guardians” for a CO contest! Signed Grisham books are not common as he has done just one book tour in the past 25 years!

“The Guardians” is fantastic! 75% of the Amazon reviews are 5 stars. It is a classic Grisham thriller. A burned out public defender travels the country seeking to get the wrongly convicted exonerated. Of course, lots of twists and turns along the way.

The Insurance Haiku Contest is a strange thing. It takes the most effort to enter compared to other CO contests. Yet I get the most entries. That tells me one thing. CO readers want to be challenged. Caption contest? Phooey. Insurance license plates? Pleeze. Juvenile. We want haikus. Make us have to work!

Second prize is a copy of Insurance Key Issues. Any honorable mentions will get an amazing Coverage Opinions pen. I found a few extras lying around.

So send in your haiku(s) (using the 5-7-5 format) that have something to do with insurance coverage.

If your response to the word Haiku is to say Gesundheit, do not worry. Just look it up and in minutes you’ll know all you need to get started. Trust me. The best part about Haiku is that you can’t tell the difference between the work of a great master or a 6 year old.

Enter as many times as you’d like. Deadline: November 15. No purchase necessary. Coverage Opinions employees are not eligible. Void where prohibited.

Some past wining insurance haikus:

The insured did what?

Intentional, on purpose!

Not an occurrence

Oh my policy

All I do not understand

But still it will rule

What, no insurance?

That is quite impossible

Premium was paid.

Coverage question

Exclusions limitations

Reservation rights

|

|

| |

|

|

|

|

Vol. 8 - Issue 9

November 6, 2019

The World’s Largest Insurance Policy Provision

|

|

|

| |

Regular Coverage Opinions readers know that I have a fascination with world’s largest objects – those quirky roadside attractions that often serve to draw tourists to small towns across America. There’s the world’s largest ball of twine in Cawker, Kansas, the 55 foot Jolly Green Giant statue in Earth Blue, Minnesota, visitors to East Glacier, Montana can come face-to-face with the world’s largest purple spoon. Known as “Big Martha,” the utensil clocks in at 25 feet. And who among up doesn’t have on their bucket list a trip to Collinsville, Illinois to see the nearly 70 foot world’s largest catsup bottle.

Given my wonderment for world’s largest objects, I must make a trip to an amusement park in Coffs Harbour, New South Wales, Australia, to see the world’s largest banana. It has even been put on an Australia postage stamp. I guess there are only so many kangaroo and koala stamps they can put out.

But the real draw is that it is a twofer -- and an insurance one at that. Of course the world’s largest banana would have the world’s largest banana peel. Thanks to a clever risk manager at the amusement park, the behemoth banana is now accompanied by the world’s largest insurance policy provision.

|

| |

|

|

|

| |

|

|

|

Vol. 8 - Issue 9

November 6, 2019

Delaware Supreme Court Issues Significant D&O Decision

A To-Be Top 10 Case of 2019

|

|

|

| |

Just as this issue of Coverage Opinions was wrapping up, the Delaware Supreme Court handed down its decision in In re: Verizon Insurance Coverage Appeals, No. 558 (Del. Oct. 31, 2019). By the way, how does a court hand down an opinion involving a phone company? It tells the president of the company to be home between 10 and 4 and the clerk will drop it off.

The decision is of significant importance for companies seeking coverage under D&O policies. However, for reasons of timing surrounding the production of this issue, I am not able to address it in detail here and why it is so significant. However, the decision -- given its many implications, and coming from the Delaware Supreme Court on a corporate-related issue -- will definitely be included as one of the “Top 10 Coverage Cases of the Year” in my 19th annual review. Since that’s right around the corner I’ll save it for then.

In general, in the Verizon decision, the high court of the first state defined the term “securities claim” for purposes of coverage. Hanging on the court’s definition was $48 million in defense costs for which Verizon was seeking recovery. Verizon had been sued by a bankruptcy trustee, on behalf of creditors of a bankrupt public company, that had been a Verizon spin-off. It was alleged that Verizon saddled the spun-off company with excessive debt.

For Verizon to be covered for its defense costs, under certain Executive and Organizational Liability policies, the trustee’s claim needed to be a “securities claim,” defined under the policies as a “Claim” against an “Insured Person” “[a]lleging a violation of any federal, state, local or foreign regulation, rule or statute regulating securities (including, but not limited to, the purchase or sale or offer or solicitation of an offer to purchase or sell securities).”

The competing positions were as follows:

“The Insurers claim that the trustee in the U.S. Bank complaint did not raise a violation of any ‘regulation, rule or statute regulating securities’ because the words ‘regulating securities’ limits coverage to specific securities activities, as opposed to matters of general applicability. . . . As the Insurers argue, under the Superior Court’s interpretation, ‘regulations, rules or statutes’ would encompass a variety of non-security related claims.”

“Verizon argues that the plain language of the Securities Claim definition includes claims alleging a violation of ‘any . . . regulation, rule or statute regulating securities (including but not limited to, the purchase or sale . . . [of] securities.’ According to Verizon, the use of the word ‘any’ shows the parties did not intend to exclude common law ‘rules’ or claims that do not ‘specifically’ or ‘principally’ regulate securities.”

Following pages and pages, and more pages, of analysis, the court held that the trustee’s suit did not involve a “securities claim.” Thus, Verizon could not recover its defense costs.

Verizon will be fine. $48 million is what my monthly wireless bill from them feels like.

Again, more about In re: Verizon Insurance Coverage Appeals in the annual Top 10 Coverage-palooza.

|

|

| |

|

|

|

Vol. 8 - Issue 9

November 6, 2019

A Judicial Rarity: Two Appeals Courts Conclude That Exclusions Make Coverage Illusory

|

|

|

| |

It is not unusual for a policyholder, denied coverage, to argue that it never had a chance as the policy is illusory. This usually happens when the claim at issue involves a risk that is fundamental to the insured’s business. As the insured sees it, if the policy does not provide coverage for something at the heart of why the insured needs the policy, that it provides no coverage at all. Hence, it is illusory. These arguments are routinely rejected by courts on the basis that, while the policy may not provide coverage for an important risk, it provides coverage for other potential hazards. So, since it provides some coverage, it is not illusory.

However, two appeals courts, in the past six weeks, have concluded that policies were illusory.

First up was Crum & Forster Specialty Ins. Co. v. DVO, Inc., No. 18-2571 (7th Cir. Sept. 23, 2019). At issue was coverage for DVO, which had entered into a contract with WTE, to design and build an anaerobic digester for WTE. Don’t know what that is? Silly you. It is used to generate electricity, from cow manure, which would then be sold to the electric power utility. “WTE sued DVO for breach of contract, alleging that DVO failed to fulfill its design duties, responsibilities, and obligations under the contract in that it did not properly design substantial portions of the structural, mechanical, and operational systems of the anaerobic digester, resulting in substantial damages to WTE. It sought over $2 million in damages and fees.” The case made it trial. The court found in favor of WTE and ordered DVO to pay over $65,000 in damages and $198,000 in attorney’s fees.

The issue before the court was the availability of coverage, for DVO, under a professional liability policy issued by Crum & Forster. All agreed that the insuring agreement – the wrongful act and professional services requirements -- had been satisfied.

The dispute was over the applicability of the breach of contract exclusion:

This Policy does not apply to “damages”, “defense expenses”, “cleanup costs”, or any loss, cost or expense, or any “claim” or “suit”:

Based upon or arising out of:

a. breach of contract, whether express or oral, nor any “claim” for breach of an implied in law or an implied in fact contracts [sic], regardless of whether “bodily injury”, “property damage”, “personal and advertising injury” or a “wrongful act” is alleged.

All agreed that the exclusion applied on its face. But was it so broad as to make the policy illusory? This was the issue before the Seventh Circuit. If so, the court’s task is to reform the policy to meet the insured’s reasonable expectations.

The trial court said that the policy was not illusory since, despite the contract exclusion, the policy still provided coverage for other risks: “[A]lthough coverage for professional malpractice would effectively fall within that exclusion as to claims alleged by the party to the contract, third parties could still bring tort claims against DVO that would not fall within the exclusion and would trigger the duty to defend in the E&O provision of the policy. The district court reasoned that as a contractor, designer, engineer and builder, DVO has a duty to use reasonable care in carrying out its contractual obligation so as to avoid injury or damage to the person or property of third parties, even though they have no contractual relationship with DVO.”

But the Seventh Circuit saw it much differently, given that the contract exclusion was broad enough to include even any third-party claims: “[T]hat analysis [the district court’s] cannot support the court’s conclusion. If more narrow language was used, the district court’s determination that third-party liability would still be covered might have merit. But the language in the exclusion at issue here is extremely broad. It includes claims ‘based upon or arising out of’ the contract, thus including a class of claims more expansive than those based upon the contract. Wisconsin courts have made clear that the ‘arising out of’ language is broadly construed.”

The court held that, based on the breach of contract exclusion, the C&F policy was illusory and the remedy is as follows: “[W]hen a policy’s purported coverage is illusory, the policy may be reformed to meet an insured’s reasonable expectation of coverage. Therefore, the focus now is not on the hypothetical third-party actions, but on the reasonable expectation of coverage of the insured in securing the policy. There is, after all, no reason to believe that DVO in purchasing Errors and Omissions coverage to provide insurance against professional malpractice claims had a reasonable expectation that it was obtaining insurance only for claims of professional malpractice brought by third parties.”

The trial court’s task was to reform it: “But we need not determine precisely what reformation is appropriate here. DVO did not file a cross-motion for summary judgment. The district court on remand may consider DVO’s reasonable expectations in securing the coverage, and can reform the contract so as to give effect to that expectation. The focus, however, must be on that reasonable expectation, which was upended by the breach of contract exclusion that rendered it illusory. The availability of third-party claims is irrelevant unless it is determined to be a part of DVO’s reasonable expectation of coverage.”

Illusory Coverage Case 2

Then last week the Arizona Court of Appeals issued its decision in Starr Surplus Lines Ins. Co. v. Star Roofing, No. 18-0641 (Oct. 31, 2019). At issue was coverage for Star Roofing, which had performed roofing work on a commercial building in Tempe. Maria Delarosa, an employee of a tenant in the building, suffered a fracture of her right forearm and other bodily injury when she allegedly fell and passed out in the building’s parking lot. Delarosa alleged that her injuries were the result of being overcome by breathing the fumes released from Star Roofing’s work.

Starr Surplus defended Star Roofing under a reservation of rights, asserting the pollution exclusion as a basis to deny coverage. Starr Surplus filed a coverage action, seeking a determination that the pollution exclusion barred coverage.

The trial court found in favor of Star Roofing, concluding that the pollution exclusion was limited to “traditional environmental pollution.” The appeals court decision is really long and has oodles of issues. Importantly here, the court agreed that the claim at issue did not involve traditional environmental pollution.

But then the court went further and addressed illusory coverage, given the nature of Starr Roofing’s operations: “Further, the transaction as a whole--the insuring of a roofing business--calls into question the advisability of a broader application of the pollution exclusion than would arise in ‘traditional environmental pollution-related claims.’ In the present case, Starr Surplus’ own underwriting activities made it fully aware of Star Roofing’s work, and the risk inherent in the installation of a roof was contemplated by the Starr Policy. This was the very risk complained about in the Delarosa action, and the scope of interpretation requested by Starr Surplus would result in illusory coverage for the ordinary commercial business activities of the insured, a result not contemplated by either party to the insurance contract.”

Needless to say, these decisions open a wider door to what is considered illusory coverage.

|

|

| |

|

|

|

Vol. 8 - Issue 9

November 6, 2019

An Insurer Rarity: One Insurer Sues Another For Bad Faith (It Wins – Be Careful What You Wish For)

|

|

|

| |

I read a lot of coverage decisions. And I can’t recall seeing one where one insurer sues another insurer for bad faith. Sure, there are lots of insurer vs. insurer suits for contribution, when one insurer believes that another insurer owes coverage and skated. But to include bad faith counts is unusual. There must have been some bad blood between these guys.

Well, the insurer got its wish. It won. And now it may have saddled itself with an obligation to undertake a duty to defend-coverage investigation concerning an issue that comes up with regularity.

The facts that gave rise to this clash amongst insurers, in Seneca Specialty Ins. Co. v. DB Ins. Co., No. 18-1163 (C.D. Calif. Sept. 9, 2019) are as follows:

CW Piedmont, LLC owned and operated an apartment building in Palmdale, California. On May 1, 2017, 38 current and former tenants sued Piedmont alleging that the building was kept in an uninhabitable condition.

DB Insurance Co. was Piedmont’s liability insurer from May 6, 2014 through May 6, 2017 (three consecutive one-year policies). Seneca Insurance insured Piedmont from May 6, 2017 through May 6, 2018.

Seneca defended Piedmont, but noted, rightly so, that its policy only applied to damages sustained by tenants after the Seneca policy became effective. However, DB refused to defend Piedmont, stating that, to the extent the tenants alleged “bodily injury” or “property damage,” their claims weren’t caused by an “occurrence.” No doubt Seneca could have said the same but it didn’t.

Both Seneca and Piedmont tried to get DB to participate in Piedmont’s defense. No go. The action was eventually settled at mediation for $218,050. DB participated in the mediation via telephone and paid nothing. Seneca obtained an assignment of any and all claims Piedmont might have against DB regarding the action.

Seneca filed suit against DB, asserting the following claims against DB, both on its own behalf and on behalf of Piedmont: “(1) equitable contribution for the defense and indemnity of the Current Tenants; (2) breach of contract; (3) equitable subrogation for defense and indemnity of the Departed Tenants; (4) alternatively, equitable contribution for defense and indemnity of the Departed Tenants; (5) bad faith refusal to defend and indemnify claims by the Current Tenants; and (6) bad faith refusal to defend and indemnify claims by the Departed Tenants.”

The contribution and subrogation claims are what you would expect to see in a case like this, when one insurer pays a claim and another says n-o. But Secena raised the stakes and included claims for bad faith. Insurer vs. insurer is the Cain and Abel of coverage cases.

DB moved for summary judgment. On the bad faith claims – which are the only ones I’ll address here -- DB argued that, even if its initial coverage position was erroneous, it was not in bad faith, as it was based on a genuine dispute regarding coverage.

On one hand, the court agreed with DB, noting that, “under California law, a bad faith claim can be dismissed on summary judgment if the defendant can show that there was a genuine dispute as to coverage[.] Stated differently, [t]he mistaken [or erroneous] withholding of policy benefits, if reasonable or if based on a legitimate dispute as to the insurer’s liability under California law, does not expose the insurer to bad faith liability.”

However, the court was not willing to make a decision by simply concluding that there was no genuine dispute as to coverage.

Recall that DB refused to defend Piedmont on the basis that, to the extent the tenants alleged “bodily injury” or “property damage,” their claims weren’t caused by an “occurrence.”

The court was none too pleased with DB’s decision, based solely on the complaint, that there was no “occurrence.” The court had these harsh words for DB: “

Regardless of the reasonableness of DB’s coverage decision, DB can’t escape bad faith liability on this basis. Why? Because DB didn’t undertake a reasonable investigation into whether the claims truly stemmed from nonaccidental conduct. And where a reasonable investigation would have disclosed facts showing the claim was covered, . . . [t]he insurer cannot claim a genuine dispute regarding coverage. . . . Just so here. Based on the vague and broad allegations in the Piedmont Action, including allegations that Piedmont negligently failed to remedy various habitability issues, DB couldn’t reasonably conclude no ‘occurrence’ existed without further investigation. Indeed, under California law, the negligent failure to repair can constitute an ‘occurrence’ when an unexpected or unforeseeable consequence results. . . . But here, DB didn’t even bother asking Piedmont whether the tenants’ damages were unexpected or unintended, and thus potentially an ‘occurrence’ under the DB policies. Rather, based solely on the allegations in the Piedmont Action, DB cursorily concluded no ‘occurrence’ existed without any further investigation into the salient facts. And for that reason, the Court can’t find DB’s decision to deny coverage for lack of an ‘occurrence’ was based on a genuine dispute.”

So Seneca got what it wanted. DB may have acted in bad faith. And now Seneca may have to investigate the facts surrounding "no occurrence" complaints when addressing its duty to defend. This includes asking its insureds if damages were unexpected or unintended. I wonder what the answer is going to be.

|

|

| |

|

|

|

Vol. 8 - Issue 9

November 6, 2019

A Coverage Opinions Rarity: A Case About Cancellation (Usually Sleepy Issue, But This One’s Worth Reading)

|

|

|

| |

This might just be a Coverage Opinions first – discussion of a case about an insurer cancelling a policy. Such cases are usually not good candidates for CO. They are often-times dull and involve issues, especially statutory, that are unique to their state.

But Yang v. Everest National Ins. Co., No. 344987 (Mich. Ct. App. Aug. 27, 2019) made the cut.

Everest sent Wesley Yang a bill for his no-fault insurance policy and informed him that the policy would be cancelled if payment was not received by the due date. Yang did not make the payment. He and his wife were subsequently injured in a pedestrian-automobile accident. They sought coverage and Everest said no as the policy had been cancelled.

Litigation ensued and the trial court found for the insureds. Everest appealed.

The appeals court summed it up: “At issue in this case is whether an insurer may cancel a policy by sending the statutorily required ‘notice of cancellation’ to the insured before the grounds for cancellation have occurred. We hold that such notice does not satisfy the Insurance Code, MCL 500.100 et seq., and is therefore ineffective to cancel the policy. Accordingly, we affirm the trial court.”

In essence, the court held that “a notice of cancellation which states that a policy will be cancelled on a specified date unless premiums due are sooner paid, is not a notice of cancellation, but merely a demand for payment.”

Therefore, an insurer needs to send a cancellation notice immediately after payment is not received by the due date. Then, the policy will cancel however many days later that notice of cancellation was required, based on any statute or policy provision. So, if a loss occurs during that notice period, it is covered, even if the insured does not ultimately pay the premium.

Yes, the case involves a Michigan statute. However, I believe that it offers lessons that go beyond the Great Lakes State. Indeed, the court looked at how several states nationally have addressed the issue, and concluded that it was adopting the majority rule. Insurers would be well-served to examine how they handle cancellation notices.

The issue arises from the following scenario:

“On October 9, 2017, Everest mailed Yang a bill for the second premium installment payment that contained a notice of cancellation for nonpayment of the premium. The document informed Yang that he must pay the premium by October 26, 2017. It stated that the failure to pay that amount by the due date ‘will result in the cancellation of your policy with the indicated Cancellation Effective Date,’ October 27, 2017. Thus, the document provided that if the premium payment was not received by October 26 the policy would be cancelled effective the next day. It also stated that the cancellation notice did not apply if the bill was paid by the due date.

On October 30, 2017, Everest, having not received the premium payment, sent Yang an offer to reinstate the policy. It informed Yang that his insurance was cancelled as of October 27, 2017, because it did not receive the premium payment by the due date. The letter informed Yang that he could reinstate the ‘policy with a lapse in coverage’ if it received payment by November 26, 2017.

Yang sent a payment for the premium on November 17, 2017, and Everest reinstated the policy effective on that date. The notice of reinstatement informed Yang that there was a lapse in coverage from October 27, 2017 to November 17, 2017.

The accident in which plaintiffs were injured occurred on November 15, 2017, two days before Yang made the premium payment.”

This sounds confusing. To summarize, Yang’s policy was cancelled as of October 27, 2017 for non-payment of premium. And, as Everest saw it, notice of cancellation had been provided when Everest sent the October 9, 2017 bill to Yang that contained the notice that policy would be cancelled if the premium had not been paid.

But here’s the problem for Everest. The notice of cancellation was sent before the premium was due. The court rejected this as being in compliance with the statutory notice of cancellation obligation: “For a cancellation to take place, the event triggering the right to cancel must have taken place first. In this case, the event that allowed for cancellation occurred on the date of nonpayment. Therefore, it is only after the nonpayment that the insurer may properly notify the insured of cancellation. In other words, it is not sufficient that the insurer warn the insured that a future failure to pay the premium will result in cancellation; rather, it must advise the insured that, because of an already-occurred failure to pay, the policy will be cancelled in ten days. This reasoning is consistent with the Michigan Supreme Court’s understanding of MCL 500.3020.”

The court observed that this decision was consistent with the majority of courts nationally that have addressed the issue.

As I noted above, an insurer needs to send a cancellation notice immediately after payment is not received by the due date. Then the policy will cancel however many days later that notice of cancellation was required, based on any statute or policy provision. So, if a loss occurs during that notice period, it is covered, even if the insured does not ultimately, pay the premium.

|

|

| |

|

|

|

Vol. 8 - Issue 9

November 6, 2019

Appeals Court: Insured Can’t Deny Coverage And Then File A DJ

|

|

|

| |

This seems like a peculiar case to me. I’ve certainly never seen this issue addressed before. At issue in United Specialty Ins. Co. v. Cardona-Rodriquez, No. A19A0859 (Ga. Ct. App. Oct. 16, 2019) is coverage for a car washing business, Geno’s Car Wash, for an injury sustained by a customer, Rodriguez, when an employee struck him with a vehicle.

United Specialty, the car wash’s insurer, filed an action seeking a declaratory judgment that the maximum limit, owed under its “Commercial Lines Policy,” is $25,000, because the employee was operating Rodriguez’s vehicle without a valid Georgia driver’s license. The trial court concluded that a driver’s license is not required to operate a vehicle on private property. Thus, the policy limit for the accident is $100,000.

The case went to the Georgia appeals court. Here is where it got peculiar. The court addressed whether there was a justiciable controversy, as required to establish jurisdiction under the Georgia Declaratory Judgment Act.

The court noted that “even though United asserted that it was providing a defense for [Geno’s Car Wash] under a reservation of rights, it unequivocally rejected Rodriguez’s $100,000 demand for payment under the policy and offered him $25,000. The reservation of rights letter did not assert that United was uncertain as to its rights or the policy limits, or advise Lewis that it was unclear how to proceed under the policy given that [the employee] was operating the van without a license. Instead, United’s litigation specialist unequivocally asserted that ‘the limits of liability coverage under your policy are $25,000, which is the basic financial responsibility limit required by the State of Georgia.’”

Based on this, the court concluded that there was no justiciable controversy as “United elected to deny Rodriguez’s demand for the full $100,000 limit of the policy, prompting Rodriguez to file suit. . . . United consistently denied the existence of policy limits of $100,000. Accordingly, United is not in need of any direction from the court with respect to future conduct on its part.”

The court cited several Georgia cases purportedly supporting this conclusion, including Builders Ins. Group v. Ker-Wil Enterprises, 274 Ga. App. 522, 523 (618 SE2d 160) (2005), which the court described as “affirming dismissal of workers’ compensation insurer’s declaratory judgment action because [insurer] had already denied coverage when it filed its petition for declaratory relief, [and] was not uncertain or insecure of its rights, status, or legal relations with respect to the making of that decision.”

Needless to say, the obvious response is that, simply because United maintained that the policy limit was $25,000, others did not agree. Thus, there was still a dispute over the amount of the policy limit. Under the court’s rationale, as long as parties are dug-in in their positions, there is no dispute between them.

But even if that’s the law, at least the court carved out an exception. However, the exception is peculiar. It appears that an insurer can maintain that coverage is not owed, but still establish the existence of a dispute needed to maintain jurisdiction for a declaratory judgment action, by having told the insured that it would “reconsider its position if the insured disagreed and/or could provide additional information that may have a bearing on the coverage issue.”

As the court saw it, the inclusion of such language creates uncertainty in the insurer, as to its coverage determination, which creates a justiciable controversy necessary for jurisdiction under the Declaratory Judgment Act.

The court also noted that its decision was dictated by a desire to prevent an insurer from denying coverage and then using the declaratory judgment procedure as a means to avoid bad faith exposure.

Accordingly, the appeals court held that the trial court was without jurisdiction to render a declaratory judgment.

|

|

| |

|

|

|

Vol. 8 - Issue 9

November 6, 2019

Court Concludes That Murder Can Be An “Accident”

|

|

|

| |

While sometimes tragic, coverage cases involving bar fights and shootings often involve interesting facts. Needless to say, there’s usually a story there. But despite this, I often times do not address such cases in Coverage Opinions. Most of the time, coverage is not owed in these scenarios, based on the injury not having been caused by an “occurrence”/accident or the expected or intended exclusion or an assault and battery exclusion.

When a court concludes that an assault and battery exclusion precludes coverage to a bouncer, for beating up a bar patron, it’s probably not a decision that offers much in the way of a lesson to be learned. But show me a case where a court holds that an assault and battery exclusion does not serve to preclude coverage to a bouncer, for beating up a bar patron, and now you’ve got my attention.

This is why Maxum Indemnity Co. v. Broken Spoke Bar & Grill, No. 13-804 (W.D. Ky. Sept. 27, 2019) made its way into this issue of CO. The court held that an insured’s act of murder could qualify as an “occurrence”/accident. Granted, other coverage provisions served to preclude coverage, but, still, murder as an accident….

At issue in Broken Spoke was coverage for Chris Gribbons, under a liability policy issued to Chris Gribbons d/b/a Raywick Bar & Grill, for a suit filed against him for killing David Litsey.

The story is that Gribbins confronted Litsey in a crowd outside the bar where Gribbins “pistol whipped” Litsey. The gun discharged killing Litsey. Gribbins argued self-defense. A jury found Gribbons guilty of Wanton Murder.

Turning to the civil case, Maxum undertook Gribbons defense, under a reservation of rights, and then filed an action seeking a declaration that it owed no coverage to Gribbons for defense or indemnity.

First up for the court was whether the “bodily injury” was caused by an “occurrence,” defined as an accident. The court concluded that it could be.

At the heart of the court’s decision was the fact that Gribbons had been found guilty of “wanton murder.” Of significance, the court in the criminal case charged the jury that, to convict Gribbons, he must have been “wantonly engaging in conduct which created a grave risk of death to another and thereby caused the death of David Litsey, Jr. under circumstances manifesting an extreme indifference to human life.”

Then, the court defined “wantonly” as “[a] person acts wantonly with respect to a result or to a circumstance when he is aware of and consciously disregards a substantial and unjustifiable risk that the result will occur or that the circumstance exists. The risk must be of such nature and degree that disregard thereof constitutes a gross deviation from the standard of conduct that a reasonable person would overserve in the situation.”

The court’s conclusion was that these instructions permitted a conviction for wanton murder without a finding that Gribbons intended Litsey’s death.

And, conveniently, this issue had been addressed by the Kentucky Supreme Court its Gribbons’ appeal of his criminal conviction. The Kentucky Supreme Court concluded that the jury had heard evidence sufficient to instruct on both wanton murder and intentional murder and “the jury could have reasonably believed that by ‘using a loaded handgun[] as a club to beat Listey, Gribbins consciously disregarded a substantial and unjustifiable risk that the handgun might accidently be discharged.’”

Putting this in simple terms, Gribbons’s conviction for wanton murder did not forestall the possibility that Gribbons did not intend Litsey’s death. Add to this that, under Kentucky law, only intentional acts are non-accidental (as well as “inferred intent” situations, when a person intentionally commits an act certain to cause that particular kind of harm). Moreover, even reckless disregard for an obvious danger is an accident because the insured did not intend the injury.

Putting these two together, the court concluded that wanton murder could be an accident.

When all was said and done, Gribbins’s victory on the “occurrence”/accident issue was a moot point, as the court held that coverage was still precluded by the expected or intended exclusion and assault and battery exclusion.

But still, murder as an accident….That gets my attention.

|

|

| |

|

|

|

Vol. 8 - Issue 9

November 6, 2019

Interesting “Use Of An Auto” Case

|

|

|

| |

Cases addressing whether injury or damage was caused by “use of an auto” are often times interesting. They can arise under general liability or homeowner’s liability policies – does the “use of an auto” exclusion apply? And they can arise under auto policies, where the insuring agreement requires that injury or damage be caused “by use of an auto.”

It is not surprising that these cases would be interesting. After all, since automobiles are designed with a clear purpose in mind, what’s “use of an auto” shouldn’t be all that hard to figure out. So, if “use of an auto” is being litigated, then it’s probably because the claim involves something more than a person simply sitting behind the wheel, motoring down the road, minding their own business, en route to Point B.

And that’s what can be said about Wilkinson v. Georgia Farm Bureau Mutual Ins. Co., No. A19A1447 (Ga. Ct. App. Sept. 20, 2019).

For convenience sake I’ll set out the facts verbatim from the opinion (not to mention that the decision is fact intensive): “[T]he record shows that Paul Buchanan and Egbert Wilkinson were friends and coworkers. On August 18, 2015, Buchanan purchased a 1994 Ford F350. Egbert asked Buchanan if he could ‘look at’ the truck, and Buchanan agreed. According to Buchanan, the Wilkinsons were not going to test drive the truck but only wanted to look at the truck. On September 30, 2015, at approximately 8:30 p.m., Egbert and Barbara went to Buchanan’s house to look at the truck. Buchanan drove the truck forward approximately eight feet from where it was parked in his driveway so that the Wilkinsons could walk around the vehicle to inspect it. The truck, which was still in front of Buchanan’s garage in the driveway, was parked on an incline and facing the street. Buchanan turned the truck on, placed it in neutral, and set the emergency brake. As Egbert and Buchanan stood outside the truck conversing with each other, Barbara sat in the driver’s seat of the truck. Barbara then exited the truck and spoke with Buchanan. As Buchanan and Barbara went to inspect the truck’s engine, Buchanan told Barbara to pull the truck’s ‘hood latch,’ and warned her to not pull the emergency brake. Barbara looked under the truck’s dashboard, pulled the emergency brake, and the truck ‘took off,’ after which Buchanan saw her lying under the truck. According to Buchanan, Barbara had been holding on to the ‘door jamb’ when she fell, and the truck rolled over Barbara’s ankles as it traveled down the driveway. Buchanan ran after the truck, jumped inside, and stopped the truck. Barbara allegedly sustained multiple injuries, including an open fracture of her left ankle, a right shoulder avulsion fracture, fractures of the tibia and fibula, and a left knee effusion.”

You know where this is going. The Wilkinsons filed suit against Buchanan. Buchanan’s homeowner’s insurer, Georgia Farm Bureau, filed a declaratory judgment action seeking a determination whether it was obligated to defend Buchanan under a homeowner’s policy. GFB relied on numerous policies provisions that it believed precluded coverage. Most importantly was the exclusion for injuries “arising out of . . . [t]he ownership, maintenance, use, loading or unloading of motor vehicles. . . .owned or operated by or rented or loaned to an insured.”

The trial court granted summary judgment for GFB, concluding that the truck was “in ‘use’ at the time of the incident because ‘[t]he truck was being used … to demonstrate its function and operability,’ ‘and that such use resulted in [Barbara]’s injuries.’”

The case went to the Georgia appeals court which reversed, explaining: “It is true that the evidence shows that Buchanan’s truck was at or near the location of the accident, that the accident was caused by Barbara pulling the truck’s emergency brake, and that at the time of the accident, Buchanan and Barbara were examining its components. However, the evidence fails to show that the vehicle was in ‘use’ as a vehicle at the time of the accident. Indeed, the truck was parked in Buchanan’s driveway and had not been employed for any purpose at the time of Barbara’s injury. Instead, the evidence merely shows that the parked truck was being inspected at the time of the accident. Thus, it cannot be said that the vehicle was in ‘use’ as a vehicle at the time of Barbara’s injuries.” (emphasis in original).

|

|

| |

|

|

|

Vol. 8 - Issue 9

November 6, 2019

Mind The Gap In Citizenship: Federal Court Makes It Hard To Sue Lloyd’s Based On Diversity

|

|

|

| |

This issue is very narrow. But for those whom it is relevant, it is of paramount importance. Can you get diversity jurisdiction over Lloyd’s to sue the insurance marketplace in federal court?

As the court put it in CNX Gas Co. v. Lloyd’s of London, No. 19-699 (W.D. Pa. Oct. 17, 2019): “[B]ecause [of] Lloyd’s unique structure as merely a forum for thousands of underwriters to buy shares of risk [it] makes it difficult to execute the citizenship analysis required to determine diversity jurisdiction. That is the difficulty at the heart of this case.”

The coverage issue in CNX Gas is complex. In general, CNX sued “Lloyd’s” (more about that in a moment) in Pennsylvania state court seeking coverage under a Control of Well insurance policy for an oil well that was rendered useless after an accident in its operation. The coverage issues, and why there was a dispute, are not relevant to the analysis here.

Lloyd’s sought to remove the action to federal court based on diversity of citizenship. At issue was whether Lloyd’s established complete diversity for purposes of jurisdiction.

The court’s decision is detailed. I’ll keep it simple here. CNX’s complaint named only five Lloyd’s “names” as defendants. Names are the individual investors, who subscribe to a share of risk under an insurance policy, within a collective unit, called a syndicate. However, CNX maintained that, in fact, all names were included as defendants, since the complaint included the following: “Defendants herein are all of the underwriters of a Certificate of Insurance. . . . On information and belief, the Defendants are the ‘names’ and members of the following Lloyd’s indicates: 1084, 4141, 33, and 9223.”

The defendant maintained that, if “Plaintiff wanted to sue all the Names, it should have included all of them, or least the names of the Syndicates they comprise, in the caption.” But the court was not persuaded: “Plaintiff cannot be blamed for failing to identify every Name before discovery. This is especially the case because identities of Lloyd’s Names are usually kept confidential.” Thus, the court held that the plaintiff’s complaint adequately pleaded, as defendants, all of the Names who underwrote the Control of Well Policy.

Having established who is being sued, the court turned to whether there was diversity of citizenship. At issue – whose citizenship is relevant for purposes of establishing diversity?

The court noted that there was a split among the circuits, which comes down to this: “[W]hether, for diversity purposes, a Lloyd’s syndicate is more like a trust or a limited partnership—in other words, whether only the representative Name’s citizenship is relevant (the trust model), or whether the citizenship of all of the Names must be considered (the limited partnership model).”

The court described the circuit split on the issue: The Sixth Circuit takes the minority position -- only a Name serving as lead underwriter counts for diversity purposes. However, the majority (Second, Seventh, and Eleventh Circuits) “take the view that when a syndicate is sued, the citizenship of every Name comprising the syndicate counts, not merely that of the Name serving as lead underwriter.”

The court also noted that “District courts addressing this issue in circuits without direct authority from their respective courts of appeals—including all of those that have done so in this circuit [Third]—overwhelmingly side with the majority regime.”

The Court adopted the majority view and required complete diversity to exist between Plaintiff and all of the Lloyd’s Names underwriting the COW policy.

This can be a tall order for the defendant, which must identify the citizenship of all the Names to permit the Court to exercise diversity jurisdiction on removal.

However, here, “[o]nly the identity of the Names comprising Syndicates 1084, 9223, 4141 and 72.6 percent of Syndicate 33 are established. The Names comprising the remaining 27.4% of Syndicate 33 remain a mystery. Importantly, the remaining 27.4% of Syndicate 33 allegedly consists of over 1,800 Names.”

Yikes for the defendant.

The court concluded that the “failure to identify and establish the citizenship of some 1,800 unidentified Names comprising the minority share of Syndicate 33 makes it impossible for the Court to establish complete diversity. At the very least, it creates substantial doubt as to whether such complete diversity exists. This doubt must be resolved in favor of remand.”

|

|

| |

|

|

|

| |

|

| |

|

|

Court Holds That Raccoons Cannot Commit Vandalism

At issue in Capital Flip, LLC v. American Modern Select Insurance Company, No. 19-180 (W.D. Pa. Sept. 19, 2019) was coverage for Capital Flip, LLC, under a property policy, for damage caused by raccoons that had entered the interior of a structure. Capital Flip argued that coverage was owed as the damage was caused by the covered peril of vandalism or malicious mischief. The insurer disagreed and Capital Flip filed a coverage action.

Following an examination of all sorts of definitions of vandalism and malicious mischief, as well as a review of cases nationally that have addressed whether coverage for damage caused by animals qualified as vandalism or malicious mischief, the court held that no coverage was owed: “This Court agrees with the cases cited above that damage caused by animals—in this case, raccoons—cannot be deemed to have arisen from ‘vandalism’ or ‘malicious mischief.’ Both the common and legal usage of those terms presuppose conscious, willful misconduct by a human being. Raccoons and their companions in the animal kingdom cannot formulate the intent needed to engage in ‘vandalism,’ ‘malicious mischief’ or any other criminal or actionable conduct. Animals do not have conscious agency and are not subjects of human law.”

I wonder about this – What about a dog, with separation anxiety, or angry at its owner for leaving the house, who chews the dining room chair while home alone? Isn’t the dog acting with intent necessary for malicious mischief, which the court defined to include intentionally destroying or damaging another’s property. Just throwin’ it out there.

This Is What’s Wrong With The Legal System

The court’s decision in Manley v. Hain Celestial Group, Inc., No. 18-7101 (N.D. Ill. Sept. 30, 2019) starts like this: “Feeling defrauded by a sunscreen label that directed her to ‘SHAKE WELL’ rather than ‘SHAKE VIGOROUSLY for 10 seconds,’ plaintiff Katy Manley filed against defendant Hain Celestial Group, Inc. a six-count complaint asserting claims for violation of the Illinois Consumer Fraud and Deceptive Trade Practices Act, breach of express and implied warranties, negligent misrepresentation and unjust enrichment.” Say no more.

[For five counts, the court granted the defendant’s motion to dismiss with prejudice. The court dismissed a sixth count without prejudice and gave plaintiff 28 days to file an amended complaint if she so chose. I checked the docket and found this October 28th entry: “The parties have informed the Court that the case has settled and that they intend to file their dismissal paperwork before the district judge shortly.”]

|

| |

|

|

|

| |

|

|

|

|

|

|

|

|

|